To read a more in-depth analysis on specific 1Q20 industry trends, select a section below.

LOANS,MORTGAGES,AUTO LENDING,SHARES,INVESTMENTS,EARNINGS,MEMBER RELATIONSHIPS,HUMAN CAPITAL,COVID-19

The longest economic expansionary period in U.S. history came to an end in the first quarter with the onset of the COVID-19 pandemic. Real GDP decreased at an annual rate of 5.0% as personal consumption and business investment contracted across the quarter.The national unemployment rate increased 0.9 percentage points from February to March following the first wave of jobless claims related to the global pandemic.

Market turbulence prompted the Federal Reserve to adjust rates twice in March. The Fed also reinstated several financial crisis-era programs, including a $700 billion quantitative easing program, in a bid to stabilize a free fall in the equity marketsand ease liquidity challenges in the credit markets.

Key Points

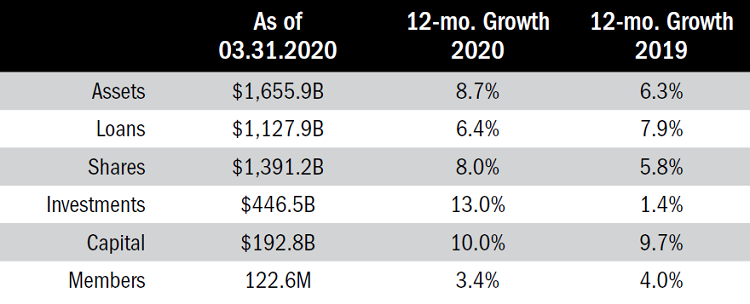

- As of March 31, 2020, over 5,200 credit unions held nearly $1.7 trillion in assets nationwide.

- Loan balances at U.S. credit unions totaled $1.1 trillion in the first quarter, an annual increase of 6.4%. Total loan growth slowed 1.5 percentage points in the past 12 months.

- Share growth accelerated 2.2 percentage points annually to 8.0% as of March 31.

- Membership increased 3.4% year-over-year as almost 4.0 million members joined the credit union movement.

- Average ROA fell 43 basis points during the past 12 months to 0.52%.

- The industry reported 34 mergers in the first quarter.

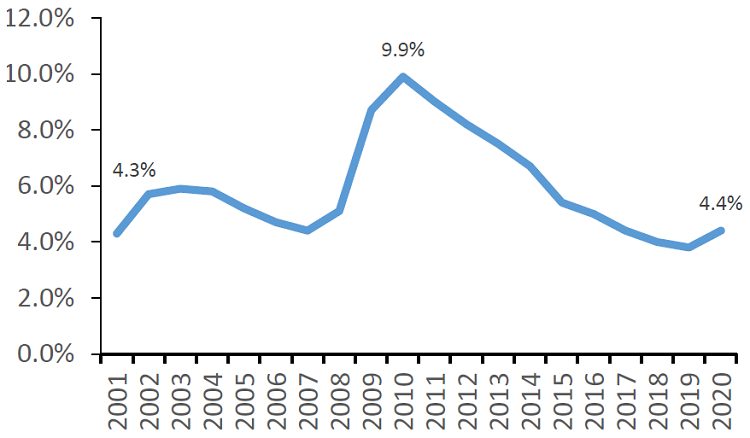

U.S. UNEMPLOYMENT RATE

DATA AS OF 03.31.20

Callahan & Associates | CreditUnions.com

In the United States, the unemployment rate ticked up to 4.4% in March 2020.

Source: Bureau of Labor Statistics

CREDIT UNION INDUSTRY OVERVIEW

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.20

Callahan & Associates | CreditUnions.com

Assets, shares, investments, and capital all grew at a faster annual rate than one year ago.

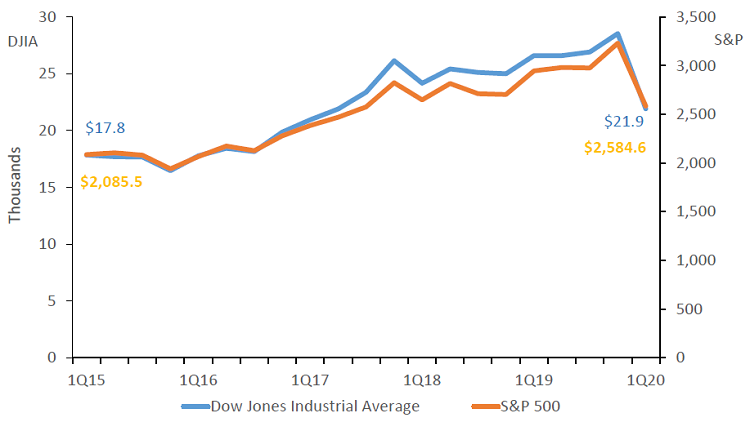

DOW JONES INDUSTRIAL AND S&P 500 AVERAGE

DATA AS OF 03.31.20

Callahan & Associates | CreditUnions.com

The Dow and S&P dropped more than 20% between the fourth quarter of 2019 and the first quarter of 2020, a sign of the pandemic’s impact on equity markets.

Source: Freddie Mac

The Bottom Line

As the economy lost steam in the first quarter, shifts in member behavior impacted credit union balance sheets. On a quarterly basis, increases in first mortgages offset contractions across nearly every loan segment except for used auto. Weak consumerdemand and strong share growth underpinned a 13.0% annual increase in investment balances, which hit $446.5 billion. Credit unions allocated un-lent shares mostly to short-term investments and cash. They now must grapple with a new normal and re-evaluateincome streams and service practices as they navigate an unknown future.

Without official data from the NCUA, Callahan is reporting first quarter data trends from institutions that represent 99.7% of the industry’s assets.

This article appeared originally in Credit Union Strategy & Performance.