The Nevada gaming industry generated $11 billion in revenue last year, according to the University of Las Vegas. More than half of that money came from casinos in the state’s northern Washoe County.

Such earnings are an undeniable testament to the gaming industry’s mastery of the odds, with mathematical formulas that ensure no matter the game or gambler, the house will given enough time always prevail.

Credit unions work toward a different outcome from casinos in that their main goal is to put money back into their communities through affordable financing and philanthropic support.

Yet as the success of Greater Nevada Credit Union ($541M, Carson City, NV) proves, cooperative business can still operate in a way that tips the scale toward more consistent success.

Here, Greater Nevada shares seven ways it has changed its product line, operations, and technology to better achieve consistent, stellar performance.

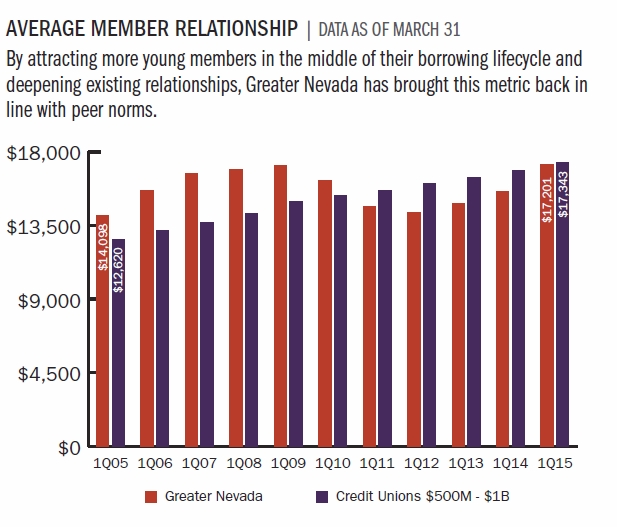

Source for all graphs, rankings, and maps unless otherwise noted: Peer-to-Peer Analytics by Callahan & Associates

1. Put Lending Front And Center

1. Put Lending Front And Center

The challenges Greater Nevada faced during the Great Recession demanded it evolve in a number of ways, including in its focus on direct lending.

In 2008, we were probably averaging about $10 million a month in indirect production versus $1 million to $2 million direct, says Dean Altus, Greater Nevada’s chief operating officer. Now, we’re about $8 million to $9 million in direct and $2 million to $3 million in indirect.

The credit union also now operates under a centralized consumer lending model, meaning when members visit a branch for a loan, branch staff connect the member by phone to one of five dedicated originators spread across the organization’s footprint.

The routing system will ring whoever is not already on the phone, Altus says.

Depending on how simple or complicated the scenario, lending staff members can answer loan queries within minutes and possibly close the same day.

These reps also handle electronic loan applications with signatures through DocuSign, which is how 20-30% of the organization’s total loan volume comes in each quarter.

Although the credit union was concerned initially that members would miss face-to-face interactions, they haven’t resisted the new process, says Marcus Wertz, vice president of consumer lending.

And despite the fact lending team members are separated geographically, iDashboards on the employee intranet which update every 30 minutes and provide companywide goal tracking as well as by-name ticker tape announcements of individual successes keep the institution’s sales and service culture going strong.

These are a great motivational tool and help create exposure throughout the credit union, Wertz says, adding that the individual branches, business services, indirect lending, and ancillary service departments all have their own dashboards as well.

When we’re hiring, we want the kind of people that are driven by this stuff, he continues. They want to see their name and how they rank and all the glory that goes along with saying, I helped 120 members accomplish their financial dreams this month.’

On the indirect side, especially, this tracking helps determine which dealerships are feeding the credit union the most loans. That’s important because premier partners get special opportunities such as displaying cars in the credit union’s branches.

We just had some dirt bikes, we’ve had hot tubs anything that might resonate with our borrowers and remind them that we offer financing for just about anything, Wertz says.

2. Make Friends With The Mortgage Company Next Door

2. Make Friends With The Mortgage Company Next Door

Greater Nevada itself has no real estate origination or processing staff, yet it has built a healthy portfolio thanks to the hard work of its wholly owned CUSO, Greater Nevada Mortgage, which leases its accounting, HR, and IT functions as well as its facilities from the credit union.

James Anderson heads up this company, which was established in 2001. Before joining Greater Nevada Mortgage, Anderson originated government and other specialized loans as well as built realtor relationships and formed partnerships with credit unions through a mortgage bank. Prior to that, he ran all mortgage lending for seven years as the vice president of real estate for Golden 1 Credit Union.

The credit union formed the CUSO with an initial investment of $300,000. Greater Nevada Mortgage currently has close to a $700 million servicing portfolio and more than $3 million in capital, with few delinquencies and strong contributing earnings to Greater Nevada’s financials.

We’re the fourth-largest mortgage producer in Northern Nevada by unit and the fifth largest by volume, Anderson says. And that’s just in Northern Nevada.

The CUSO typically sells government and jumbo loans to correspondents and releases servicing and the asset. It sells conventional loans to Fannie Mae yet retains servicing.

It also sells a portion of serviced loans to the credit union depending on its current appetite.

So far in 2015, that’s averaged approximately 20% of total loans serviced, consisting mainly of conventional first mortgages.

This symbiotic relationship lets the credit union avoid the risks of a huge portfolio yet build member relationships through products and services it might not be comfortable offering as a credit union, Anderson says.

Two examples of Greater Nevada’s production-focused dashboards.

The CUSO’s main goal for the rest of the year is to exceed $160 million in production, compared to last year’s roughly $100 million, and a big resource for getting there will be its 5/5 ARM.

Based on a similar product developed by LBS Financial Credit Union ($1.2B, Long Beach, CA) Greater Nevada Mortgage customized the 5/5 by adopting a two-year window for short sale waiting periods compared to the standard three to four years.

We had a lot of borrowers that went through hard times but are still good credit risks, Anderson explains. Those longer waiting periods were a little extensive for our market.

The 5/5 option also appeals to those who simply don’t plan to be in their homes for very long, such as miners or transient professionals.

Another big goal for the CUSO this year revolves around awareness. Twice a year it uses a third party to survey area realtors and builders. Last year, it ranked in the low 70s but is aiming to expand that to approximately 80% in 2015.

3. Deploy A Give-And-Get Deposits Strategy

3. Deploy A Give-And-Get Deposits Strategy

Greater Nevada currently offers three types of checking, two of which have rewards, Altus says.

Additionally, students, teachers, and parents of Carson City High School can opt to get a student-designed Senator debit card the result of a design contest from a few years ago on any of the accounts.

To date, the accounts include:

- Aspire Checking This account targets members who have extra money to park. It offers a 2.5% interest rate on $10,000 or less in deposits and rebates foreign ATM fees pending certain qualifiers, including 15 or more debit swipes per month. According to Altus, these accounts average approximately 40 swipes per month and their profitability is high despite the higher interest rate and fee rebates.

- Rock Checking This option features a stylish black card and targets a younger demographic. Instead of a high interest rate, those who swipe 15 times or more per month earn either iTunes or Amazon credits in addition to foreign ATM fee rebates. Students can also qualify for an alternative version of the account with lower requirements. Users of this product typically average more than 30 swipes a month.

- Connect Checking This streamlined product only requires four debit card swipes per month to avoid the service fee. However, users typically average approximately 15 swipes per month.

The respective designs for each of Greater Nevada’s card offerings.

Greater Nevada is different from most credit unions in that it charges a monthly service fee for all the accounts. The fee, however, has not stopped the credit union from reaching a penetration rate of more than 62% among its members, thanks in part to the fact it gives control of the fees back to the end user.

Once you qualify through certain behaviors, such as e-statements and a certain number of debit swipes each month, the service charge goes away, Altus says. So almost all our members get checking for free, but there’s a few things we want to see behaviorally before that happens.

4. Focus On First Timers and Second Chancers

4. Focus On First Timers and Second Chancers

Positioned in one of the hardest-hit Sand States, Greater Nevada has deepened its credit tiers to do more for those on the fringes of financial services.

For example, Greater Nevada established its credit rebuilder and first-time borrower programs at the request of members and leans heavily on financial education coursework from BALANCE to keep the costs of these products more manageable for borrowers.

Each module takes 30 minutes to an hour to complete, but the benefits and information borrowers receive from them are invaluable, Wertz says.

In addition, these programs’ guidelines require the credit union to reach out to participating members after 12 months of successful payment to try and refinance them at a reduced interest rate.

Since 2010, the credit union has also offered private insurance from Open Lending on certain member loans, particularly those with higher loan-to-value ratios. Such risk mitigation on the consumer side is especially critical given the credit union’s large yet calculated steps into other areas like business lending.

Thanks to robust pricing tools which factor in cost of funds, estimated losses, and servicing expense to help establish a price congruent with the added risk Greater Nevada typically sees a 175-basis-point return after net cost, Wertz says.

Over on the real estate side, the credit union’s CUSO offers a program called Greater Access, which is part of a larger correspondent relationship that provides funds in support of home ownership.

Different from more traditional down payment assistance programs, which offer a flat rate with no associated credit, Greater Nevada’s program is an FHA first mortgage with a silent second behind 3% of the purchase price, Anderson says.

Depending on the rate the borrower chooses, they can get a 5% contribution toward the down payment and closing costs instead of the 3% assistance, he says.

5. Tap Or Call, But Never Fail To Connect

5. Tap Or Call, But Never Fail To Connect

Greater Nevada has for a long time provided online banking, and in 2012 it enhanced its digital offerings with the addition of mobile. Today, approximately 50% of its members use remote access, Altus says, and roughly one in five consumer loan applications come through a digital channel. Members can also open accounts this way.

Despite these advances, the credit union never wants its out-of-sight members to feel out-of-mind. That’s why in 2014 it created an outbound calling department separate from its inbound service center.

Trying to do outbound from an inbound call center is tough when call volume is heavy because your outbound callers get pulled into the inbound side, Altus says. We didn’t want to see that happen.

Today, this three-person team contacts every new member that signs up in the branch as well as all those who come in through indirect and self-service channels.

These calls typically occur a few weeks after an account opening and introduce the credit union to the member. Agents ask members about their experiences so far and answer questions.

The overwhelming response from the members who are getting those calls is appreciative, Altus says.

And thanks to additional capabilities gleaned through the credit union’s new data warehouse, this group can also leverage information they have on existing members to further deepen the relationship, says Kerstin Plemel, vice president of marketing.

For example, one particularly successful call campaign targeted members who had $5,000 or more in their savings account.

We got a list of members we could serve better by looking at a certificate or money market account or by speaking to someone in financial services, Plemel says. We got some good leads out of that. But the only reason it worked so well is because we made sure this was a service call and an effort on our end to find a better solution for the member.

6. Mine The Core

6. Mine The Core

In 2009, in the depth’s of the Great Recession, Greater Nevada got the news its core provider, Fiserv, would be sun setting the credit union’s legacy system.

Although the timing was a challenge, the conversion was also a blessing in disguise, says Linda Barker, the credit union’s vice president of information technology, who joined the establishment in 2011.

Barker’s first day on the job directly coincided with the kickoff of the selection process for a new core, giving her a front-row perspective as to where the credit union could do a better job maximizing the value of its new investment.

Representatives would come in and we’d say, We want the system to do X, Y, and Z’ and then the specialist would say, Well, your current system can do that too, but you’ve chosen not to turn that feature on.’ So those sessions were a real eye-opener for us, she says.

We don’t talk about vendors around here, we talk about business partners because those are different. When you have a true partner, you’re not afraid to expose your plans and dream the dream right along with them.

In the end, the credit union signed with the OSI DNA platform, which Fiserv has since bought. After converting more than 20 ancillary systems including online banking and a reconfigured mobile product Greater Nevada officially went live on its new core November 1, 2014.

Barker now spends much of her time and effort ensuring the organization maximizes this resource to the fullest degree.

I was at a Fiserv conference recently and they were talking about how no one has time to invest in these large, once-a-year releases that core companies put out, even though they add a lot of functionality, she says.

To avoid overlooking those opportunities, the credit union is forming a release committee whose members will track and study the features offered with each update. If they choose not to take advantage of an offering, they’ll need to present a case to the executive team to justify that exclusion.

It sounds rudimentary, but many organizations ignore these resources only to end up paying extra for maintenance and work arounds later on, Barker says.

In between releases, the committee will help test and develop procedures and training so employees are able to put these new resources into play.

Because it has access to the DNAappstore where other credit unions on the same core can develop and sell their own enhancements Greater Nevada has been busy testing out many of these solutions, all of which come with a free 60-day trial.

Barker has bought six apps and has signed up the entire VP team for the app store newsletter so they can help her identify options that would aid them in their respective departments.

In addition, the credit union has hired a new vice president of e-commerce, whose role revolves around member-facing technology touch points.

This includes managing a phased rollout to EMV as well as the release of ApplePay, which the credit union released in March. Deploying such bleeding edge technology can be nerve-racking, but Greater Nevada is committed to leveraging all the resources and partnerships at its disposal to get these efforts right.

We don’t talk about vendors around here, we talk about business partners because those are different, says CEO Wally Murray. When you have a true partner, you’re not afraid to expose your plans and dream the dream right along with them.

7. Your Branch, Your Way

7. Your Branch, Your Way

Greater Nevada has increased its branch network by one-third in the past 12 months. The credit union is a believer in this delivery channel but notes it only gets out of its branches what it puts in.

None of our locations look alike, and that’s on purpose, Murray says. When people take the time to come somewhere, I’m not convinced that they’re still looking for a commoditized look and feel. I think they’re looking for answers to a need and those answers will be different based on where they live.

Efficiency is still top of mind, of course. For example,the organization’s newest branches are transitioning to cash recycler-equipped teller pods as an alternative to the traditional teller line. And thanks to its conversion to a more tablet-friendly core system, Greater Nevada is also looking at deploying more mobile technology throughout its locations following a system update sometime next year.

These changes will enable us to use smaller spaces, such as our 1,800-square-foot storefront branch in Northwest Reno, and still have people walk in and say Wow,’ says Joyce Whitney-Silva, the credit union’s chief financial officer.

Examples from across the credit union’s footprint show a tailored approach to branch design.

Last month, the credit union also opened its first in-store branch at a Walmart Supercenter in the central Nevada city of Elko.

Being a smaller town, there were not a lot of real estate opportunities, Whitney-Silva says. So we thought it would be the ideal opportunity to see how this model might work for us in certain scenarios.

Greater Nevada partnered with Financial Supermarkets, Inc., to secure the deal and leaned heavily upon that company’s expertise in regard to staff training, displays, and other factors the credit union had to adapt to Walmart’s brand environment and culture.

Another learning experience was the credit union’s new stand-alone location in Golden Valley. As a former Blockbuster building, the 5,000-square-foot space was far more than the credit union needed, yet the owners of the building did not want to split it up.

After negotiating an incredible rental price for the entire building, the credit union found a local eye care doctor to sublease approximately 40% of the building.

When you’re working with a landlord, you will lose some elements of control, Whitney-Silva says. Yet in this scenario, it was worth it from a balance sheet perspective.