Top-Level Takeaways

- Wings Financial Credit Union offers competitive mortgage rates and other perks to make its repricing program appealing to current mortgage holders.

- The program not only draws in borrowers but also increases overall member satisfaction.

- The credit union can adjust its repricing strategies if necessary to maintain a balance between competitiveness and profitability.

For as challenging as the mortgage market is for credit unions, it’s even worse for consumers.

Rather than simply waiting for the market to improve, Wings Financial Credit Union ($9.7B, Apple Valley, MN) took a proactive approach, launching a repricing promotion aimed at borrowers who were being locked out of refinancing or purchasing a new home.

“We initiated the program in November of 2023 with the goal of moving existing mortgages held in our portfolio from a sub-3% rate to something closer to current market rates at the time,” says Lia Patino, the Twin Cities cooperative’s vice president of mortgage lending. “We were looking for a program that would benefit the balance sheet while also providing value to our members.”

With interest rates soaring above 7%, touching 8% at times, convincing homeowners to relinquish their coveted 2.75% interest rates was no small feat, Patino acknowledges. But Wings found an angle that appealed to some.

“We knew there had to be members that were considering moving or taking equity out of their home but were waiting for the rate environment to change,” says Patino, a 14-year employee at Wings who has overseen mortgage lending for the past two. “We just had to figure out what that offer was.”

Exclusive Member Perk

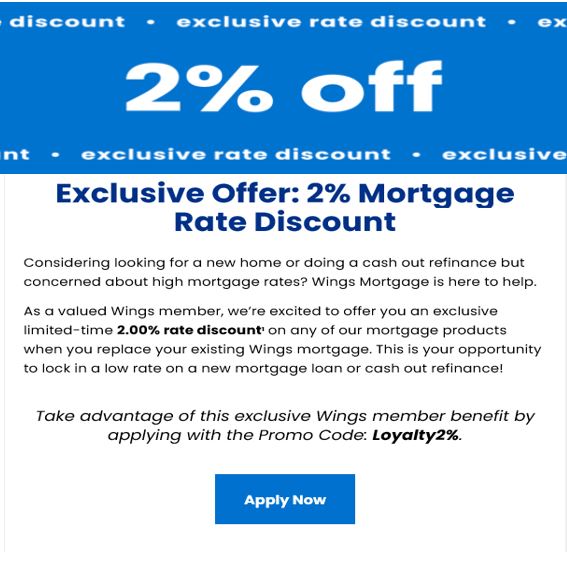

That offer, Wings discovered, was 200 basis points off current market rates plus a few other perks.

Wings deployed a highly targeted marketing campaign positioning the offer as a loyalty benefit. It targeted mortgages priced below 3% for the initial phase of the repricing program, assuming those would be the hardest to win over. Marketers also scrubbed the list for standard exclusions, Patino says, including delinquency, loans nearing payoff, and do not contact. From there, the remaining group was randomly split in half to gauge the level of interest for different offers.

The first email offered only the 2-percentage-point reduction. Patino says it garnered a 59% open rate — “a great result” — but only a 2% click-through rate, lower than expected. And no applications.

“When we delivered offers to the second group, we sweetened the deal by waiving the origination fee in addition to the rate reduction,” the mortgage VP says. “Additionally, we went back to the first group and presented this same offer. That is when we began to receive applications from both groups.”

The offer to the first group was valid for 45 days. The offer to both groups was valid for another 60 days.

“We were trying to determine what the members needed to feel the offer was significant enough for them to exit their current mortgage,” Patino says.

Where Are Untapped Mortgages In Your Market? Take a data-driven look at leaders and competitors in your financial market with Peer Suite. Backed by data from HMDA, the 5300 Call Report, and the U.S. Census Bureau, Peer offers endless opportunities to pull custom research to make strategic, member-driven decisions for your institution. Claim Your Mortgage Scorecard Today!

The Sweet Spot

Turns out, what some members needed was an attractively low rate and no origination fee. The emails garnered interest and generated a fair number of calls, and loan officers followed up with outbound calls of their own.

“When we were able to speak with the members to answer their questions and run scenarios for them, that often resulted in an application,” Patino says.

Although Wings’ initial outreach was met with some expected resistance, such as members expressing contentment with their current low rates or a lack of interest in moving or cashing out equity, there were also positive reactions.

“Some stated if they had not received this offer, they would not be purchasing a new home,” Patino says. “That was what we were hoping for — an offer that positively impacts our members’ lives while also benefiting the organization.”

As the program progresses, Wings continues to rack up deals that help members meet their own financial and housing goals while removing some particularly low-margin loans from the books.

“At last check, we had converted $8 million in loans,” Patino says. “But that number is still growing. We will begin our second campaign with the loans priced between 3-4% in the next 30 to 60 days.”

5 Ways To Fly High With Repricing

Wings Credit Union offers tried-and-true practices ripped from its own mortgage repricing.

- Be creative.

- Make the offer compelling enough for members to want to pay off a low-rate mortgage.

- Keep sending communications. Members might need to see the offer several times before they consider its possibilities.

- Engage loan officers during development. They provide perspective and insight senior leaders might not.

- Partner with marketing and compliance early.

This article originally appeared on CreditUnions.com on June 3, 2024.