GRAPH OF THE WEEK: Credit Union Hiring Spikes Amid Hot Job Market

Credit unions are hosting more FTEs and paying them more than they were one year ago, in large part driven by an extremely competitive hiring environment.

Check all the right boxes while tying your credit union compliance efforts to strategy.

Looking for quarterly data coverage, expert analysis, lessons from leading credit unions, and more? Callahan has it covered. Comparing top-level performance and digging into the details has never been easier.

Callahan & Associates spotlights credit unions that return more value to members.

Langley FCU asked what it would take to be a truly exceptional workplace, and it shares four ways to get there.

Make your succession plan strategic and give it ‘teeth’ to reap the benefits of stronger governance and more effective C-suite leadership.

A public-private partnership in Michigan aims to influence opportunities after high school via a child savings account that provides yearly deposits and every reason to imagine what comes after graduation.

A 55+ member club is helping the Minnesota cooperative strengthen long term relationships, support active aging, and rethink how it serves members later in life.

In the age of smartphones and smartwatches, a strong physical branch network builds trust and credibility.

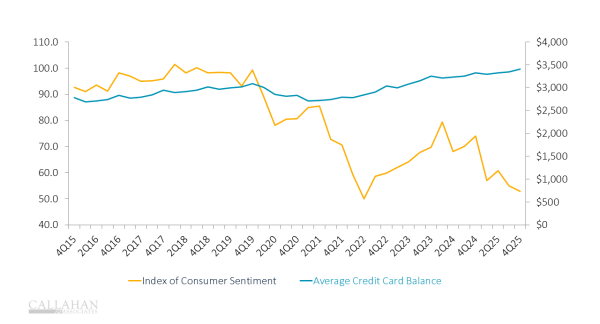

Inflation has cooled, but its aftereffects still shape how credit union members spend, save, borrow, and relate to their credit union.

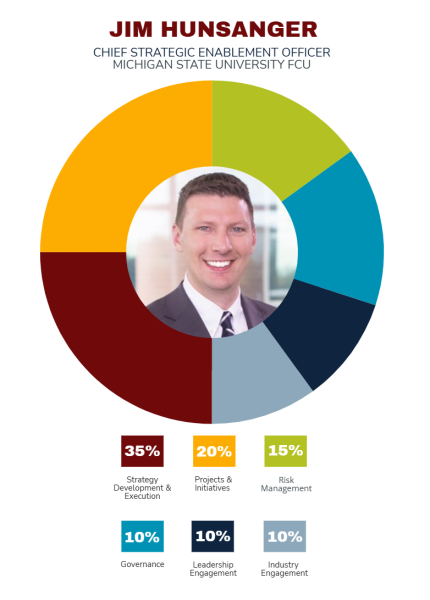

Risk gets a rebrand — and a bigger mandate — at MSUFCU, where a Strategic Enablement department helps initiatives move forward while keeping the organization safe and sound.