This is part of the Callahan Financial Performance Series. Presented by the analysts at Callahan & Associates, the series helps leaders interpret data to drive smarter decisions and uncover new approaches to measure performance. Callahan clients can access the full version of this article right now on the client portal. Read it today.

The nationwide affordability crisis has become an inescapable issue for credit union members, affecting how they borrow, spend, and plan for the future. From housing and vehicles to education and everyday essentials, the cost of daily living is on the rise, leaving many households struggling to save, qualify for loans, and manage debt.

In today’s economy, it is essential that credit unions balance member support with sustainable lending practices that ensure continued operations for those in need.

Housing Prices Reposition The Real Estate Portfolio

Housing prices are climbing faster than wages in many regions, and members are struggling to save for down payments, qualify for mortgages, or comfortably manage monthly payments if they do buy.

FIRST MORTGAGE GROWTH

FOR U.S. CREDIT UNIONS

SOURCE: CALLAHAN & ASSOCIATES

At the same time, other residential real estate products — namely HELOCs — have surged. Existing homeowners are increasingly tapping equity for not only home improvements but also to pay down student loans, consolidate high‑interest debt, and cover unexpected expenses.

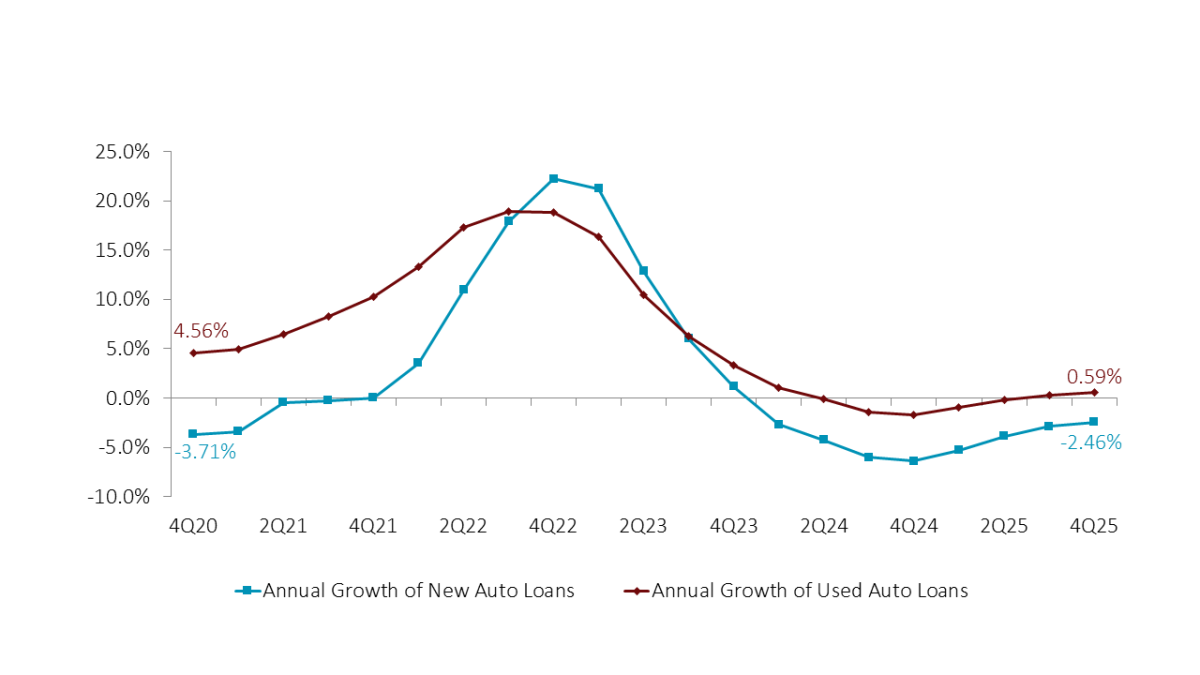

New Pressures Drive New Lending Plays

Higher sticker prices, rising interest rates, and longer loan terms mean monthly car payments now consume a larger share of already-strained household budgets for longer.

NEW AND USED AUTO LOAN GROWTH

FOR U.S. CREDIT UNIONS

SOURCE: CALLAHAN & ASSOCIATES

Considering the affordability concerns with new cars, used auto — traditionally the more budget-friendly option — remains the dominant vehicle loan. However, even the average used car loan balance has increased 3.0% at credit unions since last year, suggesting new loans for used auto are larger than they used to be. That can be a major barrier for members in need of new transportation.

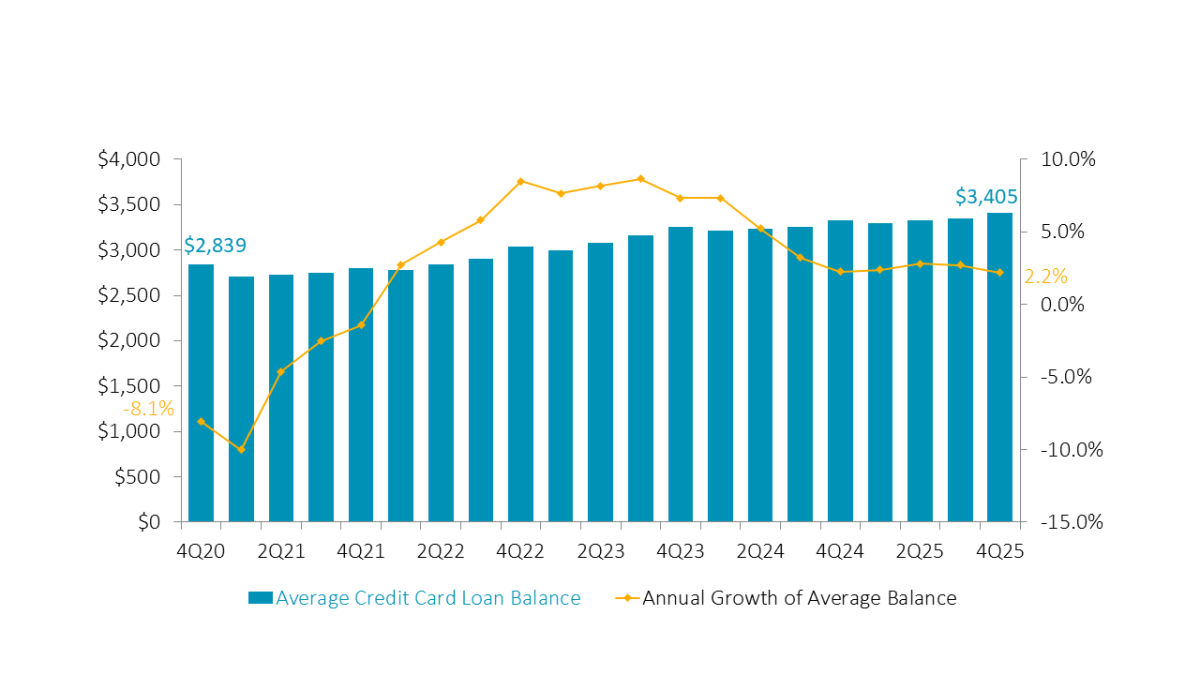

Swiping Through The Squeeze

Credit cards have become a financial lifeline for credit union members as inflation continues to chip away at household purchasing power. With essentials costing more each year, members are paying with plastic to bridge gaps in their monthly budgets. As such, average credit card balances were up 2.2% annually $3,406 at year-end 2025.

AVERAGE CREDIT CARD LOAN BALANCE AND GROWTH

FOR U.S. CREDIT UNIONS

SOURCE: CALLAHAN & ASSOCIATES

The Ripple Effects Of Rising Costs

These are simply two drops of water in the bucket of debt that has the potential to really soak members. As pressures compound across housing, transportation, education, and everyday spending, many members operate with thinner wallets and greater exposure to unforeseen challenges. That shrinking financial buffer plays a growing role in asset quality as slower repayment from tighter budgets presents higher delinquency risk.

On the opposing side, these compounding affordability challenges underscore the importance of proactive support as members navigate an increasingly demanding economic landscape.

Affordability pressures might show up first in individual products, but their cumulative impact is ultimately reflected in member behavior and portfolio performance. Credit unions must strive to not only manage risk but also recognize how interconnected cost pressures reshape both financial resilience and lending outcomes.

Ready To Read The Full Story? Callahan clients can access the full version of this article right now on the client portal. Read it today. Not yet a client but looking for expert insights to help you adapt to change, develop your organization’s leaders, and stay at the forefront of industry trends? Connect with our team to learn more.