Looking back just four years, Langley Federal Credit Union was an unrecognizable institution to the one that exists today. Loan and membership growth were negative, and the institution’s loan-to-share ratio was nearly 30% lower than the peer average of credit unions with more than $1 billion in assets. Today, things are different. Both loan and membership growth far outpace peer average, and the credit union’s loan-to-share ratio sits comfortably in the low 90% range.

CU QUICK FACTS

Langley Federal Credit Union

Data as of 12.31.15

- HQ: NEWPORT NEWS, VA

- ASSETS: $2.1B

- MEMBERS: 232,438

- BRANCHES: 18

- 12-MO SHARE GROWTH: 10.70%

- 12-MO LOAN GROWTH: 19.63%

- ROA: 0.76%

But the story of $2.1 billion Langley FCU’s organizational redirection doesn’t start at its headquarters in Newport News, VA. It starts in Marlborough, MA, circa late 2008. That’s when the CEO of Digital Federal Credit Union, Carlo Cestra, retired and the credit union looked to CFO Jim Regan and COO Tom Ryan as possible successors.

We always knew only one of us could get the CEO job, Ryan says. The person who didn’t likely would move on to a CEO position at another credit union.

Ultimately, the position went to Regan, and Ryan started a yearslong selective search to find a new credit union that would suit him like institution where he had worked for 26 years.

I was selective because I wanted to find the right organization, Ryan says. One at which I could make a difference.

Fast forward to early 2012, when the retirement of Langley FCU’s longtime CEO Jean Yokum opened up the top spot at a credit union that had just south of $1.7 billion in assets and a net worth ratio of 12.5%.

It was a credit union that was well-established and had a great reputation, Ryan says. It seemed like a great opportunity.

Ryan took the helm at Langley FCU on July 18, 2012. And although there was a lot Ryan valued at his new institution it was one of the 100 largest credit unions in the country, after all there was work to be done. Namely, its balance sheet, leadership structure, and institutional culture were ripe for change.

The First Steps In A New Direction

The First Steps In A New Direction

According to second quarter 2012 data from Callahan Associates, Langley FCU’s loan-to-share ratio of 41.22% lagged behind its asset-based peer average of 70.06%. Additionally, member growth had dipped to -6.83% and its ROA was also trending negative. Finally, the institution held more than $1 billion in total investments, which surpassed its asset-based peer average by more than $200 million.

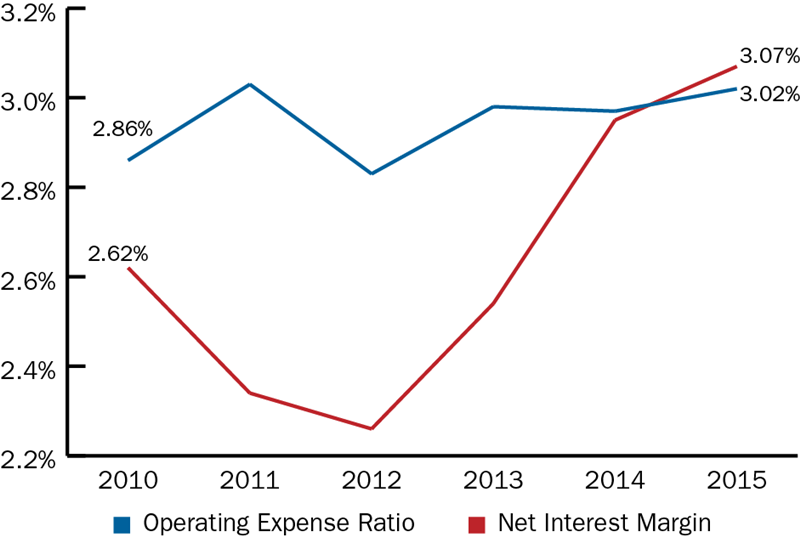

Unsurprisingly, Langley’s net interest margin had fallen to 2.19%, well below its asset-based peer average of 2.81%.

Langley was built for savers, says Langley FCU’s CFO and senior vice president Ingo Huemer.

Neither the saving nor the investing was a problem in the higher interest rate environment of the late aughts and early 2010s, but those rates didn’t last.

When interest rates started dropping, we had to make some changes, says Huemer, who was Langley FCU’s vice president of risk in 2012.

Curtis Baker, the credit union’s senior vice president of lending, agrees. Although Baker didn’t join the credit union until mid-2013, he had studied Langley FCU’s balance sheet when interviewing with the institution, and he saw opportunity for change.

At the time the yield on investments was about 75 basis points and it was a large portfolio, he remembers. It was pretty obvious in looking from afar what needed to be done.

Langley needed to make more loans.

![ThinkstockPhotos-470277327_[Converted]](https://creditunions.com/wp-content/uploads/2022/08/ThinkstockPhotos-470277327_Converted.png) Homework For Adults

Homework For Adults

Ryan spent his first months at Langley FCU learning about its people and its processes. DCU was a serious lender, and as its offensive coordinator, he had years of experience managing its branch network, call center, and lending areas. He knew what it took to kick-start a credit union’s lending engine, but first he needed to see what he was working with.

You learn a lot in the first few months on the job, Ryan says. You can’t learn everything from the balance sheet, you have to see what’s going on in the organization.

Ryan quickly identified an inconvenient truth: ALM modeling predicted Langley FCU’s earnings would be negative in six months. That’s not a deathblow to an institution with net worth north of 12.5%, but it’s not a sustainable path, either.

Flush with deposits, Langley had the liquidity to fund loan growth. But shifting the balance sheet required a philosophical change that prompted Langley FCU to also sell significant chunks of its investment portfolio to boost liquidity for loans.

We weren’t serving our members by investing their deposit money, Ryan says. I felt it was our role to invest in our members in the form of loans.

![ThinkstockPhotos-470277339_[Converted]](https://creditunions.com/wp-content/uploads/2022/08/ThinkstockPhotos-470277339_Converted.png) Building A Lending Machine

Building A Lending Machine

To aid in its transformation from a savings to a lending institution, Langley FCU lowered its deposit rates. According to CFO Ingo Huemer, the credit union kept its rates competitive but no longer positioned itself as a market leader.

We were not going to pay a premium for deposits, he says.

On the lending side, Huemer says the credit union evaluated what it was bringing in, which was middle-tier paper.

Pre-2012, if you were an ‘A’ borrower you wouldn’t come to Langley for a loan because the rate was too high, he says. But if you were a ‘C’ borrower, you could come to the credit union because we weren’t completely out of the market.

We weren’t serving our members needs by investing their deposit money. I felt it was our role to invest in our members in the form of loans.

Langley FCU set goals to become less concentrated in middle-tier paper and established a credit mix to return the yield it desired within its new risk parameters.

Bringing in higher-grade paper allowed the credit union to lower its concentration within middle-tier paper, therefore balancing the overall risk of its loan portfolio. Today, Langley FCU aims for the following credit mix within its new loans as shown in the table below.

LANGLEY FCU’S PREFERRED CREDIT MIX

| Credit Rating | Preferred Percentage Of Total Portfolio Credit Score |

Credit Tier |

|---|---|---|

| A+ | 55% | 740 |

| A | 15% | 710-739 |

| B | 15% | 670-709 |

| C | 10% | 640-669 |

| D-E | 5% | 600-639; 600 |

Despite the fact loan growth at Langley FCU has indeed taken off, overall loan delinquencies have dropped. Since reaching a high of 2.88% in fourth quarter 2011, the credit union’s overall loan delinquency has steadily declined and was 0.95% as of fourth quarter 2015, although that is still 20 basis points higher than its peer average.

<tdvalign=”top”>

12-MONTH LOAN GROWTH

For all U.S. credit unions | Data as of 12.31.15

Callahan Associates | www.creditunions.com

<tdvalign=”top”>

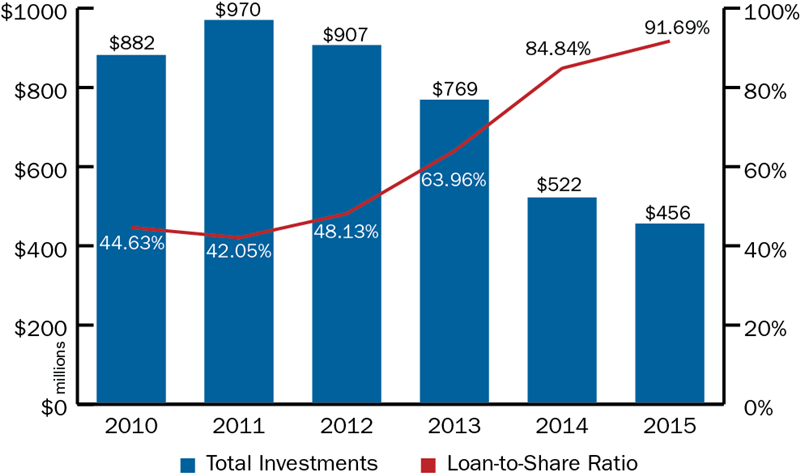

LOAN-TO-SHARE-RATIO AND TOTAL INVESTMENTS

For all U.S. credit unions | Data as of 12.31.15

Callahan Associates | www.creditunions.com

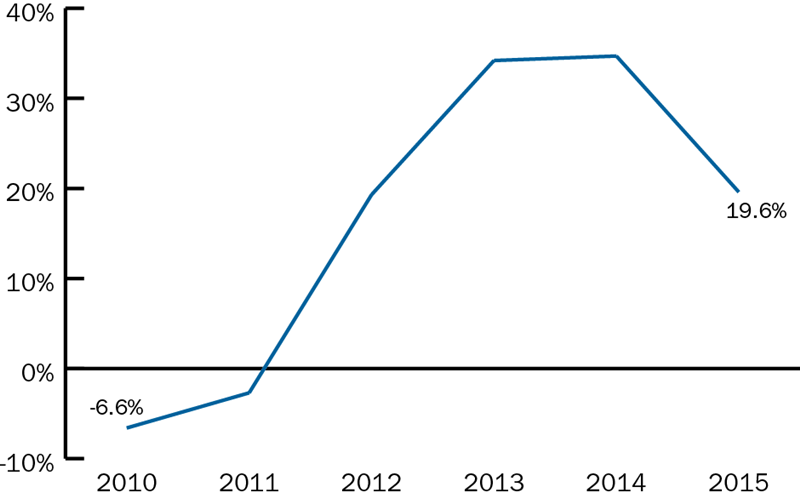

| 5-YEAR LOAN GROWTH For all U.S. credit unions | Data as of 12.31.15 Callahan Associates | www.creditunions.com  |

|

| Loan growth at Langley FCU slowed in 2015 but still outpaced national loan growth by 9.1 percentage points. | Loan growth slowed in 2015 following two years of above average growth. |

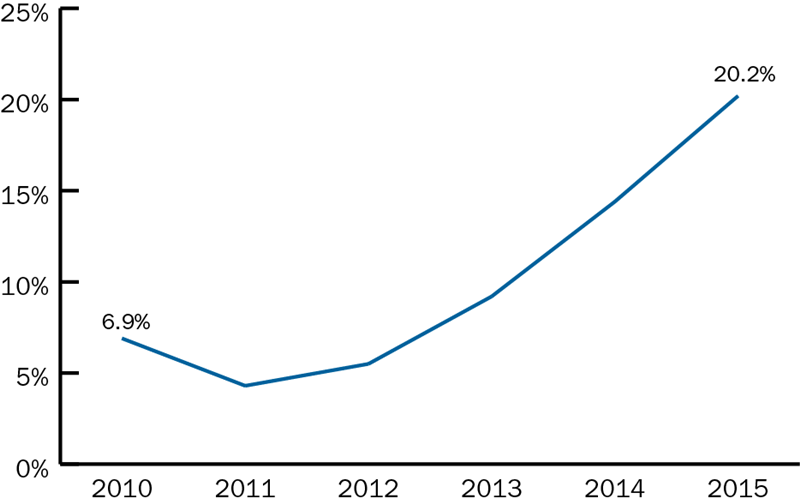

| 5-YEAR COMPOUNDED ANNUAL LOAN GROWTH For all U.S. credit unions | Data as of 12.31.15 Callahan Associates | www.creditunions.com  > |

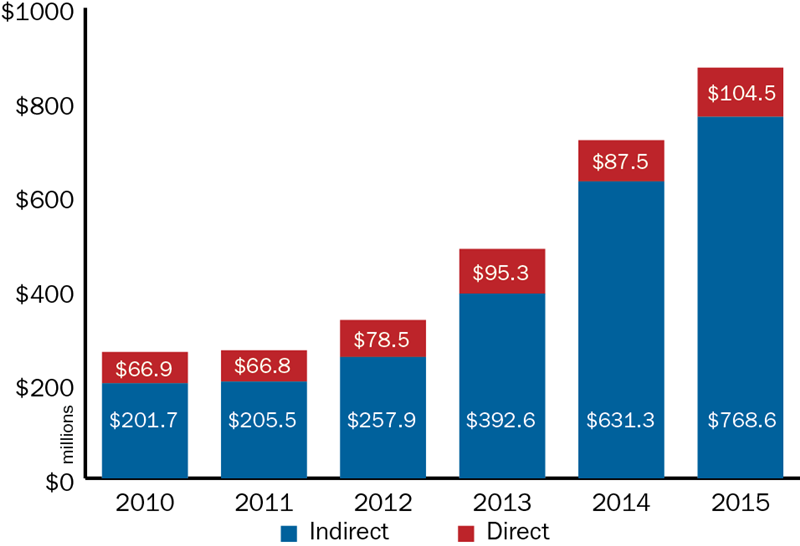

DIRECT AND INDIRECT AUTO LOAN BALANCES For all U.S. credit unions | Data as of 12.31.15 Callahan Associates | www.creditunions.com  |

| Year-end data showed the five-year compounded annual loan growth rate soared 20.2% at the Virginia credit union. | Total direct and indirect lending expanded 21.5% annually. |

| NET INTEREST MARGIN AND OPERATING EXPENSE RATIO For all U.S. credit unions | Data as of 12.31.15 Callahan Associates | www.creditunions.com  |

|

| Langley FCU continued to be loaned out at year-end while total investments fell for the fourth consecutive quarter. | The net interest margin increased at Langley FCU mainly as a result of rising interest income. |

| Source: Peer-to-Peer Analytics by Callahan Associates |

Interest Rate Risk, Friendly Loan Growth

Interest Rate Risk, Friendly Loan Growth

As the Langley FCU team looked to ramp up its lending, two factors weighed heavy on Ryan.

First, membership growth was negative.

We needed to create a value proposition for members to do business with us, the CEO says.

Second, the interest rate environment was uncertain.

We were worried about low interest rates and their eventual move upward, says Curtis Baker, the credit union’s senior vice president of lending. So what kind of portfolio responds well to rising interest rates?

The credit union turned its focus to variable-rate, short-term products such as home equity lines of credit, credit cards, and auto loans. For example, Langley’s average auto loan lasts approximately 2.5 years, according to Baker, so as rates increase, the portfolio will reprice quickly.

To better crystalize its value proposition with members, Langley implemented a new credit card strategy. By early 2013, it had dropped its legacy fixed-rate product and introduced three new cards a rewards card, a cash-back card, and a basic card with Langley’s lowest rates.

We needed to make changes, Ryan says. Some of it was as simple as looking at pricing, making changes, and developing promotions. In other cases, we had to reinvent things.

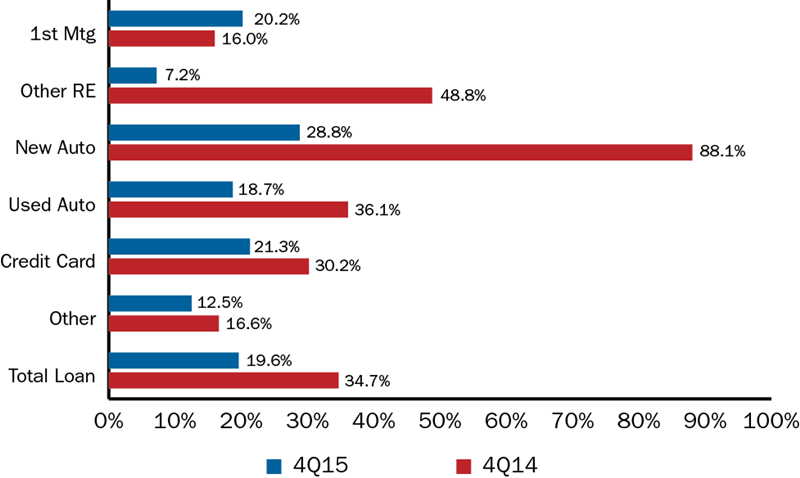

Since the fourth quarter of 2013, the credit union has yet to post three months of credit card growth lower than an annualized 10%.

When it comes to auto, Langley FCU has always held more indirect loans as a percentage of total auto loans than its peers. And through Baker’s leadership, Langley FCU hit indirect lending harder.

The credit union implemented what Baker describes as a production environment for its loan officers/underwriters, of which the credit union has 13 seven in consumer and six in mortgage lending.

It adjusted pricing its average auto loan rate is now 4.3% to create a portfolio with its desired credit mix and now makes automatic decisions based on those credit parameters. Applications with a credit score higher than 550 that don’t make it through the credit union’s auto approval process go to an employee to review; those with a credit score of less than 550 don’t.

As of fourth quarter 2015, Langley FCU held 88.04% of its total auto loan portfolio in indirect loans, which exceeds the average at other billion-dollar credit unions by nearly 30 percentage points.

The credit union also now sets production expectations both in terms of application turnover and hours of operation.

We were used to a slow volume and pace, Baker says. It was difficult for some of our employees to manage our new expectations for speed and volume. But sometimes you have to overhaul things. Sometimes you can’t change without it.

Of late, Langley FCU has also boosted its direct auto lending performance, representing, Baker says, proof that Langley’s investments in retail and other aspects of the production process have worked well. According to Baker, the cooperative produced 27% more in direct auto loans in 2015 than 2014, a performance primarily built upon the credit union’s refinance program.

Overall, loan growth at Langley FCU is up across the board. As of fourth quarter 2015, year-over-year auto and credit card growth rates are 21.47% and 21.35%, respectively. That bests its asset-based peer averages of 16.13% and 8.04%. The credit union’s total loan growth of 19.63% outpaces the 12.49% of its peers as well and represents 13 consecutive quarters of loan growth greater than an annualized 19%.

Save Time. Improve Performance.

Save Time. Improve Performance.

NCUA and FDIC data is right at your fingertips. Build displays, filter data, track performance, and more with Callahan’s Peer-to-Peer analytics.

A Balanced Growth Mode

A Balanced Growth Mode

When Ryan took over Langley FCU, the credit union’s loan-to-share ratio was in the low 40s. By third quarter 2014, it had surpassed that of its asset-based peers. As of fourth quarter 2015, it was nearly 92%, and that’s a number the credit union is comfortable with, Huemer says.

To fund these loans, the credit union had primarily relied on liquidating its investment portfolio rather than grow shares. To wit, share balances grew at levels below peer average each quarter from Ryan’s arrival to the third quarter of 2015. When liquidity tightened and some of the credit unions long-term investments were underwater, the institution utilized a borrowing strategy ($150 million) rather than selling the investments at a loss. Today, it has again returned to attracting new deposits and growing shares.

Long-term, we need to grow both sides of the balance sheet, Huemer says. We’re now in a more balanced growth mode.

As of fourth quarter 2015, the credit union holds more than $1.7 billion in shares, representing a year-over-year growth rate of 10.7%, greater than the 8.63% growth rate at the average billion-dollar credit union.

Long-term, Ryan says Langley FCU wants to grow to $3 billion in loans and $4 billion in assets by 2020. Right now, it’s approximately halfway there.

The plan to achieve these ambitious goals is to continue with its lending and deposit strategies while considering other growth opportunities.

The credit union’s senior vice president of branch services, Deb Vollmer, mentions possible new branches in Virginia Beach and Norfolk, further southeast from its headquarters in Newport News. The cooperative also has started due diligence toward a potential expansion to another part of the Commonwealth altogether.

And if there’s a merger opportunity down the road, the credit union would consider it.

Langley FCU sees years of growth in its future; certainly, it has no plans to slow down.

Our loan origination has become so efficient, we’d like to keep that machine running, Huemer says.

It was difficult for some of our employees to manage our new expectations for speed and volume. But sometimes you have to overhaul things. Sometimes you can’t change without it.

Staffing For A New Culture

Staffing For A New Culture

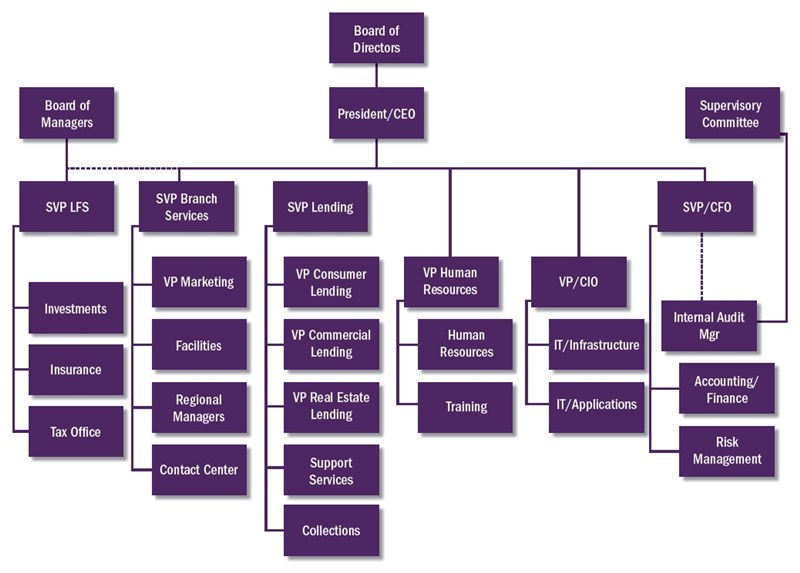

To facilitate the credit union’s culture change, Ryan assessed Langley FCU’s management and flattened the chain of command. Instead of vice presidents, senior vice presidents, and executive vice presidents reporting up the chain to the CEO, Ryan met weekly with all vice presidents and higher to learn more about the organization and identify individual strengths.

Ryan promoted some employees and refined or changed the responsibilities of others. He eliminated the EVP tier, leaving a team of senior vice presidents reporting directly to Ryan.

Don’t reinvent the wheel.

Don’t reinvent the wheel.

Get rolling on important initiatives using documents, policies, and templates borrowed from fellow credit unions. Pull them off the shelf and tailor them to the credit union’s needs. Visit Callahan’s Executive Resource Center on the client portal today.

I wanted to give people a chance to succeed, Ryan says. I knew my success was pinned to my ability to have a great management team working with me. Some new leaders might come in and clean house, but that wasn’t my style.

When Langley’s assistant vice president of branch services retired in 2012, the credit union opted to replace her with three regional managers who specialize in a different aspect of branch management sales, business development, and operations and oversee branches according to their bandwidth. For example, the sales and service regional manager oversees four branches; the other two each oversee seven.

This new design has helped the branches become a place for members to start and deepen relationships rather than simply conduct transactions. For example, branch managers are out of the office at least one day a week developing business contacts, signing up new select employee groups, or increasing the credit union’s presence in its community. Additionally, branch staff look at member relationships holistically to ensure Langley FCU is their primary financial institution, as one of the credit union’s strategic objectives for 2016 is to increase the number of members with three or more relationships.

Langley Federal Credit Union Organizational Chart

The branch’s purpose is to form and expand member relationships, Vollmer says. Everybody in the branch is engaged with the same focus.

Later in 2012, Langley also started reorienting its branches away from transactions and toward sales and service.

All credit union staff members completed CUNA’s Creating Member Loyalty program to shore up their service training and front-line, and sales staff completed additional sales and referral training. The team finished its program training in the fall of 2015; since then, Langley FCU has re-evaluated its requirements for tellers and other branch personnel with an eye toward attracting more front-line employees with strong retail backgrounds and an ability to engage in conversation.

We had branch staff who could count money, who were accurate, Vollmer says. But we can teach them how to do that. We can’t teach personality.

Building Success. Sharing Rewards.

Building Success. Sharing Rewards.

With Gratitude

Thank you to the fine folks at Langley Federal Credit Union who took the time to tell their story to Callahan Associates. Your helpfulness, friendliness, and thoroughness allowed us to present the kind of detailed, informative story that other credit unions can use to build their own successful strategies.

Where Were They Then?

Langley FCU’s senior leaders talk about the paths that brought them together.

|

|

Curtis Baker, SVP, Lending

|

It’s funny, I was here on vacation and I saw the job opening and I said why not?’ I put my hat in the ring and three months later I moved down here and started working.

|

|

Ingo Huemer, SVP/ CFO

|

I was with a larger regional public accounting firm and had been in that industry for about 20 years. I decided I was tired of tax season and needed a change, so I came to Langley about 10 years ago in an internal audit role.

|

|

Tom Ryan, CEO

|

The reality is, in any new job before you get inside and get to know the people in the organization you don’t really know. You have to understand all the things you can’t tell from a call report, a website, or outside research.

|

|

Deb Vollmer SVP, Branch Services

|

I was at a much smaller credit union for approximately 14 years before I decided to go into retail financial management as a comptroller at a local garden center. And, honestly, I missed credit unions the moment I left. So I applied to Langley and came here in 2003 as a branch manager because that’s the only position I could find that was open.

When Ryan arrived, he asked employees a simple question: How do you know if Langley is having a great year? The two most common answers, he says, were:

- I don’t know.

- ROA?

How can you be successful as an organization if not everyone understands what success is? he asks.

To develop internal understanding of success, promote common goals, and create an aligned institution, Ryan instituted a success-sharing program, an idea he brought from DCU.

Each year for the past three years, Ryan and his senior managers have worked with the board to identify a set of metrics to gauge organizational success. Typically, these metrics come in two flavors: strategic goals focused on member product usage, and growth goals.

For example, the institution’s 2016 goals are to increase deposits and loans under management by 10% each, increase active checking accounts by 9%, and increase members with three or more relationships by 12%.

These are the same goals I am assigned by the board, Ryan says. I know if I turn them into everybody’s goals, then I will have a better chance of hitting them.

If the credit union hits all its goals, it pays every employee 8% of their current annual salaries.

If the organization is successful, I want our employees to share in that success, Ryan says.

But it’s not an all-or-nothing proposition. The credit union offers employee bonuses based on the number of goals reached, so even if Langley fails to hit one or two, it still pays employees based on progress made. Each of the past three years the credit union has paid out 7-8% of current annual salary, or three to four extra weeks of pay per year.

At the branch level, however, Vollmer and the credit union set more specific goals which could involve credit cards or real estate lending, for example that ultimately relate back to the institution’s overall goals.

I need to give them a focused approach, says the SVP of branch services. Although it still aligns to our common goals measured in the Success Sharing program.

And as far as tracking these goals, any employee can view progress on the credit union’s intranet dashboard.

You could ask anybody in the organization and they would tell you what our success sharing goals are, Vollmer says. The organization is more aligned because of it.