State In The Spotlight: Pennsylvania

Besting national averages across various penetration and efficiency rates, financial cooperatives in the Keystone State are efficiently serving members and expanding books of business with their current staffing models.

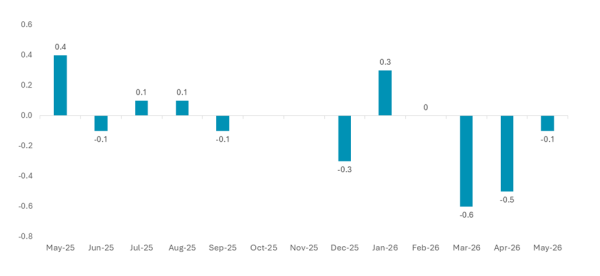

A Cash Cow 7 Years In The Making