The Right Tools To Make Tough Decisions

To create a culture of empowerment, Infinity FCU gives employees a vision to work toward, a decision-making model that managers stand behind, and ongoing training opportunities.

In order to adopt a more proactive strategy, the Iowa cooperative is using a dedicated product development team to promote visibility and follow-through from idea to launch.

This year’s finalists are reimagining how credit unions can use AI to combine cutting-edge technology with old-school member service.

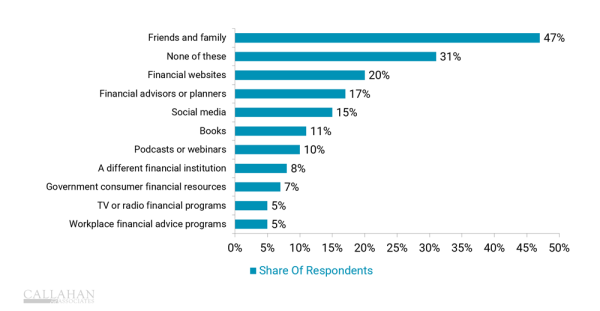

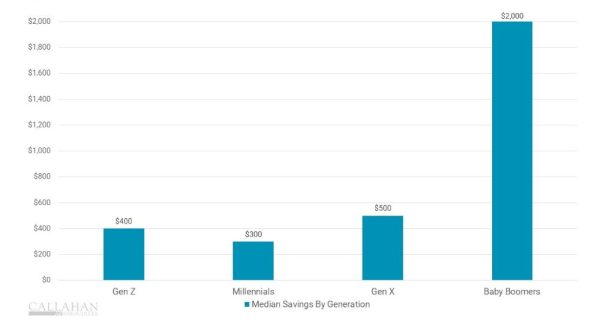

Financial advice comes in many forms. How can credits union make sure they are the No. 1 choice for their members?

This year’s finalists are uncovering new ways to harness the power of technology to improve and expand lending across the industry.

A program to help staffers improve their savings skills generated more than $200,000 in deposits and helped change participants’ financial habits.

As Super Bowl LX nears, the Callahan Bowl prediction model says the Seahawks will see green en route to the Lombardi Trophy.

Lending is evolving, and credit unions are adapting. This week, CreditUnions.com examines how shifting economic conditions are reshaping lending strategies.

Affordability pressures, extended loan terms, and shifting vehicle values are forcing institutions to look beyond familiar structures and reconsider how to balance risk and return.

Credit unions are uniquely well-positioned to guide members through uncertainty and fill essential funding gaps.

A closer look at the trade-offs of mandated lower credit card rates reveals a delicate balance between portfolio health and member access.

Are Your People Prepared?