MAPS CREDIT UNION ($460M, Salem, OR) does not measure the success of individual departments solely in terms of dollar revenue. The credit union also considers how well divisions support one another, the needs of members and the community, and the priorities of the overall organization. That holistic perspective helped the credit union embrace both the benefits and the challenges presented by its 2008 conversion to a community charter.

To counterbalance the membership and deposit growth resulting from the conversion which often exceeded the credit union’s intentions and expectations Maps became more focused on earnings, says Kevin Cole, the credit union’schief financial officer.

We didn’t have a lot of extra capital to start with in relation to our asset size, he says. Take that in conjunction with the corporate system expenses and an environment where every investment option adds interest rate riskand it was clear we needed to make sure we could generate enough capital to manage our growth.

We needed to make sure we could generate enough capital to manage our growth.

So the credit union embraced its cooperative principles and stepped up its competitiveness in areas where it had an institutional edge. In doing so, it uncovered untapped opportunities in six distinct areas: idea generation, consumer lending, high-value members, mortgages, commercial lending, and local businesses.

When I joined the board, there was a leave one another alone’ arrangement with other financial institutions, says Joe Phillippay, board chairman. But profit’ is not a dirty word. If we can do things thatwill improve our bottom line more aggressively, we should do them.

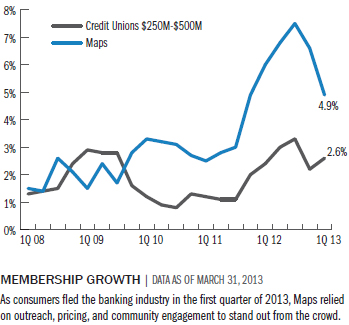

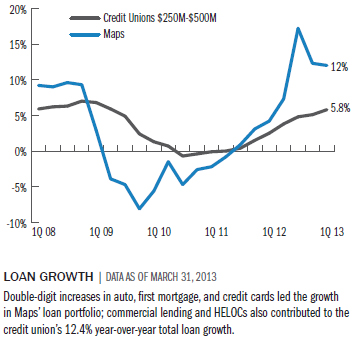

The new approach has contributed to a 12% annual increase in loan activity, a 2.8% increase in average member relationship, and an 0.84% ROA in first quarter 2013, according to Callahan & Associates’ Peer-to-Peer analytics.

INVEST IN BIG IDEAS

The employee culture of Maps is designed to favor democratic opportunity. To maintain open channels of communication and the accessibility of upper management, Maps offers a blog where employees can post questions and ideas or start credit union-relevantdiscussions. The credit union also uses a formalized group brainstorming session called the Idea Lab to elicit in-person comments and suggestions. Idea Lab topics have ranged from what new products or services to offer to what wouldmake an employee’s or a department’s job easier or more productive.

A lot of what has been coming from the Idea Lab lately has had to do with our core system upgrade, and we have added several things to the system as a result, says Barbara Cecil, human resources director. We address everything discussedin our Idea Lab in one way or another.

We address everything discussed in our idea lab in one way or another.

The credit union also looks to outside sources for inspiration, even if that means going to great lengths and distances. For example, front-line employees at Maps can apply for a chance to participate in a leadership program that sends them to three industryevents or learning initiatives throughout the year. The goal of the leadership program is to expand employees’ career paths and increase their knowledge of the cooperative system.

One employee took a trip to a Guatemalan cooperative through the World Council of Credit Union’s (WOCCU) international leadership exchange. The employee visited a credit union that has creative Credit Union Service Organization (CUSO) operations,including an amusement park and a grocery store that are only accessible to members. Maps is already a believer in the benefits of CUSOs, it operates or invests in 14 of them, and the employee was looking for best practices as well as new and interestingways to expand CUSO relationships.

The trip gave that employee a different appreciation for the role of a financial cooperative in a member’s life, says Jill Nowacki, official spokesperson and vice president of development at Maps. He learned a credit union canbe more than a place where people cash a check or make a deposit.

The credit union’s leadership program has tangible benefits for individual employee creativity, but it also has a positive ripple effect among other staff members.

Employees who come back from these trips tell friends and peers about their experience, Nowacki says.

That encourages others to get more involved.

SECURE BUY-IN TO BOOST CONSUMER LENDING

Auto lending remains a primary component of Map’s consumer lending portfolio. In first quarter 2013, it posted 29% annual growth for new vehicle loans and 24% annual growth for used autos. But the credit union didn’t achieve all of this growthworking by itself.

We have seen a great lift in awareness and activity from three recent buy local car sales, Nowacki says.

We went to our local car dealers and said, Let’s have one weekend where we encourage our consumers to buy here in Salem instead of traveling to Portland.’

The credit union has also posted impressive growth in its unsecured credit cards, with balances growing 16.6% year-over-year. This is partly the result of a Visa balance transfer promotion that included an employee incentive.

We offered employees who processed the transfers the ability to earn points just like members earn points for card transactions, says Traci Kendall, vice president of branch operations. At the end of the campaign, they were able touse their points to purchase prizes and products out of a catalog.

IDENTIFY AND PAMPER HIGH-VALUE MEMBERS

Four years ago, Maps launched a private client services department to work with its high-net worth, highdeposit balance members. The goals of the department have evolved with the changing financial environment, but it remains a valuable channel not onlyin its own right but also for its role in deepening member relationships across the portfolio.

About the time we started this department everything started changing in the financial services industry, says Pam Woodcock, director of private client services. Banks were going under and we started to see an influx of deposits,so we needed to slow down that activity.

In 2012, the department shifted its focus toward generating loans to counteract the deposit rush. Since then, it has continually found new ways for Maps to become a larger part of its high-value members’ lives. For example, it encourages them torefinance their homes or purchase new investment or commercial properties. It also develops relationships with area professionals such as CPAs, state planning attorneys, and financial planners to drive referrals.

Credit unions are not typically known for handling complex situations, Woodcock says. When you have a high net worth or are selfemployed, things are never black and white. These individuals often never thought of looking to a creditunion. One of our challenges was to turn that around.

During the program’s initial development, one local private estate planning attorney confessed Maps was at the bottom of his list simply for being a credit union and that he steered his clients away from the institution. Today, thisattorney is one of the department’s top clients and serves on Maps’ charitable foundation board.

For credit unions that want to establish a similar program, Woodcock says one of the most important differentiating factors a credit union can offer isn’t a product or service it’s the localized, accessible nature that is built intothe cooperative model.

When we started private client services, we spent a lot of time on relationship pricing and trying to determine what would draw this segment of the membership, she says. Over the years, we’ve learned for the most part price doesn’t matter. It’s all about the client wanting somebody local that can take care of problems or questions.

When unusual situations do arise, having immediate access to real decision makers in one centralized location makes a huge difference to these members.

We didn’t do irrevocable trusts before, but we had a situation come up and I asked well, why don’t we offer this?’ Woodcock says. If that client had gone into a branch with that request, the employee wouldhave looked up our guidelines, followed policy, and said we don’t do that. But these members know they won’t get that kind of a stock answer [from the private client services department].

Despite requiring additional service, high-value members return significant dividends, although not always in the form of dollars and cents. Other benefits such as increased community awareness and access to strategic partnerships thatresult from the program are priceless for a growing credit union.

High net worth members tend to be involved in the community, Woodcock says. They respond if they see Maps is giving back and is involved in what they care about.

STAY FLEXIBLE IN A CHALLENGING MORTGAGE MARKET

It can be a struggle for credit unions to increase awareness of their mortgage offerings, but gaining mortgage market share in and around Salem has been worth the fight for Maps.

Competition is stiff for quality loans, says Patty Walker, vice president of business and real estate lending and president of Maps Business Services CUSO. But mortgages are one of the best ways to get the word out about Maps.

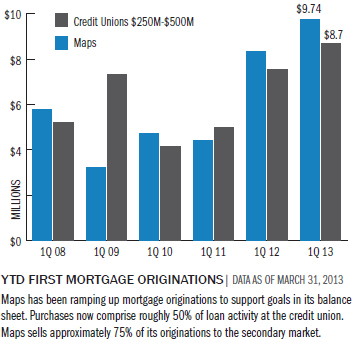

Today, Maps could sell almost every mortgage loan it makes on the secondary market. However, the credit union keeps roughly 25% of them in its portfolio either at the request of the member or to facilitate special circumstances.

We have members who don’t want their loans sold due to a past bad experience, Walker says. Other times the underwriting might take longer and would potentially create a timing issue with that purchase.

The credit union was historically more focused on refinances, but purchases now comprise 40% to 50% of its loan production.

Refis are great when rates are down, but you need to have a good balance of both refis and purchases, Walker says. So our loan officers network with local realtor associations to boost purchase activity.

Last year, the credit union increased its home equity portfolio by approximately $8 million. It is on track to repeat that growth again in 2013.

This was a little surprising to us because values here are still stabilizing, Walker says. It’s amazing how many members still have equity in their homes.

GET IN THE GAME WITH COMMERCIAL LENDING

Even before the credit union got into the mortgage market, it was involved in business lending.

Business lending is not inexpensive, says Walker, who was instrumental in establishing and growing this department in the early 2000s. It takes time and thought to put together a good program.

Maps’ commercial lending department grew rapidly, and the credit union soon pushed up against its business lending cap. To accommodate the demand for business loans Maps, along with seven other regional credit union investor partners, formed a multi-ownedCUSO called Willamette Business Group.

Growth has leveled out over the past few years, primarily due to hesitant business owners and hardhit property values. Still, the credit union is uncovering new clients and new opportunity, particularly in refinance. Maps’ specialty commercialreal estate includes a diverse mix of properties, including apartments, professional multi-use areas, and government facilities. And the credit union is investigating SBA lending in the future.

We hadn’t really considered SBA lending before because we had a robust program, Walker says. But now we feel like our members have a need for it.

To keep its pipeline full, the business services department relies on a range of resources. The credit union’s Advanced Reporting CUSO which provides tenant and pre-employment screening has been instrumental in building clientelelists and boosting loan activity. Other departments aid the effort as well. Cross-credit union cohesion is one reason Maps is so successful.

The business lending and mortgage departments work well together for cross referrals, Walker says. Our existing business folks are also some of our best private clients and 95% of the time they are looking for a mortgage as well.

SUPPORT LOCAL BUSINESSES

When you become a member of something, you shouldn’t feel like a customer, Nowacki says. You should get perks or bonuses for your membership.

Maps members take comfort in knowing the credit union also stimulates the local economy. Buy Local, the member rewards initiative of Maps, puts a distinct cooperative spin on the retailer discount concept made popular by companies such as Groupon, LivingSocial,and Scoutmob.

Here’s how it works: Maps and a local business partner offer a free product or service to members over a two-week period. The credit union covers the cost of the item or service. In return, the business offers a small, ongoing discount to customersthat use a Maps payment card for their purchase.

We’ve seen increased transaction volume, which then leads to increased interchange income for the credit union, Nowacki says. Our members are getting the chance to try different businesses and save money, and our local businessesare getting new customers.

Today, roughly 70 local businesses, from auto dealers to homemade soap shops, participate in the program. Maps was initially worried it might struggle to recruit enough partners to provide the 26 featured deals that would run over the course of each year.However, the demand for these partnerships is so strong that Maps has a waiting list that extends through the next calendar year.

Several Buy Local businesses have found the exposure so beneficial to their business that they report dropping other advertising options to invest more advertising funds into additional perks for Maps members. Whether it’s through one of its manyproducts or services, a strategic partnership, a second chance, or even just a smile and a willingness to listen, Maps knows its brand is only as strong as the sum of its parts.