A Capital Initiative At Fairfax County Credit Union

In 2010, Fairfax County Credit Union received supplemental capital from the U.S. Treasury. Here’s how it used those funds to improve the long-term health of the credit union and its membership.

Credit union leaders want to know where peers are placing their focus. These six priorities reflect how leadership teams are responding to change with intention and clarity.

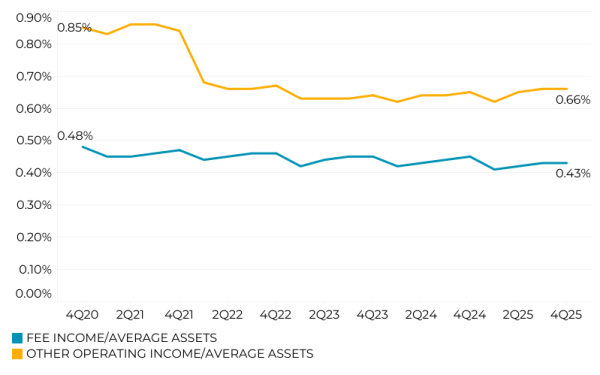

As margin support begins to fade, earnings performance is becoming more sensitive to revenue mix and harder to interpret through public reporting alone.

Harvard FCU combines digital estate planning with human financial guidance to support positive, proactive wealth transfer across generations.

Discover how small to midsize credit unions can weather the economic headwinds hitting their communities right now.

Look beyond the headlines to better understand what is driving current market trends and how they could impact credit union investment portfolios.

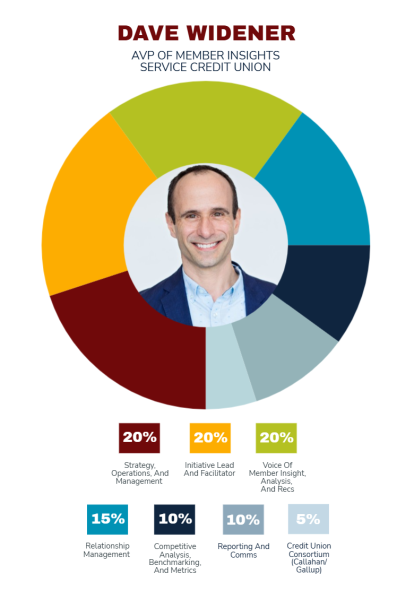

At Service Credit Union, Dave Widener connects data, strategy, and culture to shape better outcomes for members.

The Ohio-based cooperative has partnered with a fintech to offer fractional investing as part of its financial education curriculum in local schools.

Seven questions credit union board members should ask to ensure alignment on executive benefit plan goals.

As credit unions move from experimentation to adoption, leaders offer firsthand knowledge on what separates weak policies from strong ones that actually work.

How Members Cooperative focuses on structure, oversight, and clear expectations to ensure AI supports, not undermines, long term strategy.

Why Credit Unions Need Supplemental Capital