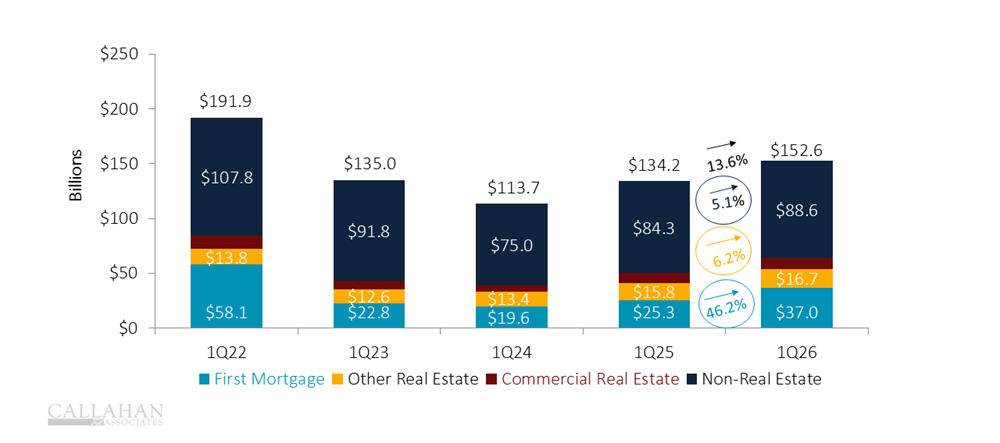

Mortgage lending rebounded in the first quarter of 2026, although that momentum remains fragile with rising mortgage rates and inflation already clouding the outlook. According to data from Callahan & Associates, first mortgages were up 46% for credit unions as modest gains in affordability drew borrowers back into the market.

LOAN ORIGINATIONS

FOR U.S. CREDIT UNIONS

SOURCE: CALLAHAN & ASSOCIATES

- A sharp increase in first mortgage volume underpinned a jump in total real estate originations in the first quarter of 2026. That segment reached its highest level since 2022.

- Declines in mortgage rates, although modest, spurred demand, with borrowers re-entering the market after a prolonged pause during peak rate conditions. Increases in mortgage rates could jeopardize this trend.

- The market is moving away from a purchase-only dynamic. Early signs of refinance activity are reappearing alongside purchase originations, driven by borrowers with higher-rate loans taken out in the past two-and-a-half years.

- Borrowers are acting opportunistically — re-engaging quickly when rates improve, even slightly — suggesting this is a short-term lending opportunity rather than a sustained refinance wave.

- Although origination volumes are improving, the trend represents selective re-entry into the market, not a broad normalization. Credit unions would be well-served to target their lending strategies.

Don’t stop here. Callahan clients can dive deeper into how shifting borrower behavior, product mix, and early risk signals are reshaping mortgage lending. The full analysis is available now on the Callahan client portal. Read it today.