The Federal Reserve has said it will keep the benchmark federal funds rate near 0% for the foreseeable future. Consumers have taken advantage of these low rates by financing and refinancing purchases throughout the year, with most loan generation coming in the form of first mortgages. The Mortgage Bankers Association reported a record year of $3.7 trillion in mortgage originations and a quarterly record of $1.1 trillion in the fourth quarter alone. Americans resumed spending activity during the holidays, and the nation’s aggregate revolving debt increased 3.3% from the third quarter after falling for much of 2020.

Key Points

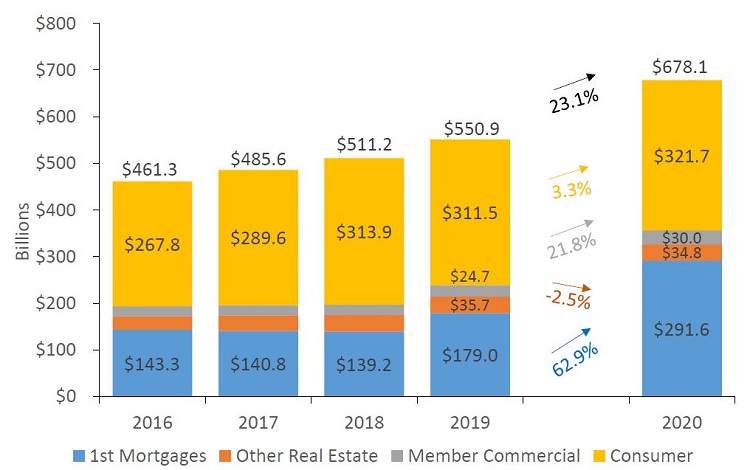

- Credit union loan originations reached a record $678.1 billion in 2020, an annual increase of 23.1%. First mortgages accounted for 43.0% of originations as home loan production grew 62.9%.

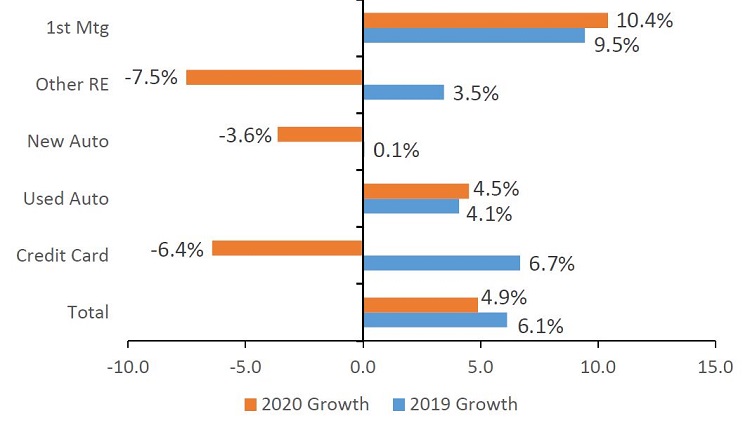

- With non-real estate lending down, outstanding loan growth slowed 1.2 percentage points annually to 4.9% in 2020. Many members opted to use government relief packages to pay off debt.

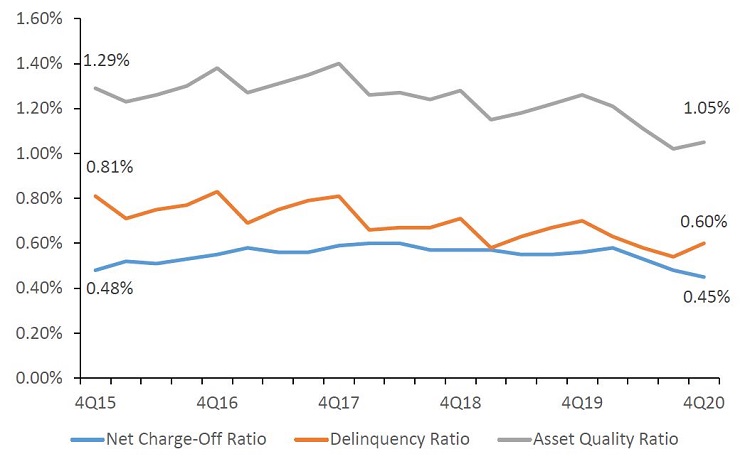

- Delinquency improved 10 basis points annually 0.60%. to Credit unions helped troubled members with widespread loan forbearance programs. Still, delinquency increased 6 basis points from third quarter lows, perhaps a sign that postponed loan payments are coming due.

Click the tabs below to view graphs.

YEAR-TO-DATE LOAN ORIGINATIONS

YEAR-TO-DATE LOAN ORIGINATIONS

FOR U.S. CREDIT UNIONS | DATA AS OF 12.30.20

Callahan & Associates | CreditUnions.com

Low rates and record demand for refinances drove the largest loan generation year on record for the industry.

OUTSTANDING LOAN BALANCE GROWTH BY TYPE

OUTSTANDING LOAN BALANCE GROWTH BY TYPE

FOR U.S. CREDIT UNIONS | DATA AS OF 12.30.20

Callahan & Associates | CreditUnions.com

Quarantines and consumer loan payoffs drove down balances in many categories. However, first mortgage balance growth was enough to maintain a healthy expansion in total loan balance.

ASSET QUALITY

ASSET QUALITY

FOR U.S. CREDIT UNIONS | DATA AS OF 12.30.20

Callahan & Associates | CreditUnions.com

The asset quality ratio the delinquency ratio plus the net charge-off ratio declined during the first six months of the pandemic; however, an increase in delinquency at the end of the year has drawn more attention to this metric.

The Bottom Line

Two competing factors influenced credit union lending in 2020: historically low interest rates and nationwide lockdowns. Low rates sparked a wave of mortgage refinances, which brought new members into the credit union movement. However, shuttered manufacturing plants and service industries suppressed auto and credit card growth for much of the year. Consumer lending rebounded slightly in the fourth quarter thanks to economic reopening and seasonal spending, but credit unions will need to monitor the decline in asset quality that came with it. All told, a record mortgage year facilitated healthy loan balance growth in the industry and many members are well situated to resume pre-COVID spending habits.

This article appeared originally in Credit Union Strategy & Performance. Read More Today.