|

| Brad Houle, President and CEO, CAHP Credit Union |

CAHP Credit Union ($157.5M, Sacramento, CA) was there when the economic CHiPs were down for its peace officer members across the Golden State, and the membership has responded in kind.

CAHPCU was founded by a group of California Highway Patrol officers in 1969, several years before the television show gave them fame and 40 years before the Great Recession gave them fits.

When hard times hit, CAHPCU did not pull back from lending. Instead, it increased its flexibility and relied more heavily on analytics to make decisions. It also doubled down on developing personal relationships with its far-flung membership.

CU QUICK FACTS

CAHP Credit union

Data as of 12.31.15

- HQ: Sacramento, CA

- ASSETS: $157.5M

- MEMBERS: 15,089

- BRANCHES: 2

- 12-MO SHARE GROWTH: 18.83%

- 12-MO LOAN GROWTH: 32.66%

- ROA: 1.24%

The results show in the numbers. With two branches one each in Sacramento and in suburban Los Angeles and 28 employees, CAHPCU has posted strong growth numbers over the past few years, culminating with a fourth quarter 2015 showingof 18.83% share growth and 32.66% loan growth both year over year and a healthy ROA of 1.24%.

Those numbers exceed its peer averages. For example, it ranked at No. 16 in loan growth among the nation’s 726 credit unions with $100 million to $250 million in assets, according to data from Callahan & Associates. Drilling down, auto loangrowth was similarly impressive, 41.95% versus 11.95% for its peer average.

And that’s all through direct lending. In fact, CAHPCU doesn’t participate in indirect lending.

Direct lending keeps us connected to our members and their needs, says president and CEO Brad Houle.

Those direct loans are performing well. Of the credit union’s 2,500 loans, there were no new delinquencies in the past three months of 2015. Not one.

How Do You Compare?

Check out CAHP Credit Union’s performance profile then build peer groups to see how you compare.

That’s no accident. The credit union relies on a mix of sophisticated lending software and proper training.

Low delinquencies begin with the initial underwriting review, Houle says. We also invest in training and education for our staff. Although it might appear to cost the credit union more to do that, the results are evident in ournumbers.

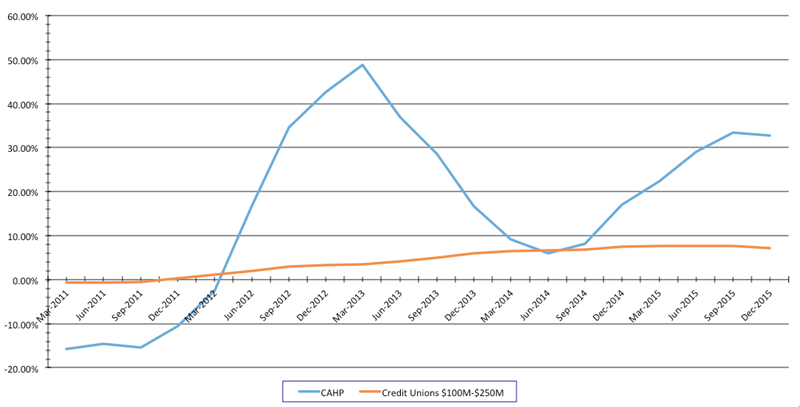

LOAN GROWTH

For all credit unions $100-$250 million in assets | Data as of 12.31.15

Callahan & Associates | www.creditunions.com

CAHPCU’s year-over-year loan growth has bested the national average posted by credit unions of its size. Source:Peer-to-Peer Analytics by Callahan & Associates

Building On The Post-Recession Boom

Many financial institutions expected a quick rebound from the recession and tightened lending while they waited. Not so at CAHP.

We realized this was the new normal, Houle says. We learned bad things happen to good people. In order to survive as a credit union, we had to learn how to lend to today’s borrower.

So the credit union uses technology as well as its human resources to listen and learn.

CAHP Credit Union uses Sertech’s ProAct Loan Portfolio Management to manage risk and support its lending decisioning. Find your next solution in the Callahan & Associates online Buyer’s Guide.

Integral to our success is understanding a member’s motivation for borrowing money as well as their long-term debt obligations, Houle says.

That requires the credit union to build member trust. For example, it shows solidarity by developing and investing in relationships with those who support the causes important to peace officers, Houle says.

It also builds ties with the members themselves.

Part of understanding a member’s motivation is developing a rapport with them, Houle says. People appreciate that time and the overall experience.

That time and experience combined with a competitive cross-sell incentive program and word-of-mouth referrals has set the stage for deep relationships that can last for years.

Peace officers are a close-knit group, Houle says. Members who trust us will recommend us to family and co-workers and return to us for future needs, even if we don’t have the lowest loan rate.

A Sense Of Ownership

Credit card penetration at CAHP also beats its peer average, a result in part of presenting the card much like a value meal that includes a credit card with most new CAHP loans and other accounts, Houle says.

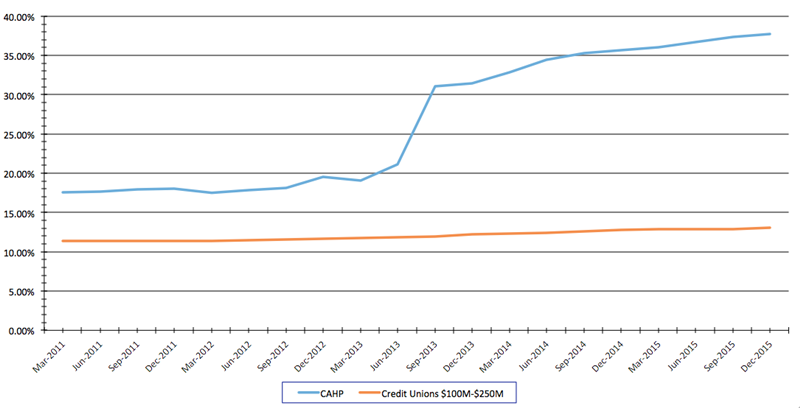

CREDIT CARD PENETRATION

For all credit unions $100-$250 million in assets | Data as of 12.31.15

Callahan & Associates | www.creditunions.com

CAHPCU’s credit card penetration is three times that of the average credit union in its asset-based peer group. Source: Peer-to-Peer Analytics by Callahan & Associates

As with auto loans, staff incentives play a role in building wallet share and sustaining growth. Those were part of a pivot that Houle initiated after he took over four years ago.

3 Tips To Boost Lending

CAHP Credit Union president/CEO Brad Houle shares three keys to credit union success.

- Invest in training and education.

- Pay staff members what they’re worth and don’t be afraid to develop a competitive incentive program.

- Develop a strong decision support system to measure, monitor, and manage risk.

We believe a change in behavior leads to a change in mindset, Houle says. Training and a comprehensive, competitive incentive program that rewards staff every step of the way will reinforce the change and ultimately lead to achange in culture.

Employees own the process, but they’re not the only ones over whom a sense of ownership has been inculcated. The credit union also strives to make its members feel vested in their trusted financial provider.

We believe when you do the right thing, you can’t go wrong, Houle says. Our goal is to develop strong relationships with our primary SEG. The result has been an increase in assets and lending and our ability to continueto serve more peace officers throughout California.