The U.S. economy has fared well relative to expectations coming into the year. There were 1.6 job openings for every jobseeker in June, underscoring the labor market’s resilience. Economic activity as measured by GDP grew at a 2.1% annualized pace in the second quarter, beating expectations of 2.0% growth.

Despite the strong top-level growth, economists pointed to a reduction in consumer spending as a point of concern. However, the slowdown in spending was not as drastic as many feared and is the expected response to the actions taken by the Federal Reserve as it works to tame inflation. Speaking of, inflation slowed in the quarter, fueling optimism for a soft landing as GDP and inflation continue to trend in opposite directions.

Don’t Miss Out! Callahan’s quarterly Credit Union Strategy & Performance is available for download in the Callahan Client portal today. Not a client? Learn how you can gain access to our award-winning publications, intuitive benchmarking tools, collaborative networks, and more.

Key Points

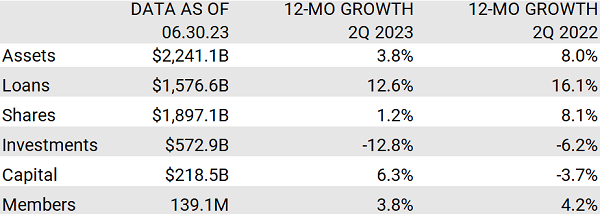

- Total assets at U.S. credit unions increased 3.8% year-over-year but only 0.3% since March 31 — the slowest quarterly expansion in almost a decade.

- Credit unions added 5.1 million members during the past 12 months. Membership reached 139.1 million at midyear, representing 3.8% growth.

- Share balances outstanding increased 1.2% annually, hovering near historic lows. Loan balances rose 12.6% over the same period, pushing up the loan-to-share ratio 8.4 percentage points. Credit unions lent 83.1 cents for every dollar on deposit.

- Revenue for the industry grew 33.4% year-over-year as margins repriced to higher rates, but an increase in expenses across the board reduced industry ROA 7 basis points to 0.79%.

Performance At-A-Glance

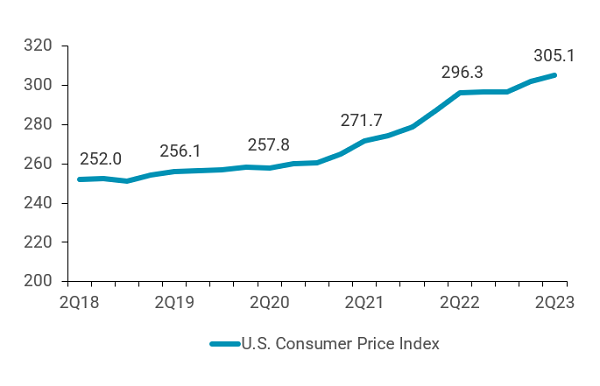

U.S. CONSUMER PRICE INDEX

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.23

© Callahan & Associates | CreditUnions.com

CPI inflation slowed to 3.0% in June, a welcome sign for consumers worn down by higher prices.

U.S. REAL GDP

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.23

© Callahan & Associates | CreditUnions.com

Real GDP increased 2.1% (annualized) quarter-over-quarter, aided by higher government spending.

CREDIT UNION INDUSTRY OVERVIEW

FOR U.S. CREDIT UNIONS | DATA AS OF 06.30.23

© Callahan & Associates | CreditUnions.com

Loan balances rapidly expanded as early paydown rates slowed. Relatedly, inflation strained member budgets, making deposit funding hard to come by.

The Bottom Line

Credit union earnings benefitted from rate increases by adding high-yielding loans to their balance sheets, which expanded top-line revenue. However, correspondingly higher funding costs offset some of these gains on the margins.

Credit unions also set more money aside for future losses, leaving themselves well-covered in the event of an economic downturn. For institutions with sufficient liquidity, booking loans at these rates should benefit their bottom line and allow them to build necessary capital. That is easier said than done in a low-savings environment, but cooperatives have reason to be optimistic. Members are joining at record rates even amid a cooling economy, and members’ financial health is normalizing after a few rocky years.

Measure Your Success With A Free Performance Scorecard

Develop a clear picture of your credit union’s performance with a complimentary scorecard from Callahan & Associates. Armed with your desired KPIs plus a few we might suggest, you’ll be in a better position to benchmark against desired peer groups and share findings with your board.