The COVID-19 pandemic has stunted the growth of credit union auto lending, but the product remains a major part of the movement’ s loan portfolio.

Although some measures, such as market share, dipped year-over-year, loan quality as measured by delinquencies has held up well through the economic upheaval, according to Callahan Associates analysis of third quarter 2020 data from the NCUA, the most recent available.

In fact, delinquency in the third quarter hit its lowest mark since 2013. Some of this improvement in asset quality can be chalked up to payment deferrals during the pandemic, but the measure is still impressive. It is worth noting, however, that delinquency is only one view of member health and more information is not yet available related to the proportion of loans in deferment and forbearance.

Auto loans lead the lending portfolio in terms of market share and penetration, as well. More than one-fifth of all members held an auto loan at their credit union as of Sept. 30, 2020, and 17.9% of all U.S. auto loans belong to member-owned financial cooperatives.

Growth Is Slowing, But Still The Portfolio Grows

Compared with the third quarter of 2019, total auto lending grew 1.2%, or $4.5 billion, to $382.7 billion outstanding. This is the slowest third quarter rate since 2011, but growth has rebounded slightly from the 1.0% annual growth rate reported in June 2020, mostly due to the economy reopening in the third quarter.

With growth suppressed, auto loans comprised 32.8% of total credit union loan portfolios in the third quarter, the lowest share in that metric since the first quarter of 2015. Some of that can be attributed to large increases in mortgage balances which was up 12.9% as low interest rates encouraged members to refinance existing loans and purchase new homes.

Refinances accounted for 57.0% of credit union mortgages in the third quarter, according to estimates from the Mortgage Bankers Association. As interest rates remain at or near historic lows, mortgage growth will likely remain strong, which would further increase the share of the loan portfolio mortgages comprise.

Total Vehicle Sales Begin To Rally

Total vehicle sales plummeted during the first months of the pandemic as automakers and suppliers shut down and joblessness soared. Projected annual vehicle sales totaled 9.1 million units in April 2020 lower than any month following the Great Recession. However, this trend reversed as the economy adjusted to a new normal, and auto sales rallied as dealerships cautiously re-opened and offered online purchase programs. In September, projected annual vehicle sales reached 16.7 million units.

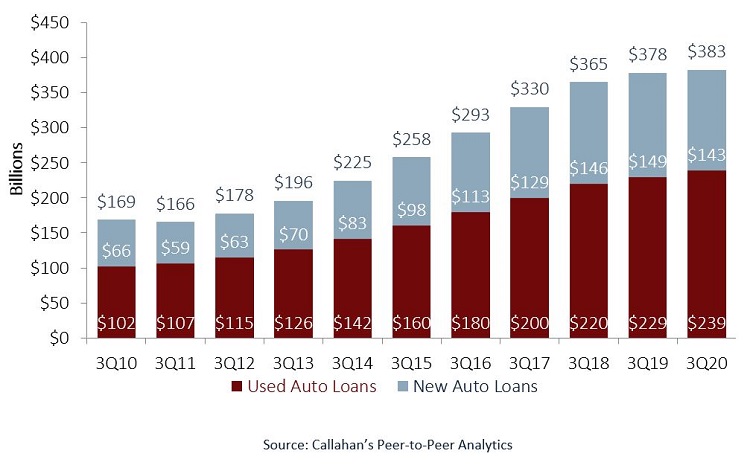

Historically, credit union auto loan portfolios skew in favor of used auto loans. Used auto balances expanded 4.4% to $239.5 billion 62.6% of auto loans whereas new auto loans contracted 3.7% to $143.2 billion over the past 12 months.

During the year, the total number of auto loans extended by credit unions increased 2.3%, or 592,000, to 26.3 million. This dynamic decreased the average credit union auto loan balance 1.1% year over year to $14,542 as of Sept. 30.

Trends In Auto Lending

TOTAL AUTO LOANS

FOR ALL U.S. CREDIT UNIONS | DATA AS OF 09.30.20

Total credit union auto lending in the third quarter of 2020 rose $4.5 billion, or 1.2%, year-over-year to $382.7 billion.

Source: Callahan Associates.

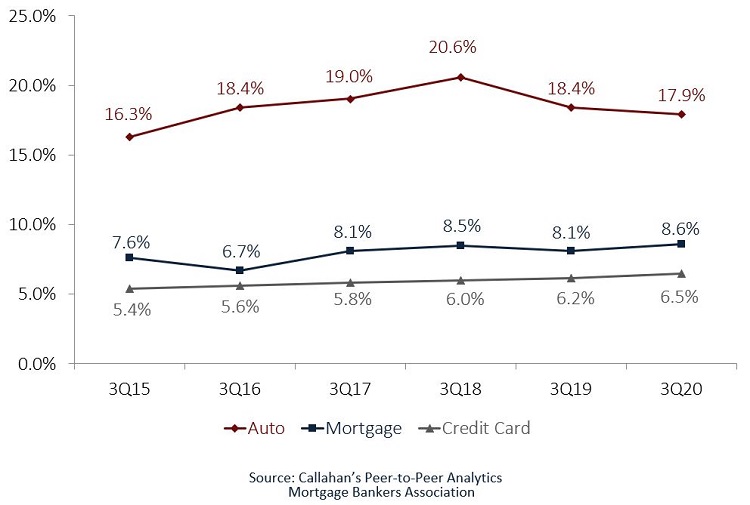

CREDIT UNION MARKET SHARE BY LOAN TYPE

FOR ALL U.S. CREDIT UNIONS | DATA AS OF 09.30.20

The credit union share of the auto lending market inched down year-over-year to 17.9%.

Source: Experian Automotive, Mortgage Bankers Association, Federal Reserve.

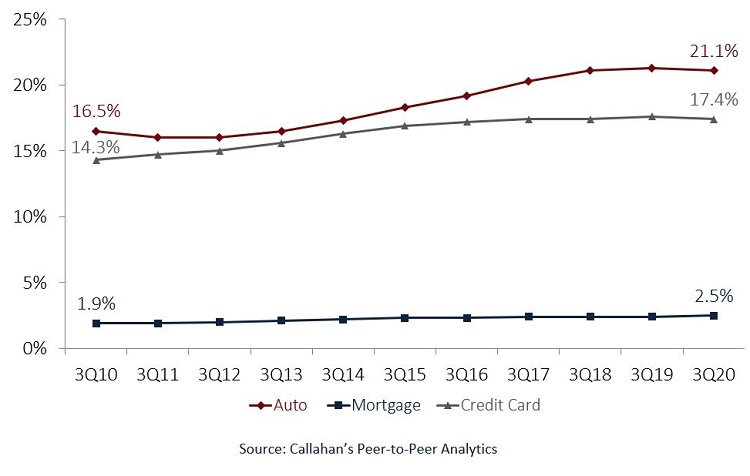

PENETRATION RATES BY LOAN TYPE

FOR ALL U.S. CREDIT UNIONS | DATA AS OF 09.30.20

The auto loan penetration rate among members dipped to 21.1% but remained the highest among loan types.

Source: Callahan Associates.

TOTAL INDIRECT BALANCES SHARE OF AUTO PORTFOLIO

FOR ALL U.S. CREDIT UNIONS | DATA AS OF 09.30.20

Indirect lending accounted for the majority of auto balances; however, growth in that channel has decelerated over the past year.

Source: Callahan Associates.

AUTO LOAN DELINQUENCY

FOR ALL U.S. CREDIT UNIONS | DATA AS OF 09.30.20

Auto delinquency continued a three-year decline in the third quarter, especially among used auto loans.

Source: Callahan Associates.

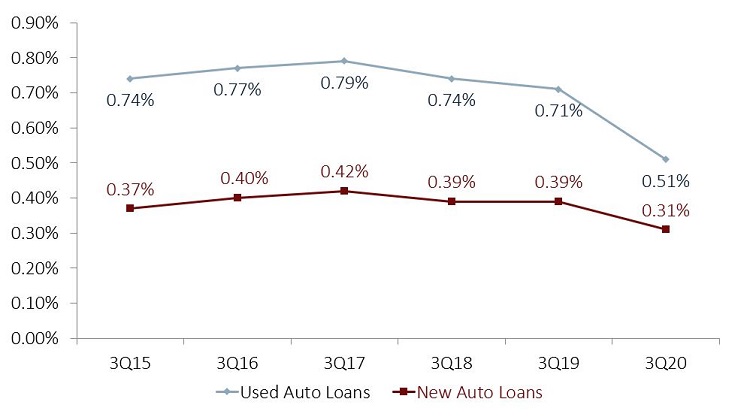

DELINQUENCY BY LOAN TYPE

FOR ALL U.S. CREDIT UNIONS | DATA AS OF 09.30.20

Auto loan delinquency dipped below mortgages in the third quarter. Despite falling sharply during the year, credit card delinquencies were the highest rate of any loan type.

Source: Callahan Associates.

<!– Left and right controls Previous Next –>

Share And Penetration

Auto lending continues to have the highest market share of any loan product for credit unions nationwide. Down 50 basis points year over year, auto market share at credit unions was 17.9% as of the third quarter, continuing a slide that began in the third quarter of 2018 when that metric peaked at 20.6%.

Comparatively, mortgage and credit card market share increased slightly over the past 12 months to 8.6% and 6.5%, respectively. Despite the slight decline in market share, auto lending continues to position cooperatives as competitive players in the national auto lending market.

The percentage of credit union members with an auto loan tied into their relationship, defined as auto loan penetration, fell 22 basis points in the past year to 21.1% as of Sept. 30, 2020. This is due, in part, to suppressed new auto loan supply during the onset of the COVID-19 pandemic and decreased consumer sentiment across the country.

Additionally, members continue to join credit unions through other product channels, particularly as indirect loan growth slows. Total credit union membership increased from 120.9 million in the third quarter of 2019 to 125.0 million one year later a 3.4% increase. During that period, net new member growth was largely through core deposit offerings (with the number of accounts increasing 4.4%), and mortgages on the lending side (accounts up 6.0% to 3.1 million).

At 21.1% auto penetration is the highest of any loan product. Credit card penetration as of the third quarter was 17.4% and first mortgage penetration was 2.5%.

Indirect Lending Growth Decelerates But Still Dominates

Indirect lending continues to be a major source of auto lending for credit unions, but that growth has contracted for two consecutive years. In the third quarter of 2018, indirect lending was up 15.5% year-over-year following two back-to-back years of growth exceeding 20%. That growth slowed dramatically to 4.7% in the third quarter of 2019 and then further to 1.7% one year later.

That said, the indirect channel still accounts for $235 billion, or 61.3%, of credit union auto balances. The slowing growth can be attributable both to an industrywide tendency to pull away from indirect lending channels in pursuit of higher-yielding originations, a trend that is amplified by historically low interest rates and decreased consumer loan production.

Loan Quality Improves Despite The Pandemic

Auto loan delinquency improved year-over-year, falling 14 basis points to 0.44% as of Sept. 30, 2020. In the past year, new auto loan delinquencies fell 8 basis points to 0.31%; used auto loan delinquencies fell 20 basis points to 0.51%.

Credit card and mortgage delinquencies also fell during the year, to 0.87% and 0.50%, respectively, as overall reportable delinquency improved across the country. This improvement in asset quality across all three major loan product types suggests payment deferrals, relief programs, and federal aid packages provided important support to help consumers decrease their debt burden in the face of economic uncertainty.

This article appeared originally in the Credit Union Times in February 2021.