The state of Wyoming ranks 10th among U.S. states in size, last in population, and somewhere in the top three in terms of beauty. It stretches out across the Great Plains 430 miles separate Jackson, located at the foot of Yellowstone National Park in the northwest corner, from Cheyenne, the state’s capital in the southeast corner and shares a border with Colorado, Utah, Idaho, Montana, South Dakota, and Nebraska.

Thanks to its natural resources, the Cowboy State’s economy relies heavily on tourism and mineral production think coal, natural gas, oil, and trona for employment and income. Other top industries include health care, agriculture, education, military, and government. With so much ground to cover, and so many industries to serve, the market for financial services can be challenging. Now, imagine serving this area with a multi-SEG charter.

Such is the case for Meridian Trust Federal Credit Union ($331.1M, Cheyenne, WY), the state’s second-largest credit union.

Despite hurdles in the forms of membership breadth, market size, and a rollercoaster economy, the credit union is thriving as it enters its 63rd year of operation.

CU QUICK FACTS

Meridian Trust FCU

Data as of 06.30.16

- HQ: Cheyenne, WY

- ASSETS: $331.1M

- MEMBERS: 26,637

- BRANCHES: 6 (+2 shared)

- 12-MO SHARE GROWTH: 7.3%

- 12-MO LOAN GROWTH: 8.8%

- ROA: 0.83%

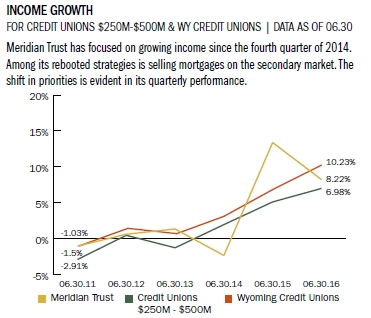

In the second quarter of 2016, the credit union posted positive 12-month growth rates in shares, loans, assets, and capital not unlike its state and asset-based peers. But unlike peer institutions, Meridian Trust’s 12-month growth in net income was 32.5%, compared with negative rates for peers. In addition, Meridian Trust’s efficiency ratio of 75.6% easily bested state and peer averages of 88.7% and 87.4%, respectively.

How does the credit union do it? Through an understanding of its market, a philosophy of continuous improvement, and a forward-looking approach.

No Mass Markets Here

A group of state employees founded Meridian Trust in 1954 as Wyoming Employees Federal Credit Union. Early offices included the State Board of Charities and Reform and a basement storage room in the state capitol.

By the late 1970s, the growing SEG-based institution was operating four branches. However, the worldwide energy crisis at the end of the decade caused the United States to severely decrease oil production. This led to layoffs at American oil fields.

The economy collapsed, says Meridian Trusts’s president and CEO Kim Withers.

The oil crisis hurt the credit union, too, which closed two branches and struggled for a number of years.

But that’s in the past.

Today, Meridian Trust owns six branches and shares two more with Utah Power Credit Union ($588.9M, Salt Lake City, UT) through its Power Trust CUSO.

The credit union’s branch network encompasses the state capital of Cheyenne, where a high concentration of Wyoming state employees work; tourist-heavy Jackson, located at the foot of the Grand Teton Mountains; and the more industrial Rawlins, whose several large employers include an oil refinery and prison that offer good pay.

We make a lot of toy loans in Rawlins, says Trevor Rutar, Meridian Trust’s chief lending officer. ATVs, RVs, and big pickup trucks do well in that area.

Its newest branch area, however, isn’t in Wyoming. It’s in Scottsbluff, NE, an underserved area approximately 100 miles northeast of Cheyenne, where Meridian Trust has opened two branches since 2013.

With such variation in member demographics, the credit union’s chief experience officer, Ed Beckmann, admits it can be challenging to create a uniform message that resonates.

How Do You Compare?

Check out Meridian Trust’s performance profile on Search Analyze. Then build your own peer group and browse performance reports for more insightful comparisons.

According to Beckmann, the credit union’s historical marketing strategy was to roll out a single campaign across all its markets. But that’s not the future for Meridian Trust.

With the differences in these markets the variances in income, education, and awareness we’re finding it’s better to treat them differently, Beckmann says.

The credit union is now changing the graphics on promotions to better reflect the priorities of its different areas. For example, Scottsbluff is principally a town of borrowers and young families, Beckmann says, whereas Jackson tends toward the more established, upscale families.

We’re not changing what we’re offering, Beckmann says. Just how we’re presenting it.

The local customization of each campaign comes courtesy of Meridian Trust’s in-house marketing team. And though Beckmann admits it can be tough on the department, he says in the long term it is the right thing to do.

BEST PRACTICE: Make It Personal

Meridian Trust’s branch footprint stretches across several distinct geographic areas. Because different areas house different members with different needs, customizing marketing messages across regions has become an imperative.

We are never satisfied. Even if we’ve come up with something we’re happy with, we still ask what can we do better?”

The Kaizen Philosophy: Operations Edition

When working on his MBA from the University of Notre Dame, Rutar took a class on lean thinking and operations. That’s when he discovered kaizen, the Japanese business philosophy of continuously improving working practices, personal efficiency, and more.

Although the philosophy is mainly applied to manufacturing processes, Rutar uses it in his world of financial services, too. That’s why Meridian Trust’s products, services, and vendor relationships receive constant scrutiny.

We look at where there is waste in the system and what changes can reduce or eliminate that waste, CLO Rutar says.

Rutar joined the institution in 2014 and has since helped the credit union make several improvements to its operations. One involved updating the old consumer and mortgage lending platforms.

We were spending a lot of IT and loan department time trying to make these systems work for us, Rutar says. So we spent a few dollars and got a good platform.

At the end of August 2016, the credit union launched an online mortgage loan platform and signed up for a program called Webcaster, which feeds mortgage application information entered online directly through to the credit union’s new lending platform. There, Meridian Trust picks up the application, decisions it quickly, and notifies the member.

We wanted to provide service in an area in which we weren’t competitive, Rutar says. If a member wanted a mortgage or a HELOC, they would have to complete a paper application, come in to speak with a mortgage loan officer, or call. It was pretty cumbersome and limited to our 9-5 hours.

Meridian Trust uses Symitar for its mobile banking. Find your next partner in Callahan’s online Buyer’s Guide. Browse hundreds of supplier profiles by name, keyword, or service area. Start today at CreditUnions.com/connect/buyers-guide.

Now, the credit union is looking to improve its document operations.

Meridian Trust currently uses a third-party document provider that requires it to manually enter application information a slow process that is prone to error. With a document provider that plugs in directly to its loan platforms, it could enter application information once and automatically generate documents.

We’re taking a mortgage process that could take 60 to 90 minutes from application through document generation down to 30 minutes, Rutar says.

Finally, the credit union is updating its mobile app again.

The credit union revamped its mobile application in August 2014 and over the next two years added capabilities such as fingerprint ID and card controls.

The credit union is now migrating its in-house Symitar Episys core processing platform to Symitar’s service bureau and has decided it also makes sense to convert to the company’s mobile platform, too, with an eye toward better integration and service.

We are never satisfied, Beckmann says. Even if we’ve come up with something we’re happy with, we still ask what can we do better?’

BEST PRACTICE: Sync It Up

Technology is a necessity, but it shouldn’t be a burden. By creating synergies between product and service offerings, Meridian Trust has found an upfront investment in technology was worth eliminating the problems caused by trying to get different systems to work together.

The Kaizen Philosophy: Product Edition

The credit union applies that philosophy of continuous self-improvement to its product offerings as well.

A Heap Of HELOCS

For example, when Meridian Trust was looking for a way to manage interest rate risk in 2014 when interest rates were low but the potential for a rate hike was strong it looked to a revamped HELOC.

At the time, it carried $7 million in its HELOC portfolio, but rather than simply push that product harder, Meridian Trust devised a new HELOC structure one that allows it to provide a service to members while steering clear of booking a number of long-term mortgages

In the new HELOC, the introductory rate remains at 1.99% for the first 12 months. After the first year, and every year on the anniversary of the note, Meridian Trust resets the rate to the Wall Street Prime Rate, which at press time was 3.50%.

We monitor those each month to make sure we are pricing them appropriately, says Rutar, the CLO. And in our market, 3.50% is still a competitive rate.

The product has a 10-year draw period. Once that expires, the member has 20 years to repay the obligation.

According to Rutar, the credit union wanted to double its HELOC portfolio by fall 2016. By July 2016, the portfolio had quadrupled to $35 million. And as the introductory rates reprice, the credit union gets a boost to its net income. That, Rutar says, will only continue.

The HELOC has been so successful that Meridian Trust has hired an additional mortgage loan officer and two mortgage loan processors who reach out to local real estate agents and increase awareness of the product.

Thinking Big Balances

With an improved HELOC program on the book, Meridian Trust has now turned to increasing balances in its $12 million credit card portfolio. Specifically, it wants to increase balances by $1 million or 9% in 2016.

To do this, the credit union is rolling out three changes to its two Classic and Platinum credit cards.

First, the credit union is offering more attractive interest rates. It gave all new consumer credit cards opened between Nov. 1, 2015, and Oct. 31, 2016, a 0.00% introductory 12-month APR on purchases and 2.99% for balance transfers. After 12 months, both rates reset: 9.90% for Platinum and 12.90% for Classic cards.

For members not attracted by low rates, the credit union is adding a rewards element to its Platinum card and increasing the credit limits of its best card users.

If our members don’t carry a balance, they don’t care about the 0% or whatever interest rate, Rutar says. They want a reward for using it.

For the rewards program, members who purchase $1,000 through their Platinum card during the first 60 months will receive $100 cash back via a gift card or in travel perks.

For the credit limit increase, Meridian Trust will offer a balance increase of 15-20% to members who have never missed a payment, actively use the card, have had it open for a designated period of time, and have not experienced credit score deterioration.

As of press time, the credit union has not yet implemented the rewards or credit limit increase, however, the attractiveness of the offerings along with a clever marketing campaign featuring a Super Zero character helped Meridian Trust hit its 2016 $1 million growth goal by July 2016.

Super Zero, the interest rate super hero, helped Meridian Trust meet its credit card balance growth goals even before it rolled out a full array of new incentives. Image courtesy of Meridian Trust FCU.

We’re never about making minor tweaks and pushing our current products, says Beckmann, the chief experience officer. We ask what we can do to this product to make it better.

BEST PRACTICE: Make It Better

Meridian Trust is a full-service credit union with a variety of products and services. But just because members apply for loans or use mobile banking, for example, doesn’t mean it can’t improve those areas. Meridian Trust takes the stance that just because something isn’t broken doesn’t mean it can’t be better.

We’ve done this a few times; we’ve seen the booms and busts.

Driving Into Scottsbluff

As of second quarter 2016, membership growth at Meridian Trust was 8.1%, well above the asset-based peer average of 2.7%. But through 2011 and 2012, the credit union lagged behind asset-based peers in this metric.

It was around the close of 2012 that CEO Withers considered a geographic expansion. The underserved area of Scottsbluff, NE, quickly moved to the top of the list.

Meridian Trust petitioned the NCUA for an extended field of membership, which required the credit union to develop a three-year plan outlining marketing and growth strategies, and found a turnkey branch location in a high-trafficked complex next to the offices of a State Farm agent, professional life counselors, physical therapists, and a state senator.

We came in and slapped some paint on the walls, added new carpet, upgraded the surveillance systems, and installed an ATM, says Karen Woodul, the credit union’s senior vice president of operations. That ATM is one of two in the area.

Since the branch opened in August 2013, the credit union’s member growth has trended up and is now well above peer average.

Meridian Trust hired locally for its branch staff, which includes a branch manager, loan officer, and teller. It was a challenge, Woodul says, because the talent pool was small. But finding the right local talent was important.

It’s a pretty tight-knit community, she says. We felt if we brought in outside employees, the branch wouldn’t do as well.

Despite best-laid plans and the approved field of membership expansion, there was an issue.

The branch location wasn’t within the underserved census tracts that composed the new FOM as designated by the NCUA. And because the regulator required the credit union’s physical presence in the FOM, Meridian Trust had to get creative and mobile.

In late 2013, Meridian Trust introduced a Nebraska-based, fully functional mobile branch with an ATM and two laptops with access to the credit union’s entire core system. Mobile branch tellers can open accounts and process loans. After hours, the credit union locks up the branch and uses a generator to power the ATM.

It looks like an RV and is built with a Ford F-350 engine so credit union employees don’t need a Class D license to drive it.

It even has a name. And a gender.

His name is Moby, Woodul says.

Welcome to Wyoming, Moby. Representatives of Meridian Trust FCU pose with the mobile branch as they re-enter the Cowboy State. Photo courtesy of Meridian Trust FCU.

There’s a garage in Scottsbluff, within the underseved census tracts, where the credit union keeps Moby, thereby satisfying the NCUA’s field of membership requirement. But Moby is mobile, and the credit union drives it back and forth across the border frequently.

From Rawlins and Torrington in Wyoming to Scottsbluff and Kimball in Nebraska, Moby is a popular attraction all over the credit union’s footprint. In fact, according to CEO Withers, Moby inspired executives from a bank in the Dominican Republic that Meridian Trust recently hosted to create a mobile branch with eight tellers.

Moby runs on a set monthly schedule, and members can find the mobile branch’s schedule on the credit union’s website, posted in brick-and-mortar branches, and in their email inboxes. This reliability is something the credit union’s membership takes seriously.

We missed one of our dates and got in trouble with a member, Woodul recalls. It hasn’t happened again.

In addition to the member service benefits, Moby drives awareness for the credit union. Case in point, prior to Moby and the credit union’s first Scottsbluff branch, Meridian Trust was unknown to that part of western Nebraska.

They’d never heard of us, says experience officer Beckmann. We started from scratch there.

BEST PRACTICE: When Opportunities Arise, Take Them

Meridian Trust jumped at the chance to move into Nebraska. But when it realized its turnkey branch didn’t satisfy the NCUA’s field of membership requirements, the credit union had to be nimble and creative in its operations. The result, Moby, might be one of the credit union’s most popular and recognizable attractions.

A Merger In The Nebraskan Panhandle

Meridian Trust’s presence in Scottsbluff paid off in a big way when the NCUA approached the credit union with an opportunity in the summer of 2015.

Panhandle Co-Op Credit Union, based in Scottsbluff, was hurting. A fraud claim, near subprime lending practices, and several high-dollar losses led the sole-sponsorship credit union into financial trouble and NCUA supervision.

Although Meridian Trust was not aggressively looking to merge, according to Withers, the 26,000-member credit union saw potential in the $3.5 million, 900-member Panhandle Co-Op.

It was a sole sponsorship of the Panhandle Co-Op Association, Withers says. That association has more than 20,000 members. This was a way to complement our Scottsbluff branch.

The merger was finalized on April 1, 2016, making Meridian Trust the largest financial institution in the Nebraska Panhandle.

It’s a market that has been underserved by financial institutions for a long time, CLO Rutar says. We’ve been able to shake things up by moving in and offering competitive products.

According to Withers, Panhandle Co-Op was essentially a two-product credit union that focused on auto and signature loans.

Meridian Trust, on the other hand, is a full-service institution that has embedded itself into its new community. According to operations VP Woodul, who oversees four branches, including both Scottsbluff locations, Meridian Trust has grown by more than $21 million in loans in its three years in Nebraska.

A large portion of that business has come from indirect lending. The credit union has approximately 60 dealer relationships across its footprint, and two of its top 10 dealers operate in Scottsbluff.

When we went into Scottsbluff, indirect loans were low-hanging fruit, Rutar says. There weren’t that many competitors.

But like many financial institutions that participate in indirect lending, Meridian Trust wants to deepen those relationships. The credit union educates dealers on Meridian Trust products and provides them with new member applications. Additionally, the credit union sends introductory letters to all new indirect members and at some point in 2017 plans to replace those letters with a soon-to-be-produced introductory video.

We’re hoping technology will help us capture more wallet share, Rutar says.

However, there is a limit on how much indirect lending the credit union will tolerate.

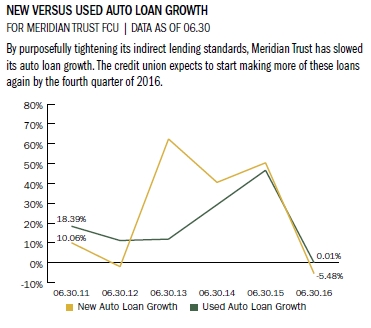

In the second quarter of 2016, Meridian Trust posted negative auto loan growth. That’s a notably weaker performance compared with the first quarter of 2015 when it posted 60.41% total auto loan growth.

According to CLO Rutar, that’s because the credit union is tightening its indirect business. Since second quarter 2015, Meridian Trust has shrunk its indirect portfolio by $7 million, or more than 20%, according to data from Callahan Associates. As a percentage of total auto loans, indirect loans made up 40.5% of the portfolio at second quarter, down from a high of 48.5% in second quarter 2015 and well under the asset-based peer average of 52.0%.

Meridian Trust sets product portfolio concentration limits based on its net worth or asset size. For indirect loans, Meridian Trust has its concentration limit set at 15% of assets. At its highest, in the second quarter of 2015, indirect loans made up 13% of the institution’s assets. By second quarter 2016, that ratio had fallen to 10%.

Meridian Trust did not stop making indirect loans; rather, it increased rates, set stricter underwriting guidelines, and decreased the allowed advance limit it paid its dealer partners. But these are temporary changes, Rutar stresses, and by fourth quarter 2016, he expects the credit union’s concentration limit to reach a point where he’ll feel comfortable making more of these loans.

According to Rutar, that’s one of benefits of indirect lending.

You can turn it off and on as you need to, he says.

BEST PRACTICE: Everything In Moderation

When Meridian Trust moved into Nebraska, indirect lending was a powerful tool. But the credit union recognized possible risk concentration within this difficult to cross-sell portfolio and set concentration limits by which it now abides.

The Future For The Economy. The future for Credit Union Members.

There’s another change on the credit union’s horizon, though it has more to do with the future of Wyoming’s economy than anything else.

According to the U.S. Energy Information Administration, Wyoming ranks second behind Texas in terms of total energy production. Wyoming is the country’s largest producer of coal, fifth-largest producer of natural gas, and eighth-largest producer of crude oil. Historically, coal, gas, oil, and trona production has created high-paying jobs and industry taxes have helped fund the state’s government, which does not collect an individual or corporate income tax.

But domestic changes in policy and international shifts in supply have disrupted the status quo.

Wyoming’s coal producers which collectively produce 40% of the nation’s coal have laid off thousands of workers, and some have filed for bankruptcy, citing the cost of meeting federal clean coal standards. If resource production continues to decelerate, Wyoming’s state government might experience income shortfalls and layoffs itself.

We’re concerned about coal and anything else that is mined from the ground, Rutar says.

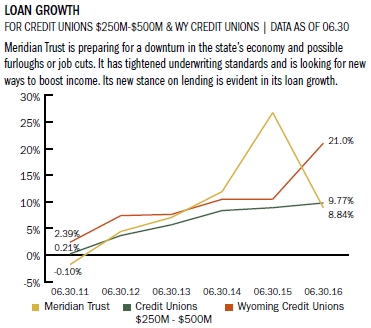

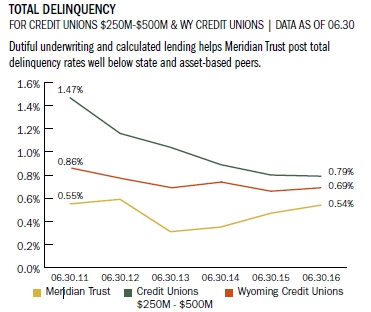

That said, Meridian Trust is well positioned should economic trouble continue, and operationally the credit union is already preparing to serve affected members.

Underwriting standards, if not stricter, are now a little more thorough.

We want to make sure we’re not loaning vehicles to an 18-year-old first-time oil field worker who might make a lot of money but doesn’t realize if the industry goes away, then he’s going to have trouble making those payments, says the credit union’s chief financial officer, Joani Hafner.

Meridian Trust has made a concerted effort to control costs and boost income. The credit union’s second quarter ROA of 0.83% rests far and above the 0.57% posted by asset-based peers.

One way it has boosted income without absorbing too much undue interest rate risk is by partnering with Sun Trust Bank to sell mortgages onto the secondary market.

Meridian Trust had sold mortgages in the past, but the process wasn’t always transparent, according to Rutar. For example, the credit union wasn’t always aware if a member had a question or a problem.

Through its October 2015 partnership with Sun Trust, the bank underwrites the loan and services it after Meridian Trust closes it. But the credit union better controls the process and is able to build deeper relationships.

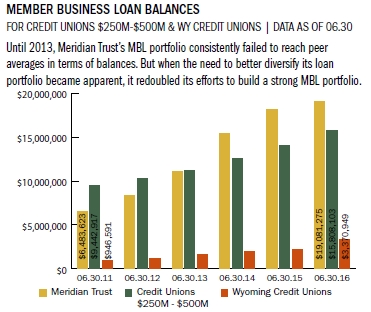

Another way the credit union has decreased its risk is by re-engaging its member business lending.

Until 2013, the credit union’s MBL portfolio consistently failed to reach peer averages in terms of balances. But when the need to better diversify its loan portfolio became apparent, it redoubled its efforts to build a strong MBL portfolio.

According to Hafner, member business loans generally take the form of rental property, such as fourplexes, small mom-and-pop stores, and farm equipment. At second quarter 2016, Meridian Trust’s $19 million in MBL balances bested its peer average of $16 million while net charge-offs and delinquencies remained at 0%. And the portfolio continues to trend north.

We set a goal to hit $22 million in balances by the end of 2016, Rutar says. It’s an area we’ll be interested in going forward.

The results of the November election will help clarify the economic outlook of the state, but for the time being, the future of Wyoming’s economy is a frequent talking point among both executive and branch-level employees.

We talk about it in board meetings, asset liability management meetings, loan meetings, and branch operations meetings, CFO Hafner says. It’s a topic of discussion across the credit union multiple times per month.

Should economic troubles persist, Meridian Trust is capitalized well enough to weather potential losses. Its risk-based capital and net worth ratios are at 18.2% and 10.8%, respectively, safely stronger than well-capitalized.

But then, it’s not as if the credit union is unfamiliar with the booms and busts befitting a state so entrenched in natural resource production. As the oil crisis in the 1970s taught the credit union, geographic and SEG diversification can help the institution overcome hits to a single industry.

And more than three decades later, Meridian Trust learned another hard lesson.

In 2013, automatic spending cuts to the U.S. federal government totaled approximately $85 billion. Federal pay rates were unaffected, but the sequestration resulted in involuntary unpaid time off.

Wyoming felt the impact, and to help its affected members bridge the gaps in income, Meridian Trust started offering a furlough microloan product with a 12-month introductory 0% rate and a maximum total loan balance of $2,500, which the credit union can adjust on a case-by-case basis.

It still offers that loan today, though the use has evolved. For example, when flooding in May of this year damaged homes and offices in Lander, WY, the credit union increased the maximum loan balance on the microloan for members who produced pictures of their damage and estimates for repairs.

But as government and natural resource industry layoffs loom, these sequestration loans, as CLO Rutar calls them, might again fulfill their original purpose.

All in all, CEO Withers feels confident both in the state’s ability to weather the economic storm and the credit union’s profitability and ability to lend.

And why not? This is Wyoming. The people here know the drill.

We’ve done this a few times; we’ve seen the booms and busts, Withers says. We’ve tightened some things, but I’m optimistic. Like the farmer says, next year’s crop is always the best you’ll ever have.