Credit Card Balances Expand Through 2018

Delinquency in this portfolio remains the highest for any major credit union loan product.

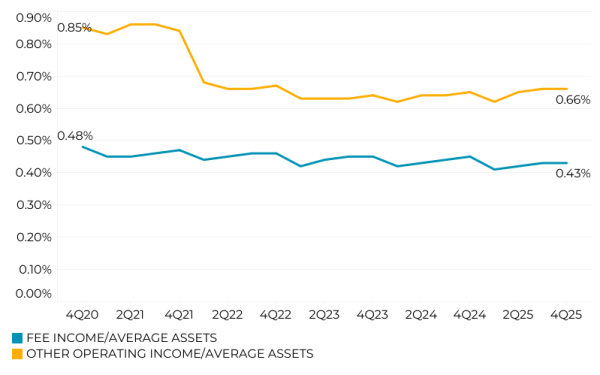

As margin support begins to fade, earnings performance is becoming more sensitive to revenue mix and harder to interpret through public reporting alone.

Discover how small to midsize credit unions can weather the economic headwinds hitting their communities right now.

Look beyond the headlines to better understand what is driving current market trends and how they could impact credit union investment portfolios.

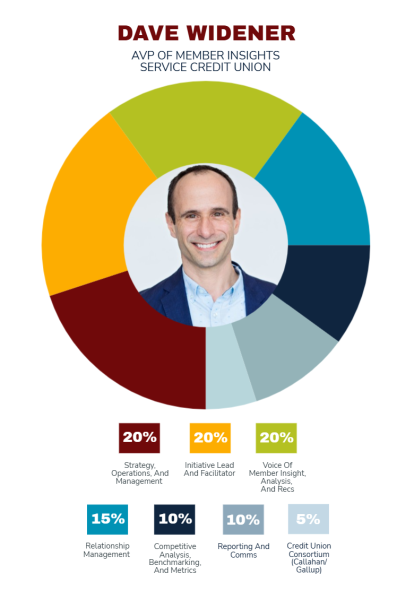

At Service Credit Union, Dave Widener connects data, strategy, and culture to shape better outcomes for members.

The Ohio-based cooperative has partnered with a fintech to offer fractional investing as part of its financial education curriculum in local schools.

Seven questions credit union board members should ask to ensure alignment on executive benefit plan goals.

As credit unions move from experimentation to adoption, leaders offer firsthand knowledge on what separates weak policies from strong ones that actually work.

How Members Cooperative focuses on structure, oversight, and clear expectations to ensure AI supports, not undermines, long term strategy.

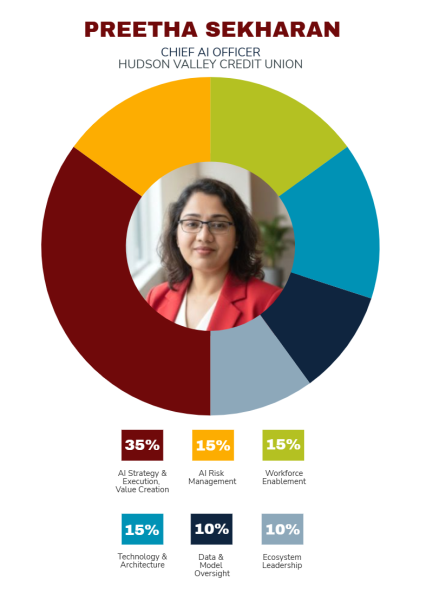

As Hudson Valley Credit Union’s artificial intelligence chief, Preetha Sekharan holds a rare role in the industry, but it’s one that is likely to become far more common in the future.

Artificial intelligence for credit unions has moved from a future concept to today’s full-fledged leadership and governance challenge.