This is part of the Callahan Financial Performance Series. Presented by the analysts at Callahan & Associates, the series helps leaders interpret data to drive smarter decisions and uncover new approaches to measure performance. Callahan clients can access the full version of this article right now on the client portal. Read it today.

Credit union balance sheets continue to tell a largely positive story, but member finances are under growing pressure. Stable employment has kept the worst outcomes at bay, yet higher prices for housing, transportation, and everyday necessities are steadily eroding purchasing power.

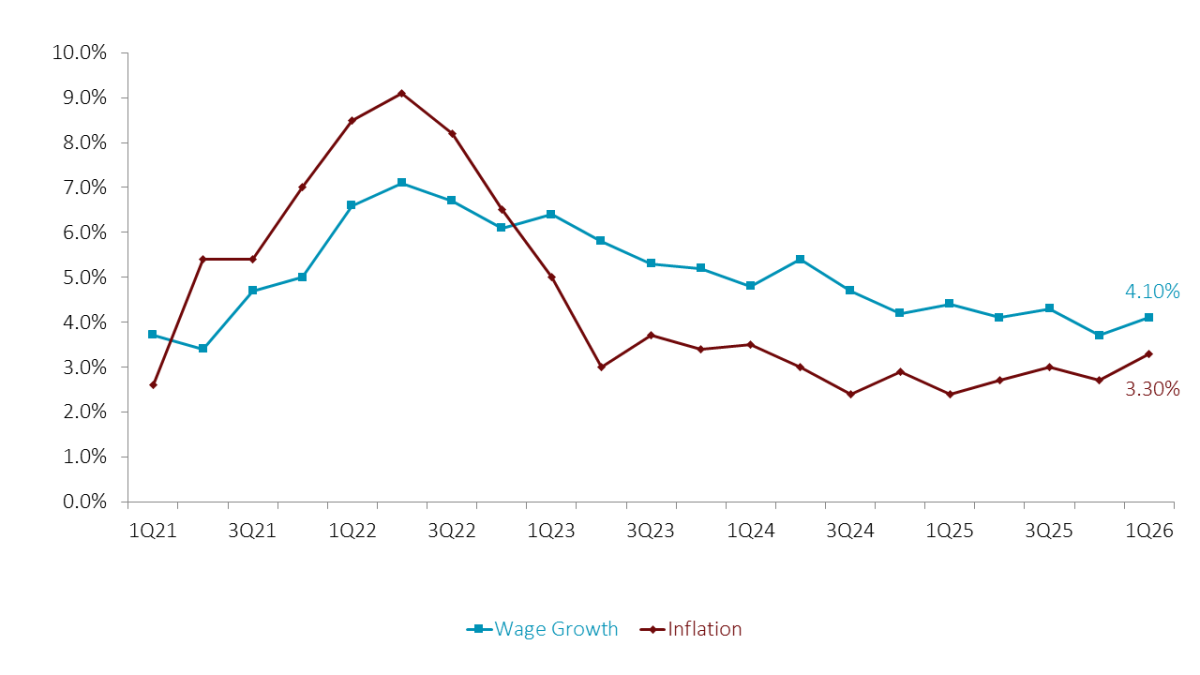

On paper, wage growth looks like a bright spot. In practice, inflation continues to absorb much of those gains, limiting real income growth and leaving many households with far less financial flexibility than headlines suggest.

WAGE GROWTH VS. INFLATION

FOR U.S. WORKERS | DATA AS OF 03.31.26

SOURCE: FEDERAL RESERVE BANK OF ATLANTA | BUREAU OF LABOR STATISTICS

- The divergence between wage growth and inflation highlights one of the most consequential macroeconomic trends for credit unions: real income pressure. Although nominal wages have risen, inflation absorbed much of those gains from 2022 to 2023, reducing purchasing power. According to the Bureau of Labor Statistics, inflation-adjusted wages and salaries for private industry workers have increased just 0.1% in the past 12 months. Despite a stable unemployment rate, the disparity between wages and inflation can negate many benefits of job security.

- With inflation cutting into wages, members turned to savings and credit to cover everyday expenses. Even as inflation has moderated, the cumulative erosion of real income has left household wallets thinner than headline wage figures imply. Credit card balances in the first quarter increased 2.6% annually, suggesting members are turning to credit for a financial cushion.

- From an asset quality perspective, compressed real wages heighten member vulnerability. Although credit card delinquency remained nearly unchanged at 2.03% from one year ago, its makeup is changing. The share of late-stage delinquency — defined as more than 60 days past due — has increased to 64.8% of total delinquent credit card dollars. That’s the highest reported by credit unions in more than 20 years. This signals a migration toward deeper delinquency, where financially strained members are less able to catch up once they miss payments.

Wage dynamics are only one piece of the picture. Housing affordability, energy costs, consumer confidence, and savings behavior are also shaping how members experience today’s economy and how those pressures show up on credit union balance sheets. Read more about that on the client portal.

When members know you care, they stay. The late-stage delinquency data in this article suggests households are running out of room. Gallup research shows emotionally engaged members are far more likely to trust their credit union as a financial partner when stress peaks. Callahan and Gallup equip credit unions to build that trust intentionally so members turn to you first when it matters most. Read more today.