Key systems conversions and hardware purchases can be like a game of Jenga, where players build up a tower using blocks from its foundation. Move the wrong block at the wrong time and the whole thing tumbles. But unlike Jenga, credit union technology permits moving multiple pieces at once.

We did a lot of conversions last year, all launched simultaneously and run concurrently, with a live date of August 1, says Sam James, vice president of information systems and technology for Mobiloil Federal Credit Union ($407M, Beaumont, TX). This included the conversion of its core to a Jack Henry & Associates’ Symitar system, five major supporting systems, and a reassessment of 22 sub-vendor relationships that needed to be swapped out or adapted to fit this new foundation.

| Technology Profile: Mobiloil Federal Credit Union | |

|---|---|

| HQ: | Beaumont, TX |

| Assets: | $407M |

| Members: | 41,568 |

| Efficiency Ratio: | 67.35 % |

| Data Processor: | Jack Henry: Symitar Quest |

| Data Warehouse: | ARCU |

| Home Banking: | Intuit (at present) |

| Online Account Opening: | Meridian Link: Opening Act |

| Bill Payment: | Intuit (at present) |

| eStatement: | QuestMark (Houston, TX) |

| Mobile Banking: | Intuit (at present) |

| Text Banking: | Intuit (at present) |

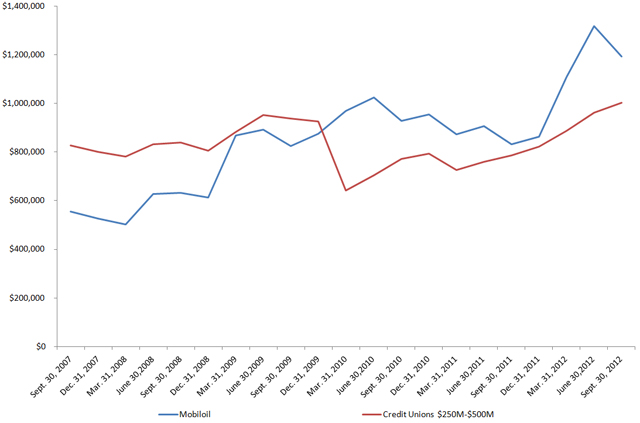

Conversion of the core, the electronic funds transfer system, and the ATM driving system alone netted Mobiloil more than $460,000 a year in savings, James says, and ROA is at 1.59%, up 40 basis points over last year. Although this institution does have a slightly higher operating expense ratio than its peers (3.78% versus an average of 3.61%), according to Callahan & Associates’ industry data, Mobiloil relies on five key best practices to ensure it’s getting the most out of everytechnology dollar spent.

OPERATING EXPENSE RATIO

DATA AS OF SEPTEMBER 30, 2012

Callahan & Associates | www.creditunions.com

Generated by Callahan & Associates’ Peer-to-Peer Software.

Make Vendors Work For Your Business

In March 2011, after some significant staff turnover and the realization that the institution was not fully using the vendor relationships it had, James and his seven-member IT team led Mobiloil in taking a fresh look at its technology surroundings including a decade-old core system relationship.

Though viable for many years, this provider had advanced in ways that were not quite in line with the credit union’s current priorities. And when the vendor did take steps that aligned with Mobiloil’s key priorities such as the abilityto write back to the database and extract more data from that source it was not to the degree the institution hoped for. Realizing that changes needed to be made, Mobiloil decided to set up a vendor audition.

We told our existing provider,come in and talk to us as if we’d never met you before,’ James says. We advised them we would also be bringing in other vendors and whichever offering was the best for the credit union,that’s who we’d do business with.

Both the current vendor and several competing core companies held workshops and demonstrations for senior executives, department managers, and even some front-line staff. In the process, leaders were able to better assess how Mobiloil employeesand members might interact with these systems successfully while minimizing any dependenceon outside conversion consultants.

After narrowing its options down to just the current provider and the strongest challenger, Mobiloil created a small away team that flew out to other institutions to examine how these solutions operated.

The CEO and I tried to remain as nonpartisan as possible. The final commitment wasn’t based on a straw poll, but we still asked everyone who was involved to tell us what they liked and didn’t like about each solution, James says.

In addition to winning the popular vote, the challenger’s system ultimately won out because it presented an advantage in three key areas: the speed at which changes could be made to keep the system compliant, ease of training, and the ability toincorporate new programming code for the institution to produce in house.

Leverage Your Momentum

Once a decision was made on the core conversion, Mobiloil took advantage of that vendor shift to readdress all the ancillary systems the core touched. Although a large-scale conversion required nearly $2 million and effectively shut down anything elseon the credit union’s radar for one year, it actually made the purchase of other technology more feasible.

It was time to replace our RISC mainframe anyway, and we knew some new hardware purchases would start saving us money right away, says James. We just used that as a big coupon toward the new core system and ended up paying less forthese options with our new company than with the old.

The difference in maintenance costs alone for these systems totaled more than $50,000 a year, while increased automation in areas like fee processing, ACH, and Reg D saved the institution from having to hire at least two more full-time employees for theIT department, two for accounting, and two for automation. James estimates these personnel costs would easily have been as high as $300,000 a year.

Buy For The Long Haul

Although it can be tempting to clean house completely, Mobiloil was also well aware that a new system does not always equal a better one.

If we buy something, it’s got to remain a pinnacle of technology for some time, James says. For example, the storage area network (SAN) for the credit union’s imaging system has fulfilled a number of past and current needs atthe institution from Check 21, to virtualization capabilities, to disaster recovery despite having been purchased more than 10 years ago.

This long-haul mentality also means Mobiloil avoids any services or relationships where additional costs, such as per member charges, can quickly hemorrhage out of control.

Save Time And Dollars

Even when a solution offers significant cost savings, make sure it doesn’t come at the cost of lost efficiency or productivity,James says.

In the past, an older signature capture system that Mobiloil had pursued required lending representatives to break the discussion with the member and head off to a printer to retrieve the signed documents.Now, the credit union uses large swivel screens, a smaller tablet on the desktop capable of capturing signatures, and encrypted documents sent electronically to keep the conversation moving and improve lobby workflow. This also shaves up to six minutes on average off of branchsales interactions adding up to about $138,000a year in savings.

Mobiloil employees each already generate about $140,000 more in loans per year than their counterparts at other institutions, and total loans are up 17.9% annually in 3Q 2012.

LOANS ORIGINATED PER EMPLOYEE (ANNUALIZED)

DATA AS OF SEPTEMBER 30, 2012

Callahan & Associates | www.creditunions.com

Generated by Callahan & Associates’ Peer-to-Peer Software.

Know When To Say No

According to James, organizations that use specific technology campaigns to target a single membership demographic for example,Gen Y often end up with limited results. Instead,credit unions should focus on what their membership as a whole is really asking for.

I like to be right up there on the edge of new technology, but I don’t want to do something I don’t think will bring us any benefit, James says. As a member owner, why would you want us spending your cash on somethingyou’re not going to use, instead of paying you better rates and charging you less for a loan

If attracting new membership is an institutional goal, concentrate on things like convenient branch locations and fee-free ATMs, which rank much higher on the list of consumer prioritiesthan online features and mobile apps. And for Gen Y, focus on technology that attracts boomers first. Whom their parents bank with is often more important to young consumers than any flashy,technology-related feature, James says.