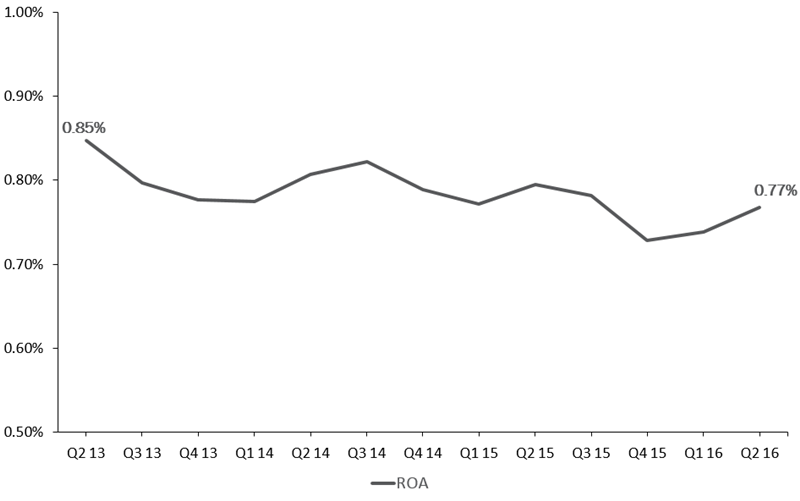

Credit unions are on track to post a solid 0.77% in Return on Assets (ROA) for second quarter 2016, according to Callahan Associates. That figure is a three-basis-point improvement over first quarter 2016; however, the metric is down slightly from last year’s second quarter ROA of 0.79%.

ROA, which Callahan calculates by dividing annualized net income by average assets, measures a credit union’s profitability. In general, a high ROA reflects a credit union’s success at using its assets to generate income.

Credit unions should, however, view ROA in light of their individual strategies. For example, if a credit union passes on opportunities to earn higher profits such as by charging lower fees or offering better loan rates then its member-centric strategy might result in a low ROA relative to its industry peers.

RETURN ON ASSETS

FOR U.S. CREDIT UNIONS* | DATA AS OF 06.30.16

Callahan Associates | www.creditunions.com

* For 5,976 credit unions.

Source: Peer-to-Peer Analytics by Callahan Associates

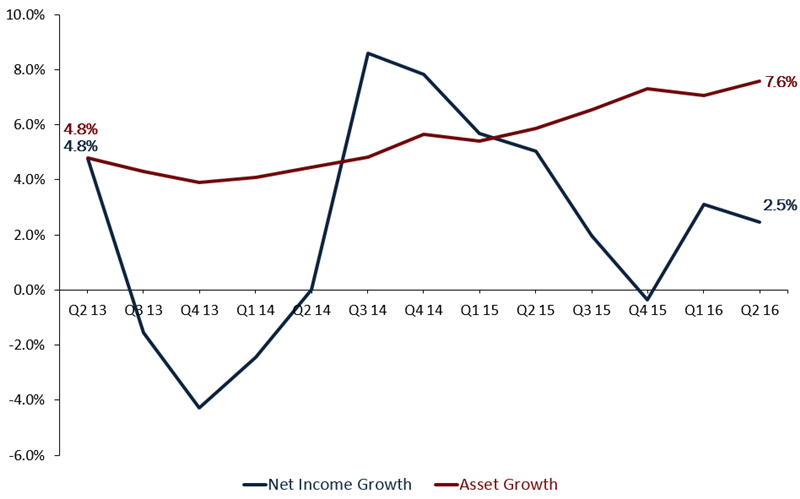

Strong positive net income and asset growth for the industry makes its difficult to understand why ROA growth is slowing. However, separating the two components of ROA paints a clearer picture.

Assets are growing at a much higher and much more steady rate than net income. Because assets are the denominator in the ROA equation, the overall ROA ratio is growing at a slower pace.

YEAR-OVER-YEAR NET INCOME AND ASSET GROWTH

FOR U.S. CREDIT UNIONS* | DATA AS OF 06.30.16

Callahan Associates | www.creditunions.com

* For 5,976 credit unions.

Source: Peer-to-Peer Analytics by Callahan Associates

The industry asset growth is stellar, but credit unions would benefit from focusing on increasing net income. On way to boost net income and consequentially ROA is by scaling back interest and non-interest expense or ramping up interest and non-interest income.

In Search Of Non-Interest Income

In July 2016, Callahan Associates surveyed 170 credit union executives from 40 states to gain insight into their current and emerging sources of non-interest income.

Click here for the:

Asset growth is a metric that measures success, but credit unions need to leverage their expanded asset bases to grow net income.

ROA is not the most important metric to credit unions financial cooperatives are driven more by member return than profits. Nevertheless, it is important to monitor ROA. By growing net income and assets at a similar rate, credit unions can boost this standard measure of productivity and profitability.