Fintechs are claiming an ever-growing share of the financial services market. Digital assets in particular have expanded rapidly in recent years, and new research from McKinsey suggests this growth is poised to accelerate even further.

ESTIMATE TOTAL MARKET IMPACT OF DIGITAL ASSETS (TRILLIONS)

FOR THE GLOBAL ECONOMY | DATA AS OF APRIL 2026

SOURCE: MCKINSEY & COMPANY

How digital assets will ultimately reshape the credit union landscape remains a question. From lending to deposits, these emerging tools have the potential to fundamentally transform financial services — and credit unions will need to adapt to stay competitive.

Strategic Insights

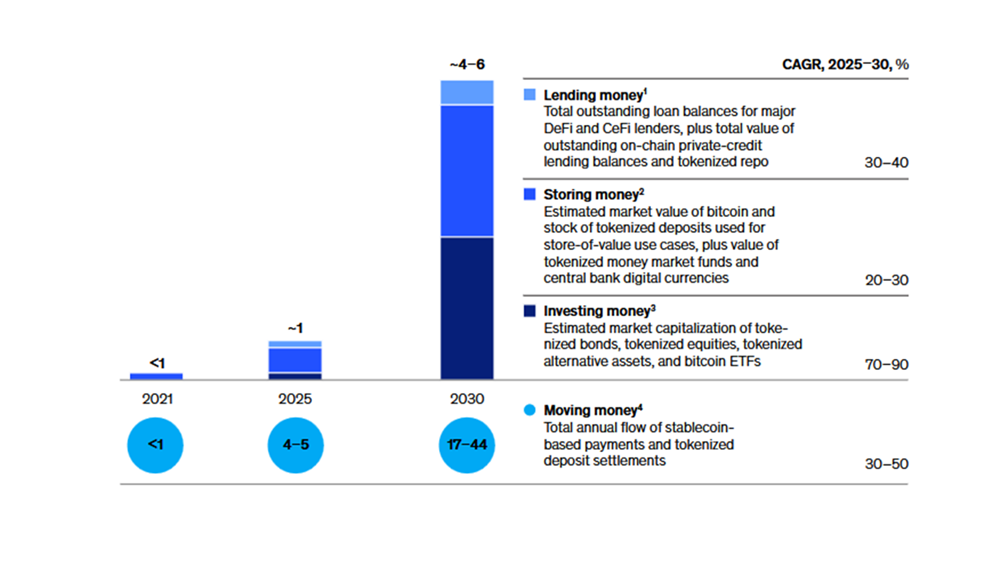

- According to McKinsey, digital assets’ role in lending could expand at a compound annual growth rate of 30% to 40% through 2030. The estimate includes total outstanding loan balances held by major decentralized and centralized finance lenders as well as blockchain-based private-credit lending. Centralized finance providers may accept digital assets as collateral but still operate through traditional compliance processes, including Know Your Customer requirements and centralized custodians.

- Meanwhile, McKinsey estimates the total flow of stablecoin-based payments and tokenized deposit settlements will reach at least $17 trillion by 2030. This money movement has the potential to bypass debit cards, removing a key source of non-interest income from credit unions.

- A strong understanding of the digital asset landscape can help credit unions. Familiarity with the legal, regulatory, and technical realities of these technologies provides important context for long-term strategy.

- When Cloud Financial Credit Union ($439.7M, Sartell, MN) realized a good chunk of its membership had cryptocurrency, it determined it had to invest in this emerging financial space.