Top-Level Takeaways

-

Arbor Financial Credit Union has grown loans, shares, members, and more through market expansion, mortgage loans, and high-interest savings products.

-

After a 2015 CEO change, a 2016 branding change, the credit union is poised for even more growth.

Four years ago, Arbor Financial Credit Union ($652.M, Kalamazoo, MI) was a different financial institution both by brand and by plan.

Known then as Educational Community Credit Union, the cooperative had a community charter for 21 counties that allowed it to serve more than educators; however, its name created a marketing barrier that limited its growth potential. Between 2010 and 2015, the credit union increased assets 24%, compared with a statewide growth rate of 41% over the same period.

We thought it would be good enough to say everyone could belong, says Earle Shelner, the credit union’s chief financial officer. But having the word Educational’ prevented members from even looking at us.

After a nationwide search to replace its retiring CEO, the credit union hired Julie Blitchok in March 2015. Blitchok previously worked for the state’s largest cooperative, Lake Michigan Credit Union ($6.5B, Grand Rapids, MI), as its senior vice president of retail operations. There, she saw firsthand how a large branch footprint again the state’s largest could affect growth.

Under her leadership, the credit union’s financials have taken off. In the second quarter of 2019, loan growth, share growth, and ROA far outpaced the average of asset-based peers. The credit union anticipates crossing the $1 billion threshold in slightly more than six years and more than doubling today’s workforce in another four.

New Markets And The Frontline

When Blitchok assumed the role of chief executive, she took stock of the organization to understand the challenges, opportunities, and talent she had inherited. Only then did she start looking ahead toward a new future for the cooperative.

She brought a positive energy to the organization, Shelner says. Now we are starting to execute on her vision.

In August 2016, the credit union rebranded to Arbor Financial. In doing so, it retained its color scheme but introduced aspirational imagery emblematic of the credit union’s future.

![]()

Arbor introduced a new name and logo in 2016. The name, which calls to mind trees, is emblematic of the credit union’s potential for future growth.

Arbor implies trees and trees grow, just like we’re growing by branching into new markets, Shelner says. Since the name change, we’ve heard from quite a few people saying finally we can join your credit union.

The credit union also has plans to expand its branch footprint outside its Kalamazoo home. It will open three branches in 2019 including the one in Grand Rapids it opened in August and two more each year for the next four years, according to Shelner.

Additionally, the credit union expanded its field of membership in 2018 and can now serve the entire state of Michigan. Before 2013, when the credit union assumed its community charter, the cooperative served nearly 30% of its potential members. Now, after two FOM expansions, that figure is down to 0.41%. But the credit union is adding members at a strong clip, and the drop in this metric underscores the potential presented by the geographic expansion.

Everybody talks about going digital and how members don’t want to see people, Shelner says. But they do. They want to know there is a physical presence if they have a concern or question or need someone to walk them through a process.

Because of this brick-and-mortar strategy, Arbor is dedicated to ensuring it has exceptional hiring and training practices. Hiring is a game of quality, not necessarily quantity, Shelner says. The new hire process now takes two months, which has its benefits as well as its drawbacks.

Growing as fast as we have can put a strain on resources, the CFO says. But getting the right people onboard, those who want to be here and fit out culture, is more important than just getting people onboard.

Although the hiring process has created a lag time in filling positions, turnover has decreased. And, as the credit union continues to expand its branch network, Shelner anticipates creating additional retail-focused roles that the credit union will fill internally, thereby creating career paths for good employees.

With internal promotions, they’ll have opportunity to grow, Shelner says.

Although a network of branches staffed with well-trained, dedicated front-line employees definitely has its service advantages, members stand to benefit even more through Arbor’s product expansion plans.

Arbor Financial’s Growing Years

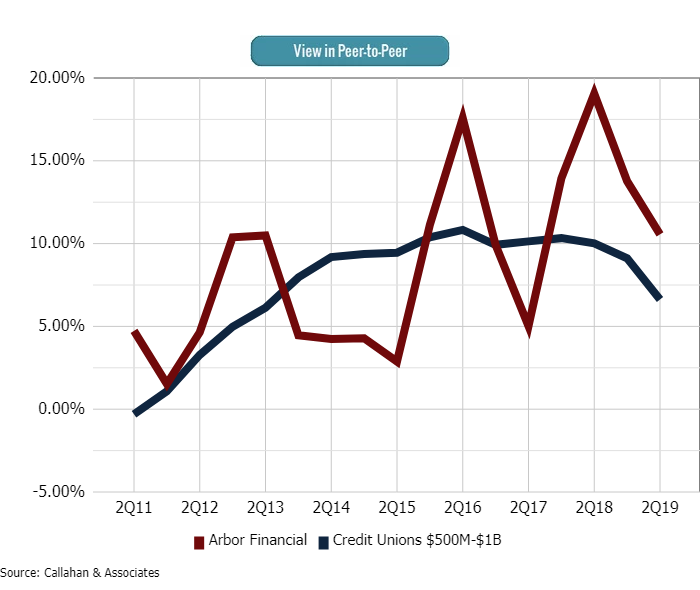

LOAN GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan Associates | CreditUnions.com

Mortgages are the largest segment of Arbor’s loan portfolio. They are also the fastest growing. In the coming years, as refinance activity increases, Arbor wants to position itself as the largest mortgage lending credit union in the state.

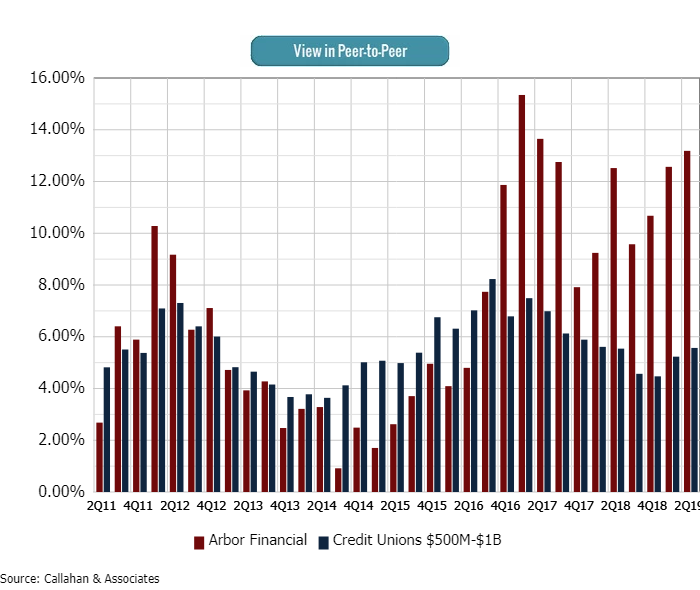

SHARE GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan Associates | CreditUnions.com

Arbor Financial launched its Momentum Checking account in late 2016; coinciding with the account’s introduction and a higher rate environment generally. The credit union’s share growth has far outstripped asset-based peer performance in the years since.

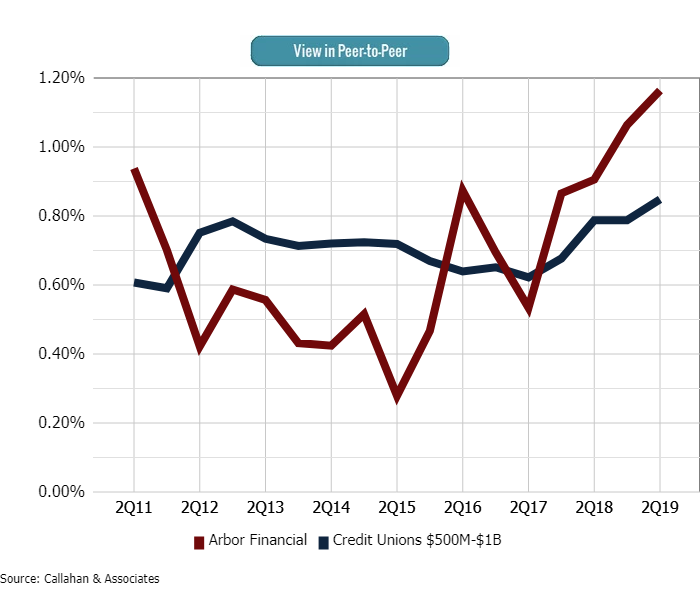

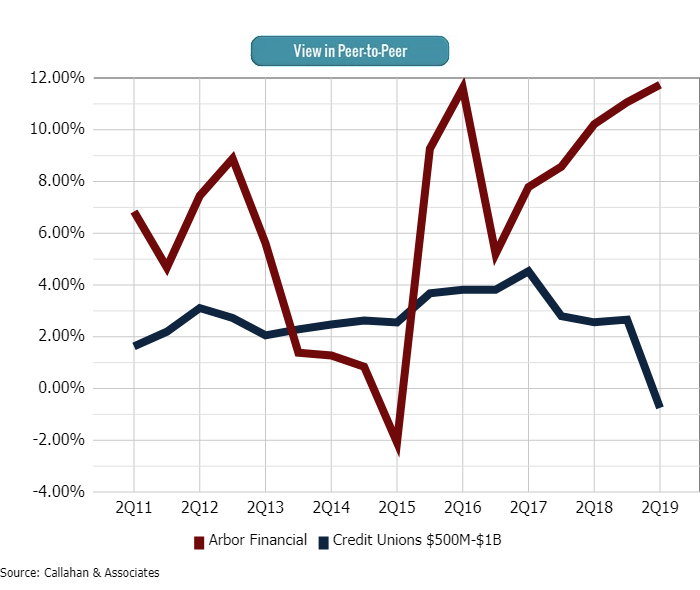

RETURN ON ASSETS

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan Associates | CreditUnions.com

Prior to new CEO Julie Blitchok taking the reins in early 2015, Arbor Financial’s ROA lagged behind peers. In the year’s since, it has risen nearly 100 basis points.

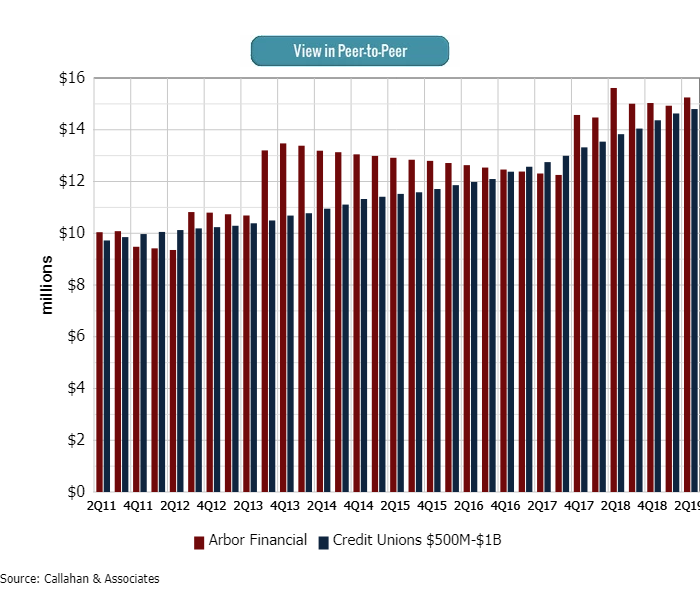

LAND AND BUILDING

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan Associates | CreditUnions.com

As part of a geographic expansion plan, the credit union will build three branches in 2019 and move into the Grand Rapids market. It plans to open two additional branches each of the next four years.

AVERAGE MEMBER RELATIONSHIP GROWTH

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.19

Callahan Associates | CreditUnions.com

Since 2015, Arbor Financial’s average member relationship growth far outpaces peer growth. As the credit union has introduced new products and services and keyed in on its rate strategy, members have responded by using more products at higher dollar amounts.

Savings And Mortgages

Arbor’s share growth of 13.2% in the second quarter put it at No. 26 among the 260 credit unions with $500 million-$1 billion in assets . In fact, the credit union has outpaced the share growth of asset- and state-based peers for the past three years, partly because of the current rate environment and partly because of the credit union’s response to it.

Arbor has picked up new deposits through high-rate certificate specials, adding some $50 million to its $122 million CD portfolio in the past 12 months. But the growth extends beyond this product. For example, in 2016, the credit union launched Momentum Checking, which resembles a high-interest checking offered at other credit unions but with an Arbor twist.

The credit union often stratifies its deposit products based on deposit amount and term, Arbor’s CD rate matrix includes 80 APY options and Momentum is no exception. The product has three tiers, and savers can earn a maximum of 5% APY if they keep a minimum balance and hit activity thresholds, including setting up direct deposit and opting into e-statements.

MOMENTUM CHECKING RATES

FOR ARBOR FINANCIAL CREDIT UNION | DATA AS OF 08.09.19

| Minimum Requirement | APY | |

|---|---|---|

| TIER 1 | 10-19 Debit Card Purchases; $0-$15,000 in balances | 1.00% |

| TIER 2 | 20-29 Debit Card Purchases; $0-$15,000 in balances | 2.00% |

| TIER 3 | 30 Debit Card Purchases; $0-$15,000 in balances | 5.00% |

Arbor tends to set its middle-tier rates close to market average, while its higher tiers have more aggressive rates.

The credit union increased the maximum APY from 4% to 5% in June to coincide with Arbor’s move into the Grand Rapids market. Shelner says he hasn’t seen any advertised rates this high, which leads him to believe this might be a point of differentiation. Anecdotally, the account has helped drive new memberships and higher debit card use, which is one of the qualifying activity thresholds. To qualify for the top tier rate, members must make a minimum of 30 transactions a month.

People think 30 is a lot, Shelner says.

However, the data suggests otherwise. Arbor’s Momentum debit card users average 43 transactions per month, compared to 34 for non-Momentum debit card users, Shelner says. The median for Momentum debit card transactions is 36.

Arbor historically has had a high checking account penetration, but even that has increased by more than five percentage points since it introduced Momentum Checking. In the second quarter of 2019, Arbor’s share draft penetration of 70.8% bested the performance of asset-based peers by approximately 14 percentage points. Perhaps more tellingly, the credit union’s Return Of The Member (ROM) metric, Callahan’s proprietary scoring systemthat provides a comprehensive measure of member value, is among the best of its asset-based peers. Part of the ROM calculation includes value returned to savers and member usage.

As of June 30, Arbor ranked 12 in ROM among 261 credit unions with assets between $500 million – $1 billion. Three years ago, before Momentum Checking, the credit union ranked 69.

Where Do You Rank?

Callahan’s Return of the Member (ROM) uses a single metric to showcase the value a credit union delivers to members relative to peers. Want to know where you rank? Request your ROM score today.

![]()

On the other side of the balance sheet, Arbor’s loan portfolio is mostly composed of mortgages, unlike other credit unions of its size and in its state. In the second quarter, these loans made up more than 60% of the credit union’s total portfolio. Shelner attributes the cooperative’s mortgage success to low rates and short-term fixed-rate products that drive refinance activity.

Arbor offers 7-, 10-, and 15-year fixed-rate products that have proved attractive to middle-aged borrowers looking to refinance. And as interest rates look primed to drop again, Shelner believes refinance activity will pick up in the next several years.

People who bought houses six or seven years ago are seeing rates come back down, which will drive refinances, Shelner says. There’s a lack of new homes of a certain price range available in our markets. We believe people will take out cash to remodel and add-on to what they currently own.

The credit union does not make indirect auto loans and its only recent merger occured in a small, NCUA-requested deal before Blitchok’s tenure. Its future growth plans are not based on either of those models; rather, Arbor’s plans for future growth are based on continuing what it already does well: savings and mortgages.

We’ll never be as big as someone like Quicken, but we believe we can be one of the largest mortgage players in the state of Michigan, Shelner says. That’s our plan.