Top-Level Takeaways

-

Alliant Credit Union formed a committee of stakeholders from across the credit union to guide a large, transformational effort to modernize its lending system.

-

A new consumer loan origination system has helped Alliant reduce decision rules, close credit card applications faster, and fund car loans on the same day.

Alliant Credit Union ($9.7B, Chicago, IL) is rewriting the rule book for loan processing, shrinking it in the process.

In the past decade, the Prairie State cooperative has grown from a single-SEG credit union serving United Airlines to the largest credit union in Illinois. As such, its software and processes must accommodate a multi-SEG, multi-community credit union that has just crossed the $10 billion asset line.

CU QUICK FACTS

Alliant Credit Union

Data as of 12.31.17

HQ: Chicago, IL

ASSETS: $9.7B

MEMBERS: 385,302

BRANCHES: 12

12-MO SHARE GROWTH: 4.8%

12-MO LOAN GROWTH: 12.9%

ROA: 0.74%

As we grew and changed our focus, we needed to give our users access to everything they needed for the loan process without having to talk to anyone, says Jeremy Pinard, Alliant’s vice president of consumer lending.

Today, Alliant is in the final stages of deploying a consumer loan origination system (CLOS) that has helped the credit union reduce the number of decision rules per loan product by more than 25%, close credit card applications in 30 minutes, and fund car loans the same day. The credit union also can now connect with all the major credit bureaus, rather than hard coding into just one, and can change rates on the fly.

ContentMiddleAd

A Better Member Experience

To ensure its new lending platform would adequately serve its needs, Alliant brought in stakeholders from across the credit union for plenty of talking.

It was the first time we created a war room, put bodies in there, and dedicated them to a project like this, Pinard says. At one point, we had 20 people in there.

In 2014, senior managers began considering the very large, transformational effort that would be needed to modernize its lending system that was both too manual and relied on software that was no longer supported.

We did a business case that looked at what our financial return would be and how long it would take, Pinard says. We’re well on track with that. But the bigger point is that we’re taking the organization to another level with the member experience.

Click to see a screenshot example of the new Alliant CLOS in action.

For example, Alliant’s previous system used a complicated waterfall decision tree that made it difficult to approve loans, says John Listak, Alliant’s lending systems project manager. A loan application from a member who had one delinquency 24 months ago would be deferred to a human being.

The new system which uses an Agile Scrum software development framework and the FICO Origination Manager decision engine to run calculations, determine rates, and approve or deny loans quickly looks at multiple fundamental data points, including FICO scores and reports from multiple credit bureaus.

We have hundreds if not thousands of data points that we can capture and report on, Listak says. We’ve gone to a new level in our ability to track and provide audit trails and follow and manage our risk.

That’s no small benefit for a credit union that must accommodate the new reporting requirements that come with crossing $10 billion in assets.

Take Learning To The Next Level

Like what you’re reading? Callahan’s Media Suite subscription provides deeper insight to help credit unions thrive. Unlock expanded access to CreditUnions.com, Search Analyze, and Callahan’s industry publications today.

Members also now get email alerts and can easily follow the loan process online or through a mobile app. Plus, they can communicate with someone at Alliant through the app if they need to, and the people at the other end have more visibility into the process, too.

All the history is right there, says Pinard, the lending vice president. It has improved the experience for the consumer and the internal users. We’re not seeing as many complaints now that so much of the friction in the application process is no longer there.

Click the tabs below to view graphs.

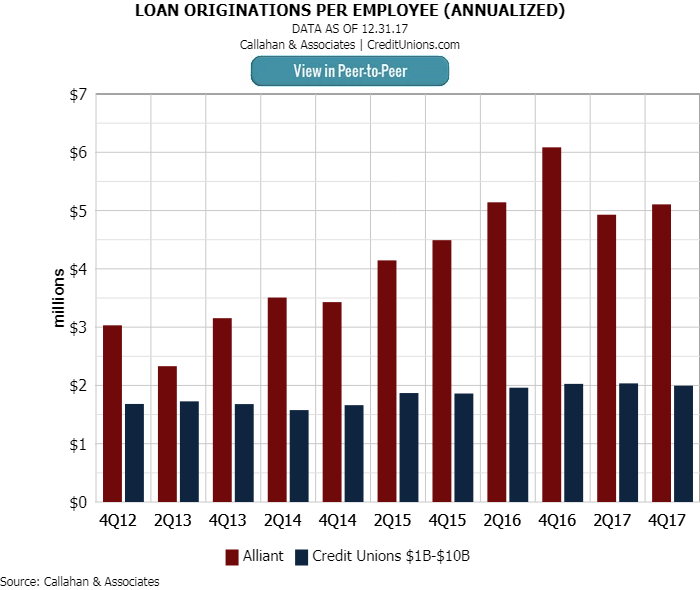

ANNUALIZED LOAN ORIGINATIONS PER EMPLOYEE

In the fourth quarter of 2017, Alliant reported $5.1 million in loan originations per employee and ranked at No. 6 in this metric for credit unions with $1 billion to $10 billion in assets.

LOAN INCOME PER FTE

Alliant generated $490,732 per each of its 498 FTEs in the fourth quarter. The average was $158,078 for credit unions $1 billion to $10 billion in assets and $143,943 for credit unions nationwide.

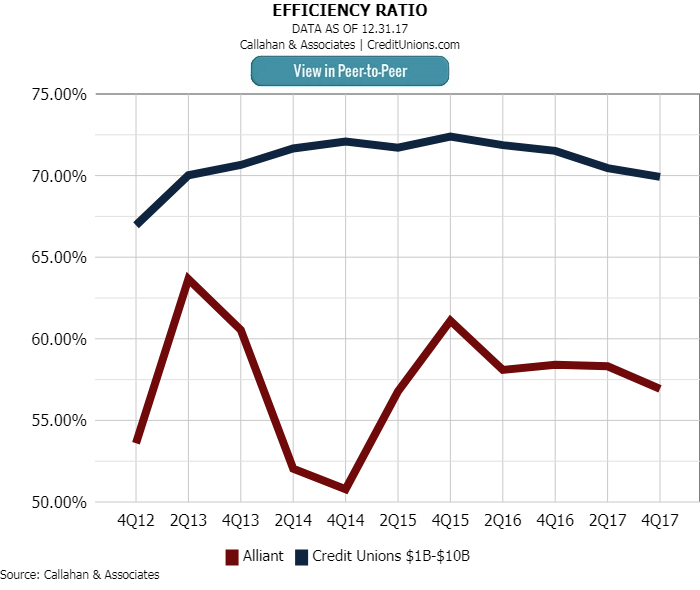

EFFICIENCY RATIO

Alliant’s fourth-quarter efficiency ratio of 56.93% placed it among the top 10% of its asset-based peer group.

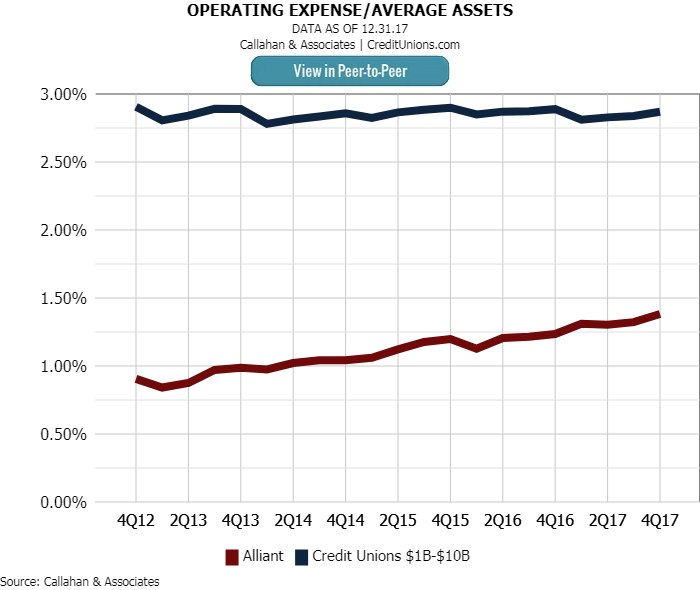

OPERATING EXPENSE/ AVERAGE ASSETS

Compared to the average billion-dollar credit union, Alliant spends less to operate its business.

AVERAGE SALARY BENEFITS/ EMPLOYEE

Alliant paid more in average salary and benefits per employee, $128,363, than all but two credit unions in its asset class in the fourth quarter of 2017. Only New York’s United Nations FCU ($130,841) and California’s Star One Credit Union ($173,528) paid more.

$(‘.collapse’).collapse()

Better Results

Alliant started using the new CLOS for auto loans and credit cards in late 2016. It then added home equity products in October 2017 and RV loans in February 2018. It will start running unsecured loans through the system later this year. The current mortgage and commercial loan systems will remain although there has been some discussion about replacing the latter.

In raw numbers, the credit union has taken more than 72,000 applications through the new origination system and funded more than 28,000 of those applications for more than $500 million. But these numbers are not the only measure of success.

In our previous system, we were around 25% look-to-book, Pinard says. In our new CLOS, we’re up to almost 40% look-to-book in all our consumer lending products combined.

Top Of Mind For This CLOS

Here are the top four priorities that Alliant determined it would need in its new CLOS:

- Omni-channel experience

- Secure digital document management functionality for both internal and external users

- Creation of a museum-quality and inspection-ready digital consumer loan package

- Secure digital internal and external communication functionality

- Full integration with third-party systems, including Allied, DocuSign, FedEx, First American, FIS (IDA, IDV, OFAC, QualiFile), FICO OM-DM decision engine, NADA Guides, Equifax, Experian, TransUnion, OnBase, and Symitar.

That’s a pretty efficient rate, even for a credit union that already stands out for its productivity. For example, Alliant serves 774 members per full-time equivalent employee, compared with 385 for credit unions nationwide. And its members, many of them employees of United Airlines, maintain a sharply higher average loan balance than the national average for credit unions $32,982 versus $15,761, respectively.

But the credit union is not stopping here. Alliant took a multi-disciplinary approach to develop the new CLOS, and it is continuing that approach in the form of an independent development team that focuses on enhancements, product support, and compliance.

I love this part of it, Pinard says. We have people from our business and IT teams sit together and work to make sure that this product doesn’t just sit on the shelf, wither, and die.