A successful credit card lifecycle marketing strategy includes four stages: upfront account acquisition, near-term account activation, long-term usage maximization, and an empowered retention strategy. For a credit union to build and manage a successful credit card program, expertise must be built to engage, build upon, and retain relationships with cardmembers.

Acquisition is the first and most important step as it is the initial point of contact with a potential cardmember. This point of contact might happen in the branch with frontline employees, via email or direct mail campaigns, or through a web page. During the credit card account acquisition process, success is measured not only by the number of new accounts, but also by getting the right product into members’ hands.

The elements driving success at this stage are catching the cardmember’s attention with a targeted message at the most opportune time, and understanding the target audience for the card product and tailoring the message to that specific audience.

In the second stage of the credit card lifecycle marketing strategy, activation follows acquisition. After approving the member and delivering their credit card, the focus shifts to ingraining the card product into the cardmember’s day-to-day payment behavior.

Some steps during the acquisition phase that can help get a head start on activation include the development of appealing products, introductory APR rates, and reward point bonuses on new accounts. Activation starts in earnest as the marketing team mails out welcome kit materials, followed by special offers, PIN mailers, and cardmember opt-in to ongoing communications. These activities make up an motivates members to engage with their new credit card program in a specific timeframe.

Usage is the next stage in the lifecycle strategy. Once the cardmember is acquired and activated, usage focuses on driving top-of-the-wallet status and behavior, thus reducing the likelihood of the cardmember responding to a competing credit card offer. In today’s market, cardmembers are implored to use their cards under a constantly expanding universe of benefits at nearly every turn. Whether it’s rewards points, enhanced fraud protection, new technology integration, increased transparency/tracking, cardmember benefits, discounting or lower interest rates, there’s a definitive reason why an individual uses one card over another.

In order to remain competitive, credit unions must understand cardmembers and give them a reason to use that credit card, and then focus on reinforcing that message and providing incentives for continued use and loyalty. The more a cardmember uses your credit union’s card, the less likely they are to jump at a competitor’s offer and reduce their engagement with your credit union’s product.

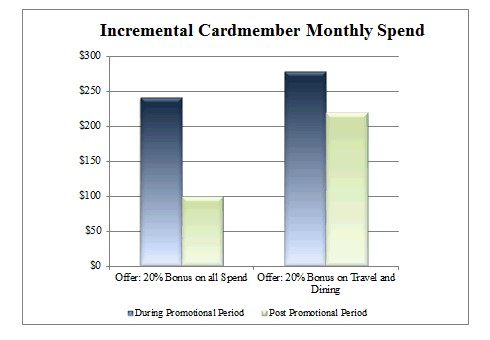

Below is an example of the increase in cardmember spend when they receive a marketing incentive offer such as earning bonus reward points during a three-month promotion period. This chart measures the cardmember impact both during the promotional period and the first three months following the promotion. For a point of reference, the average opt-in rates for these types of usage campaigns are usually around 10%.

Retention is the last stage and encompasses the goal on keeping your best cardmembers. A credit union makes a substantial investment in driving the acquisition, activation, and usage of cardmembers and going forward a credit union should show the discipline to protect that investment. Credit unions have to give cardmembers a reason to become loyal members.

Loyalty and rewards programs offer the most compelling reasons for cardmembers to keep using their cards. According to the J.D. Power’s 2015 U.S. Credit Card Satisfaction Study, rewards and benefits are the two main reasons cardmembers select a credit card and are key drivers of satisfaction and spend on a primary card. More than half of cardmembers surveyed selected their new card for a better rewards program and 24% did so for better benefits.

According to Gallup, the average American carries almost four credit cards. How can you ensure that your credit union’s card product will not only be among that population, but also be the card the member chooses to use the most? A strong focus on lifecycle marketing should help you feel more confident in the answer to that question.

For nearly 50 years, Elan has delivered a best-in-class credit card program, card products and exceptional service to its valued credit union partners. Today, Elan helps nearly 300 credit unions drive member engagement through a robust cardmember lifecycle marketing strategy. Year after year, our partners remain pleased with the Elan solution, as Elan has seen a more than 96% renewal rate. For more information, call 1-800-223-7009 or visit cupartnership.com.