Read the full analysis or skip to the section you want to read by clicking on the links below.

LENDING AUTO LENDING MORTGAGE LENDING CREDIT CARDS MEMBER BUSINESS LENDING SHARES INVESTMENTS MEMBER RELATIONSHIPS EARNINGS SPECIAL SECTION: CUSOS

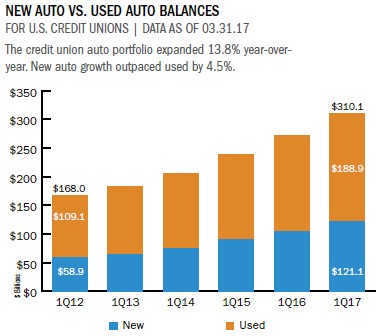

Auto loans, the second-largest component of the credit union loan portfolio, expanded 13.8% over the past 12 months. New auto loan balances increased 16.6% to $121.1 billion; used auto loans increased 12.1% to $188.9 billion as of March 31, 2017. Although still representing a larger balance, the share of used auto loans in the auto portfolio has declined more than 4 percentage points from 65.0% in the first quarter of 2012 to 60.9% as of March 31, 2017.

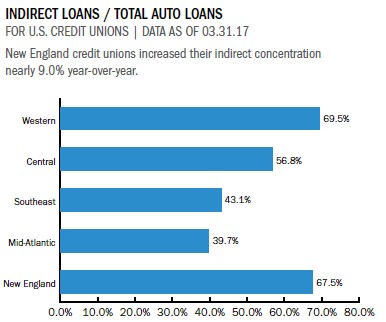

Indirect lending has become an attractive way for credit unions to spur growth in their auto portfolios. The share of indirect loans in the credit union auto portfolio has grown from 18.4% as of March 31, 2004 when the 5300 Call Report started recording data on indirect lending to 56.0% as of March 31, 2017. That’s a 37.6-percentage-point increase in 13 years.

During this time, the number of institutions par ticipating in indirect lending has increased from 1,235 to 1,947. In first quarter 2017, credit unions in the NCUA’s New England region reported the highest percentage of indirect loans to auto loans, 67.5%, whereas the Mid-Atlantic region reported the lowest, 39.7%.

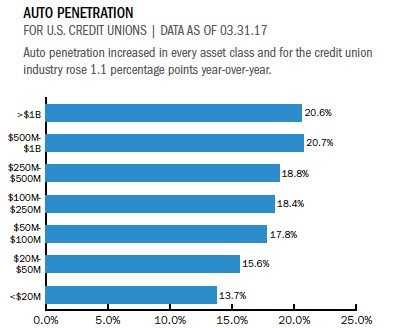

Credit union auto market share increased 84 basis points year-overyear to 18.8%, according to data from Experian Automotive. Data from Callahan Associates shows the percentage of members that have an auto loan with a credit union, also known as auto penetration, has also increased from 18.6% in first quarter 2016 to 19.7% in first quarter 2017. Every single asset class posted gains over the past year. Auto penetration rates ranged from 13.7% for credit unions with less than $20 million in assets to 20.6% for credit unions with more than $1 billion in assets.

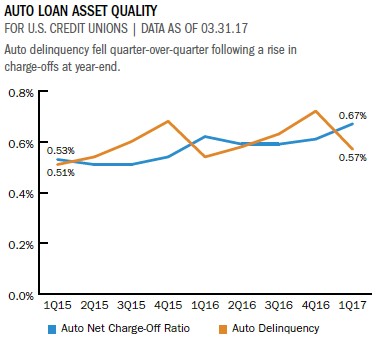

Although delinquency in the credit union loan portfolio fell 2 basis points in the past 12 months, delinquency in auto loans increased 3 basis points to 0.57%. This still remains well below other consumer lending products, such as credit cards and student loans.

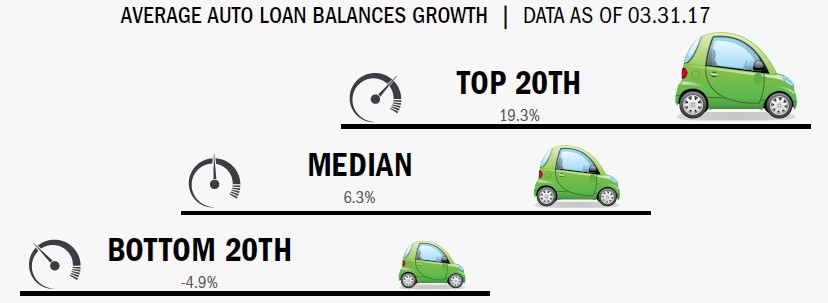

Click the graphs below to enlarge and then continue reading to see how ABECU makes a nice business out of a lease-like product.

Large lenders turned out notable success in auto lending throughout the rst quarter of 2017, driving the average auto balance growth rate to 13.8% for the industry. Median auto growth was 6.3%. The top 20th and bottom 20th percentiles expanded 19.3% and -4.9%,

CASE STUDY

ANHEUSER-BUSCH EMPLOYEES CREDIT UNION

Anheuser-Busch Employees Credit Union has brewed up a niche in balloon lending for automobiles.

The loans work much like a lease, with lower monthly payments and a balloon payment at a guaranteed future value at the end. But there’s a big difference.

The member actually owns the car, says Janice Bruno, vice president of indirect lending at ABECU, which has more than 2,600 of the loans.

The balloon notes represent approximately $71 million of a $676.7 million auto portfolio and attract a certain kind of borrower, Bruno says.

Our Value Plus loan works for the person who is looking for a lower payment, the person who likes to get a new car often or who wants that more expensive vehicle but not the large payment, Bruno says. It can also help the person who’s upside down on their trade-in.

Like a lease, borrowers choose a maximum amount of mileage a year they plan to drive ― up to 18,000 miles a year for up to five years at ABECU ― and can turn the vehicles back in to the credit union or re-finance at the end of the term.

But unlike a lease, they can refinance, pay off, sell, or trade in the vehicle, and there’s no security deposit, acquisition fee, or pre-payment penalties.

The loans are available for new and used vehicles and offered through direct and indirect channels. Members can apply online for the balloon loan or access it at the credit union’s network of dealers.

ABECU’s online calculator shows that a $25,000 balloon note for 60 months at 12,000 miles a year would cost $491 a month with a 2.34% conventional loan and $348 a month as a Value Plus balloon loan.

Read The Whole Story

RETURN TO INDUSTRY PERFORMANCE BY THE NUMBERS 1Q 2017