Top-Level Takeaways

-

Consolidated Community has launched a security deposit loan and other housing products to help borrowers in pricey Portland.

-

Grant money provided by the Northwest Credit Union Foundation and CDFI Fund underpin these new housing products.

Consolidated Community Credit Union ($252.4M, Portland, OR) is an accomplished mortgage lender that is now taking on its local housing crunch by helping renters, too.

Consolidated has partnered with the Northwest Credit Union Foundation and two other local cooperatives $93 million Point West Credit Union and $120 million Trailhead FCU to offer a security deposit loan that is designed to help people find a better place to live.

“Consolidated’s website describes the loan as a way to remove the financial barriers of rental housing. The hot Portland market can make those barriers especially high,” says Consolidated president and CEO Larry Ellifritz.

According to Ellifritz, the average monthly rental of a one-bedroom, 764-square-foot apartment is $1,548; a three-bedroom house averages $2,752. And to buy? The average home price is $452,473. By comparison, Abodo puts the national median rent for a one-bedroom apartment at $1,025, and Zillow says the median home listing price in the United States today is $282,000.

It was a real eye-opener to see how underserved and almost abandoned this demographic is in our community. When a member is hugging you at the end of a loan closing, you know you’ve done something right.

Covering The Costs

“The unsecured loan covers two-thirds of move-in costs, including first and last months’ rent, pet fee, security deposit, and more,” Ellifritz says. “Borrowers can take out up to $5,000 with a term of one year and a rate of 4.99%. There’s a minimum credit score of 580 but no pre-payment penalty.”

“It’s a very well-priced product for someone who makes 60% of the average medium income in our market,” Ellifritz says.

The three credit unions, buttressed by a $150,000 grant the NWCUF was awarded by the Meyer Memorial Trust, have underwritten approximately 10 of these loans so far and plans to make 50 in the next three years.

Ellifritz says the loss ratio so far has been approximately 20%, but he doesn’t expect that to continue.

“We’ve learned a ton throughout the year and are projecting a loss ratio of 8% to 10% as the program evolves,” the CEO says.

The three Portland credit unions also are working with a group of Washington state cooperatives that want to offer the same product there, and the Portland trio has their eye toward taking the program national if possible.

Eye-Openings And Hugs

Consolidated might have thought it was simply offering a vehicle to put people into better housing, but the credit union soon learned what it was offering represented more than four walls and a roof.

“We typically don’t interact with these members on a daily basis, so it was a real eye-opener to see how underserved and almost abandoned this demographic is in our community,” Ellifritz says. “One of our most impactful loans was to a single father of two kids that wanted to move into a one-bedroom apartment. He and his kids [ages 7 and 9] had always lived in a studio apartment, so a one-bedroom unit seemed like a dream come true.”

For that member, a loan of only $2,500 helped turn his dream into a reality and made an outsized impact on his life.

“When a member is hugging you at the end of a loan closing, you know you’ve done something right,” says Ellifritz, who has worked at Consolidated for the past 25 years, at the helm for the past eight.

Spreading The Word

Consolidated is a well-established player in the local housing market, yet the rental loan is still an unusual offering because it’s geared toward renters and not buyers. It has opened the door to serve a whole new segment of borrowers but also has presented new challenges in outreach.

“This has been a struggle, finding the right entities to talk to about this loan product,” Ellifritz says.

According to the CEO, marketing so far has focused on local social media as well as community partners, nonprofits, housing authorities, other government agencies, landlords and property managers, the latter through a recently launched email campaign.

Although getting the word out has proved challenging, finding credit unions to participate with Consolidated in the loan’s pilot has not. Ellifritz says the loan was an easy sell to the three credit unions’ boards, and the clear impact the loans have had on borrowers’ lives has naturally increased the compassion of the lenders.

This product falls right in line with our values, the Consolidated CEO says.

So does a package of new mortgage products that Consolidated has rolled out to address the housing crunch in the Portland market.

That package includes:

- ITIN Mortgage Loan: For members who lack citizenship or permanent resident alien status.

- Accessory Dwelling Unit loan: Usually a second mortgage loan to build a second dwelling unit on a member’s property. Also, for rehab projects.

- The 100% Community Home Loan program: A 100% LTV loan designed to help a member who lacks a down payment.

“These are great loans that truly enable members to achieve homeownership sooner than expected,” Ellifritz says.

What’s more, each loan targets a specific situation, such as fast-rising home prices that can make it prohibitively difficult to come up with a 3.5% down payment required for an FHA loan.

“For that, we created the 100% Community Home Loan program that enables members to buy a home with no money down if the closing costs are gifted or the seller pays them,” Ellifritz says.

Using a $700,000 CDFI grant as a funding backstop for the three mortgage plans, Consolidated’s goal is to make $14 million in the 100% LTV loans in the next three years. It has made 10 totaling $3.3 million since October 2018.

“Knock on wood, they’ve all performed great,” Ellifritz says.

In fact, the Portland credit union’s first mortgage delinquency in the third quarter of 2019 was 0%, compared with 0.65% for its asset-based peer group, 0.28% for all Oregon credit unions, and 0.55% for all U.S. credit unions.

Addressing The Housing Gap

The credit union is working to make a significant impact on the affordability of housing, but Ellifritz says his shop doesn’t take credit for this creative approach to home lending.

“These programs were built by members,” he says. “We listened to their requests and built programs around their needs.”

He also lauds Sharee Adkins, the NWCUF executive director, for coming up with the idea for the security deposit loan, Ellifritz says, and pursuing the grant that made it possible.

The NWCUF is due all the credit, he says.

Together the rent deposit and mortgage loan products address what Ellifritz calls a huge product gap for first-time homebuyers and renters with less-than-perfect credit.

These groups are left to pick from a sub-standard product set, the Consolidated CEO adds. Many financial institutions prey on these individuals, and that’s unforgivable. We offer great products so they can thrive rather than start the homeownership journey with two strikes against them.

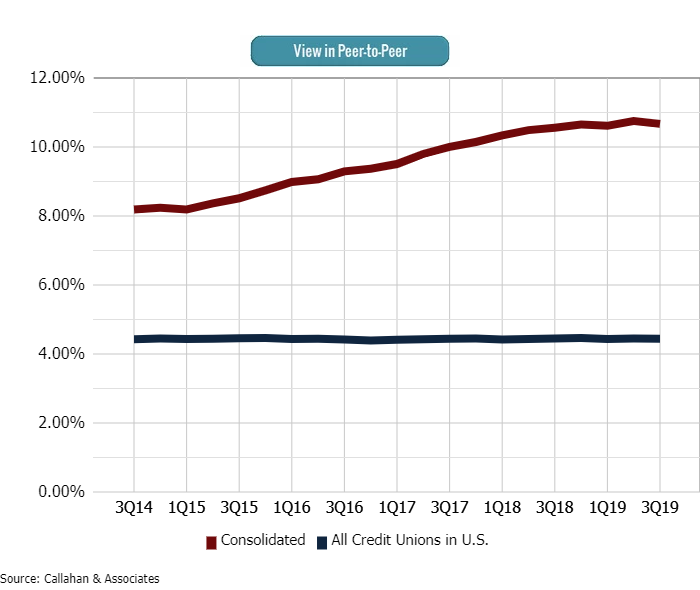

REAL ESTATE LOAN PENETRATION

FOR U.S. CREDIT UNIONS | DATA AS OF 09.30.19

Of Niches And Partnerships

Larry On Lending

Consolidated Community president and CEO Larry Ellifritz shares best practices for how to create and manage a lineup of lending products that serve an economically diverse membership.

- Hire experienced, savvy lenders that have a background in the specific loans the credit union wants to originate.

- Talk to many lenders before launching a new loan product.

- Go slow. Build in runway to make pivots in the program rather than discontinuing the program at the first pivot.

- Reserve intelligently for loan losses. Don’t be stingy.

- Pay lenders what they’re worth or they’ll find another financial institution that will.

“We’re a $250 million credit union, so we have to be good in our niche, and the niche we have chosen to specialize in is real estate lending,” Ellifritz says. “We decided it’s the way we could have the greatest impact on our members’ lives.”

And to the benefit of the credit union’s members, Consolidated takes a broad view of real estate lending, one that goes beyond its direct market and field of membership. Indeed, the cooperative operates a subsidiary, Consolidated Mortgage Group, that provides support for government-sponsored mortgage and other services to fellow credit unions in six states.

“CMG processed 854 mortgage loans for more than $250 million last year, the most it has ever processed in one year. And, for the first time in its 22-year history, more of those loans were for partner credit unions than for Consolidated itself,” Ellifritz says.

“The mix was about 60/40 partners to Consolidated loans,” Ellifritz says.

Of the subsidiary’s growth, the credit union CEO adds, “Like all things credit union, one CEO talked to another, and now we serve 40 credit unions with more than $2.5 billion in combined assets. I’m amazed how the program has grown, and we’re humbled to serve this great group of member-owned cooperatives.”