For more than four years, elevated interest rates intended to combat inflation have provided an unusually strong earnings environment for credit unions. Rising yields pushed the net interest margin well above operating expenses, creating a spread that sustained earnings with less dependence on non-interest income.

But with rate cuts beginning in the fourth quarter of 2025 and further easing expected through 2026, those conditions are shifting.

Asset yields are beginning to retreat just as competition for deposits intensifies — putting pressure on margins and raising a pressing question for the industry: what comes next for credit union earnings?

Credit Union Earnings Then And Now

To determine where earnings might go, it’s helpful to understand the primary drivers in today’s environment.

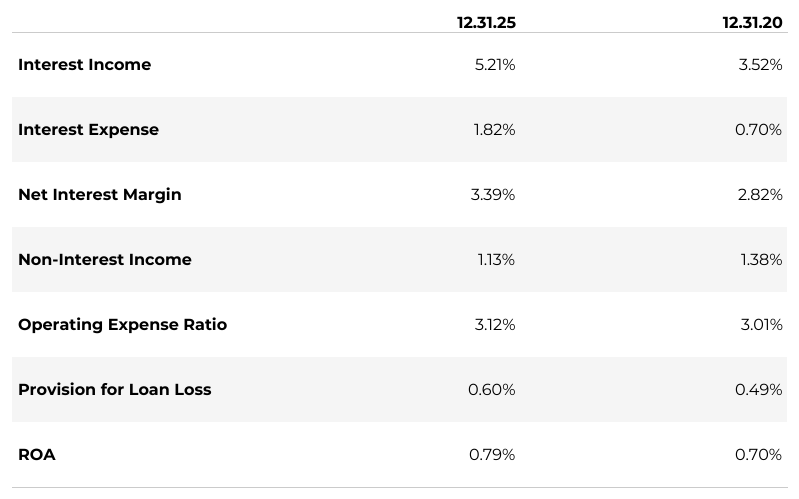

EARNINGS MODEL COMPARISON EXPRESSED AS A % OF AVERAGE ASSETS

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.25

SOURCE: CALLAHAN & ASSOCIATES

Increased interest rates have played an outsized role in supporting credit union performance in the past half-decade. Since the fourth quarter of 2020, the net interest margin has jumped from 2.82% to 3.39%, more than offsetting the rise in operating expenses and carrying earnings.

During that period, non-interest income dropped from 1.38% to 1.13% of assets, not because there was less of it but because assets grew faster.

If rates come down as expected, support from the net interest margin will normalize and the earnings model will start to rebalance. Expenses tend to be slow-moving, but revenue lines can shift quickly, making the composition of non-interest income more important than the level alone.

Unlike interest income, which largely follows rate cycles, non-interest income represents a set of levers credit unions can influence through pricing, product design, and member engagement. That makes it an important mechanism for sustaining earnings as margin support fades.

The Limits Of Public Reporting

Not all non-interest income behaves the same. Understanding how each component performs, and how that mix differs across credit union peers, is just as important as the total itself when navigating a new environment.

The 5300 Call Report groups non-interest income into broad categories like fee income and other operating income, which are useful for trend analysis but do not offer insight into what is driving change or how institutions are adapting. Such detail becomes even more important when margins tighten.

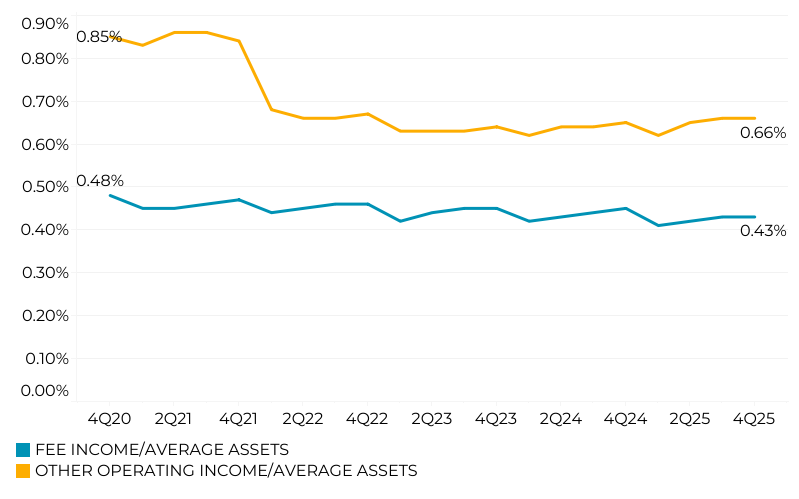

NON-INTEREST INCOME SOURCES

FOR U.S. CREDIT UNIONS | DATA AS OF 12.31.25

SOURCE: CALLAHAN & ASSOCIATES

Comparing how loan late fees move with asset quality or how interchange tracks with member spending helps credit union leaders connect revenue performance to underlying member behavior and economic pressure. Without that context, similar top-line results can mask very different patterns in drivers across peers.

That level of analysis requires more detail than the call report provides. Participation in Callahan’s Non-Interest Income Study helps credit unions explore questions such as:

- How are peers adjusting NSF and overdraft strategies amid increased consumer scrutiny and regulatory focus?

- As mortgage activity picks back up, are credit unions reintroducing secondary market sales as a meaningful earnings lever or are they relying more heavily on retention?

The study breaks down non‑interest income into its component parts and allows leaders to compare patterns across peers to determine where revenue is gaining traction, where it is fading, and how they might need to adjust their own mix as margin support fades.

Do you want to take part in next year’s study. Callahan & Associates’ annual Non-Interest Income Study is the industry’s only comprehensive, participant‑reported analysis of NII performance nationwide. Participating credit unions gain insight into how high‑performing institutions structure successful NII strategies, helping leaders align decisions with both organizational goals and member needs. Looking for clarity, granularity, and benchmarking confidence not available through traditional reporting?Learn how to join the 2026 study.