A family can be working and paying the bills and still be one car repair away from crisis. For millions of U.S. households, financial hardship feels just as precarious as poverty, yet their numbers are undercounted by official measures.

Federal poverty level (FPL) guidelines vary by household size but rely on a single national baseline for the continental United States, regardless of wide differences in local cost of living. Only Alaska and Hawaii have separate guidelines. Additionally, although the FPL is adjusted each year for inflation, the underlying methodology and assumptions used to calculate the poverty guidelines date back to the 1960s and have not been fundamentally reworked to reflect modern spending patterns and economic realities. Today, essentials such as housing, healthcare, childcare, and transportation comprise a far larger share of household budgets than they did back then.

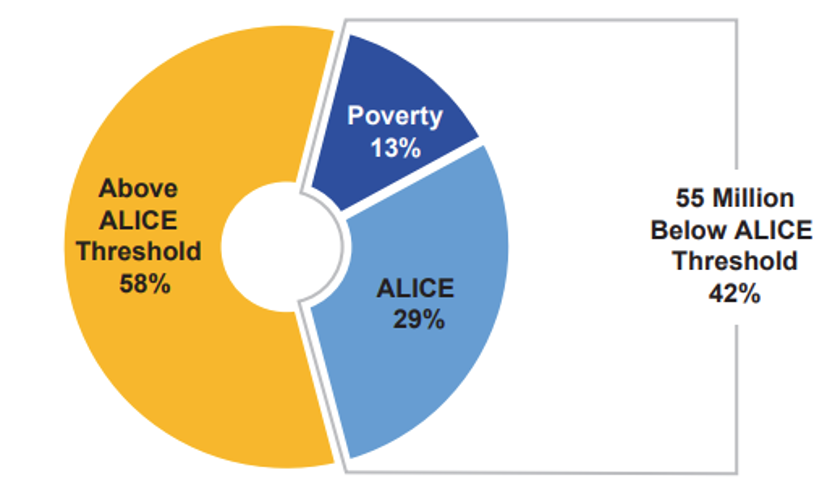

To address this gap, the United Way of Northern New Jersey developed a way to capture the households that earn more than the federal poverty level but still struggle to afford basic necessities. The ALICE (Asset Limited, Income Constrained, Employed) framework calculates a Household Survival Budget based on the localized cost of basic necessities such as housing, childcare, food, transportation, healthcare, technology, taxes, and more for every county in the United States. It then compares that budget with household income sourced from the U.S. Census Bureau’s American Community Survey to establish the ALICE Threshold and provide a more accurate picture of financial hardship.

According to the 2025 State of ALICE Report, the cost of household necessities plus taxes greatly outstrip FPL guidelines. Thus, households below the ALICE Threshold must make difficult decisions every day. They often earn too much to qualify for public assistance but not enough to comfortably afford necessities like groceries, car repairs, and medications, placing them between a rock and a hard place.

SHARE OF U.S HOUSEHOLDS ABOVE AND BELOW ALICE THRESHOLD

FOR U.S. HOUSEHOLDS | DATA AS OF 2023

SOURCE: United Way, U.S. Census Bureau

Strategic Insights

- The K-shaped economy continues to define the post-COVID landscape. According to Axios, 59% of all consumer spending in the United States comes from just the top 20% of income earners.

- Money markets reflect this inequality as well. Bloomberg claims the top 1% of U.S. households now hold close to one-third of the nation’s wealth, the highest level since World War II.

- Widening inequality helps to explain deteriorating consumer sentiment; many people simply have not seen improvements in their standard of living. The University of Michigan Survey of Consumers expects consumer sentiment to fall to all-time lows of 47.6 in April 2026, driven by stubbornly high inflation expectations and the Iran conflict.

- When money stops making sense, people suffer a crisis of financial confidence. That’s when financial nihilism can take hold.

- According to JD Power’s March Banking and Payments Intelligence Report, 68% of U.S. consumers are considered financially unhealthy with one-third expecting their financial situation to worsen over the next three months. The vast majority have changed spending habits, purchasing less expensive grocery items or even less food overall.

What Can Credit Unions Do?

- In Tucson, a handful of credit unions have paired up with their state credit union association’s foundation to make housing more affordable. Read more today.

- DuGoood Federal Credit Union is strengthening local households through a workforce partnership that combines products, education, and philanthropy to support job training and technical education. Read more today.

- Holy Rosary Credit Union is giving young people a leg up before they enter the workforce and establish their own households. Its career and technical education program offers scholarships, internships, and courses eligible for college credit. Read more today.

- Nuvision Federal Credit Union’s Added Advantage program tracks member engagement across the credit union, then rewards relationships through better pricing and other perks, easing the stress some households face. Read more today.