Top-Level Takeaways

-

Interest rate risk strategies at Purdue Federal Credit Union also generate revenue.

-

The Indiana credit union uses a third-party advisor to help it execute different kinds of debt and trading instruments

Purdue Federal Credit Union ($1.1B, West Lafayette, IN) is using rate swaps and hedging to simultaneously dampen interest rate risk and generate revenue.

Purdue Federal began interest rate swaps shortly after the NCUA granted the credit union derivative-trading approval in December 2015. Since then, the strategy has generated approximately $1.5 million in extra interest income from the loans Purdue Federal has been able to hold rather than sell.

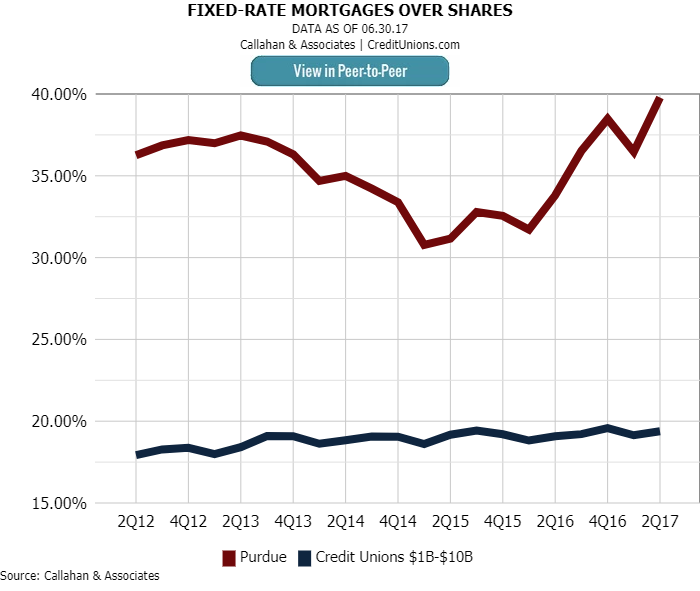

These swaps are basically agreements between the credit union and a trading partner to trade one stream of interest payments for another over a set period. Derivative contracts have allowed Purdue Federal to hold an additional $80 million in first mortgages in a real estate loan portfolio that grew 18.71% year-over-year to $628.42 million in the second quarter of this year. ContentMiddleAd

Meanwhile, the credit union expects its mortgage pipeline hedging strategy to add 3 basis points a year to its ROA.

Purdue Federal works with an outside advisor to administer the hedging program, which helps the credit union provide rate locks to members while mitigating risk from rising interest rates.

Purdue Federal Credit Union’s derivatives program has helped it hold on to a much higher percentage of the mortgages it originates than other credit unions with $1 billion to $10 billion in assets, according to second quarter data from Callahan Associates.

The strategy involves evaluating new loans daily, lowering risk by taking daily losses and gains while committing the mortgages to future sales as much as 120 days out at a to-be-announced price.

Hedging helps dampen the market risk that occurred when Purdue Federal was selling loans to Fannie Mae with the typical 45-day delivery date. So do the four interest rate swap transactions the credit union currently has on its balance sheet.

Brian Musser, CfO, Purdue Federal

Whereas these kinds of debt and trading instruments are considered quite liquid and fairly plain vanilla in trading circles, they’re not for amateurs.

I wouldn’t recommend trying to do these yourselves, says Brian Musser, Purdue Federal’s CFO since 1991.

He says it required some effort to get the programs up and running; however, now it’s the third-party advisor that does the heavy lifting. Musser and his team focus on growing a robust lending operation that includes an unusually large mortgage market share.

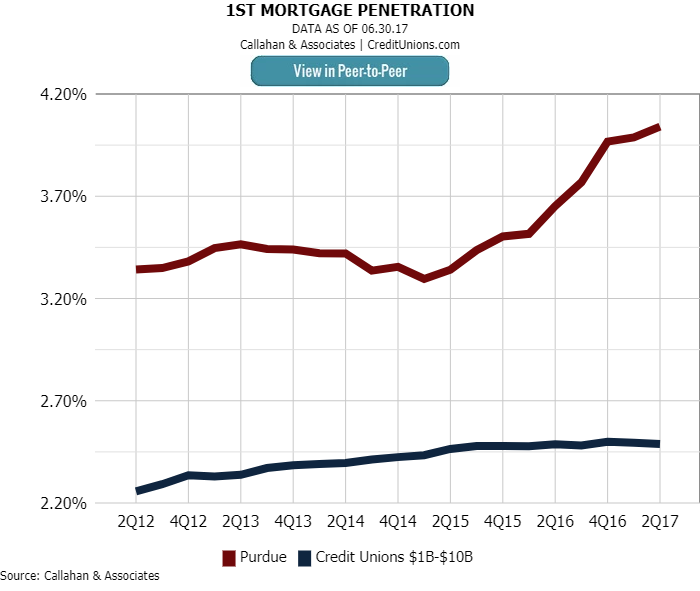

Purdue Federal’s first mortgage penetration is well above the average credit union its size, despite a membership that includes a sizable share of far-flung Purdue gradates.

Musser says Purdue Federal’s penetration rate jumps up to 7.98% when counting loans it has sold but still services.

Purdue Federal ranked first among all lenders in its home Tippecanoe County market, according to data available in MortgageAnalyzer from Callahan Associates. In 2015, the most recent year for which HMDA data is available, the credit union captured a 13.54% share in applications and 20.43% in market share in dollar amount of loans funded, with 758 loans funded out of 973 applications.

Are You Ready For HMDA?

Don’t fear the annual data dump. MortgageAnalyzer makes it easy to assess market data and trends. New data is coming soon. Request a demo today.

Musser says when loans for other entities are added in ― including FHA loans closed for Quicken Mortgage ― Purdue Federal actually took 1,601 applications in 2015 and funded 961 of them for $172,121,958.

Purdue Federal uses ALM First as it advisor for interest rate swaps and internal hedgine. Find your next partner in Callahan’s onlineBuyer’s Guide.

The growing portfolio, and accompanying interest rate risk, is the result of Purdue Federal’s decision to build its first mortgage volume as the refinance market faded.

Building relationships with local realtors; adding new products, such as a competitively priced construction loan; and deepening ties to the residential rental business that flourishes around a major university has helped drive that mortgage business. Now, the credit union’s derivatives and hedging work is keeping the interest rate volatility in check.