Cybersecurity Is Under Fire And Credit Unions Are Fighting Back (Part 1)

Bad actors don’t rest. Credit unions are beefing up cybersecurity with smarter tools, stronger teams, and sharper defenses.

Lower prices and better amenities are making pre-built homes an appealing option for credit unions looking to bolster their balance sheet and borrowers stymied by the affordable housing crisis.

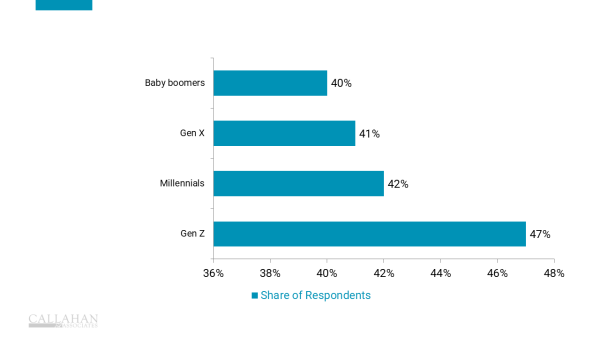

Data from Vanguard shows retirement preparation declines with age, leaving no generation fully ready. The gap presents both a challenge and an opportunity for credit unions.

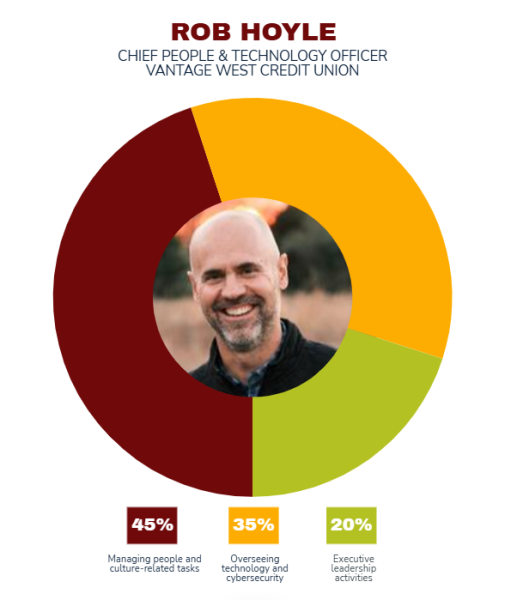

It’s not every day a technology leader takes over HR. Vantage West’s Rob Hoyle explains why the two disciplines are linked now more than ever.

Rising credit union benefit costs don’t have to remain a permanent operating burden.

Look beyond the headlines to better understand what is driving current market trends and how they could impact credit union investment portfolios.

From macroeconomics to multiculturalism, the future of AI, and more, the second day of this year’s convention was packed with insights.

From new attitudes to new ways of thinking about service delivery, here’s a look at the first day of the industry’s biggest event.

Storytelling drives growth and loyalty at Navy Federal, where real member experiences become narratives that strengthen trust, reinforce value, and build lasting relationships.

From where stories come from to how they’re produced and distributed, Lake Trust shares how authentic member narratives strengthen its brand and show what “positive impact” looks like in action.

An expert in user experience turns complex problems and opportunities into narratives that guide leaders toward confident decisions and growth-focused investment.

RBC2: Only One Mind To Change