JetStream FCU Turns CDFI Funding Into Lifelines After Hurricane Maria

A pair of CDFI grants allowed the Florida-based credit union to help members restart their lives on the island or relocate to the United States.

Members are anxious about their financial futures, even as credit unions remain financially strong. Institutions that respond to this moment can make 2026 a turning point.

Global events are flowing directly into household budgets, reshaping how credit union members save, borrow, and cope. Such trends don’t always show up in headline data.

Credit unions are benefiting from a rare margin advantage as loans reprice slower than deposits. The question now is how institutions will use that strength to better serve members.

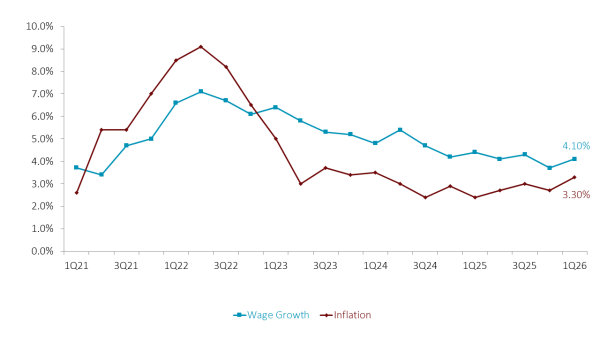

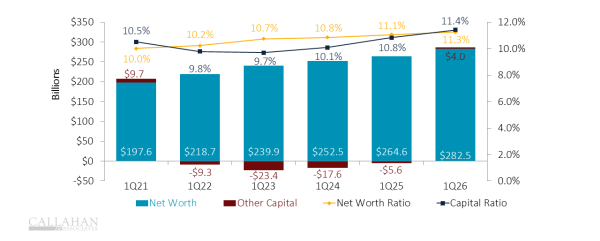

Inflation, war, and uncertain futures have reshaped members’ needs in 2026. What does credit union performance data from the first quarter of 2026 say about household budgets, inflation pressures, and more?

Look beyond the headlines to better understand what is driving current market trends and how they could impact credit union investment portfolios.

Today’s job market is shaped by skills based expectations, with employers slowing entry level hiring and placing greater emphasis on applied experience.

St. Cloud Financial is betting on digital assets to protect member relationships and future relevance. It’s picked up lessons for other leaders along the way.

Traditional risk tools alone aren’t enough. Portfolio protection must evolve to meet members within the lending experience itself.

The Ohio cooperative is refining the role of its foundation to clarify what belongs within the credit union and what belongs under its charitable arm, strengthening focus and long term strategy for both.

The credit union migrated its on-premises contact center and implemented workforce management software to maximize efficiency, minimize costs, and provide a better member experience.

RBC2: What Capital Problem?