Cybersecurity Is Under Fire And Credit Unions Are Fighting Back (Part 1)

Bad actors don’t rest. Credit unions are beefing up cybersecurity with smarter tools, stronger teams, and sharper defenses.

How a former Sam’s Club finance leader adapted his member-first mindset to a not-for-profit credit union.

The Michigan cooperative keeps everyday payments working and members happy by using a common friction point to build brand loyalty.

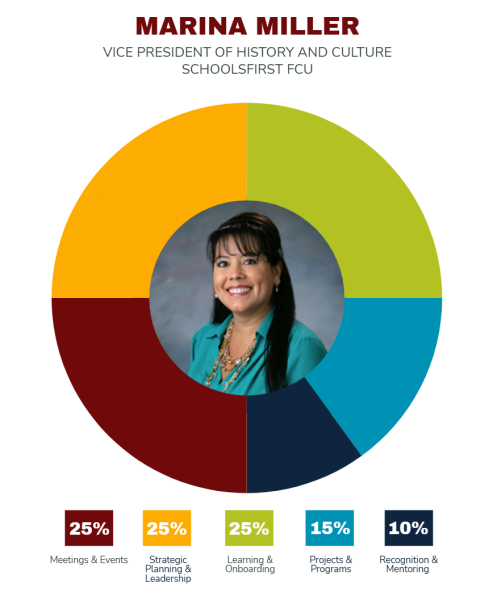

How a unique role instills SchoolsFirst FCU’s future leaders with an appreciation for its past.

Arriba Advisors co-founder Tom Russell explores how credit unions can bridge the gap between a growth mindset and their technical reality.

RKL offers insight, expertise, and experience to help fight off growing threats.

Members are anxious about their financial futures, even as credit unions remain financially strong. Institutions that respond to this moment can make 2026 a turning point.

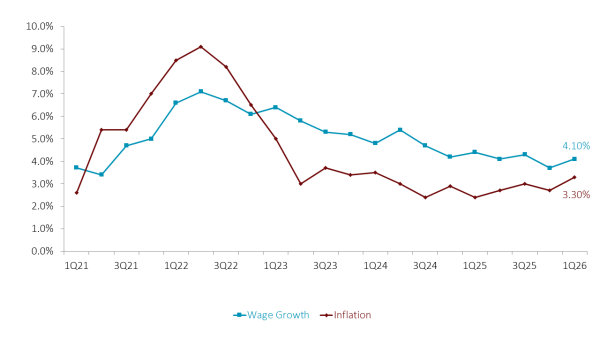

Global events are flowing directly into household budgets, reshaping how credit union members save, borrow, and cope. Such trends don’t always show up in headline data.

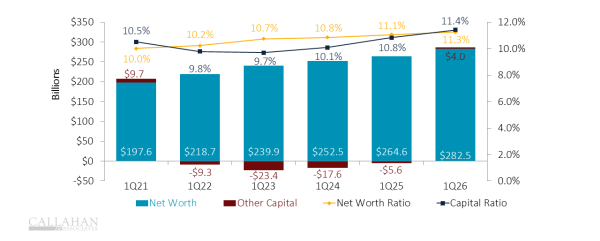

Credit unions are benefiting from a rare margin advantage as loans reprice slower than deposits. The question now is how institutions will use that strength to better serve members.

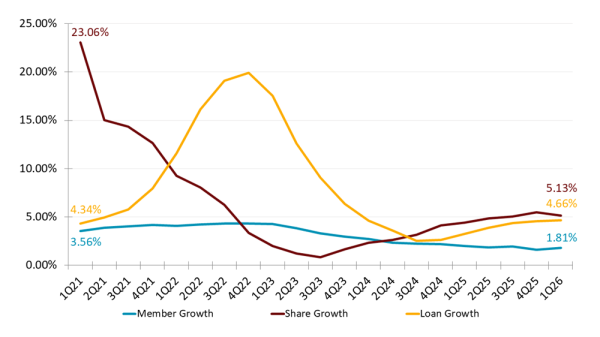

Membership growth is slowing, but financial activity is not. What does the modern financial relationship look like?

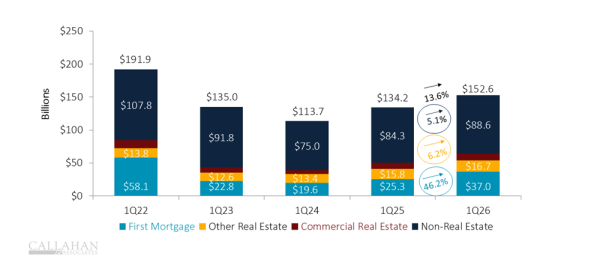

Inflation, war, and uncertain futures have reshaped members’ needs in 2026. What does credit union performance data from the first quarter of 2026 say about household budgets, inflation pressures, and more?