Read the full analysis or skip to the section you want to read by clicking on the links below.

LENDING AUTO LENDING MORTGAGE LENDING CREDIT CARDS MEMBER BUSINESS LENDING SHARES INVESTMENTS MEMBER RELATIONSHIPS EARNINGS SPECIAL SECTION: PRODUCTIVITY EFFICIENCY

Credit unions added 1.2 million net new members in the third quarter of 2017 and surpassed 111 million total members. Year-over-year, the number of credit union members grew 4.0% from 107.5 million as of Sept. 30, 2016, to 111.5 million as of Sept. 30, 2017. Member growth for the past five years is 17.6%.

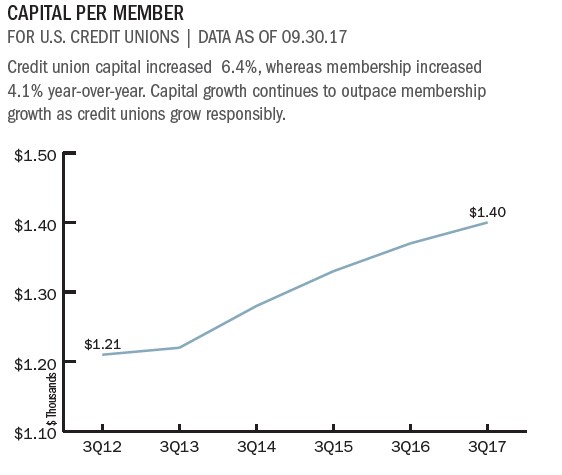

As rosters at credit unions grow, it is important credit unions ensure members are fully using all their cooperatives have to offer. The average member relationship takes the pulse of member usage by tracking the total amount of share and loan balances (excluding member business and commercial loans) a member holds with their credit union. As of Sept. 30, 2017, the average member relationship for all credit unions reached $18,195. That’s a 3.9% improvement over last year’s $17,507.

In addition to average member relationship, accounts per member is another way to gauge member engagement. On average, members hold 2.47 accounts with their credit union. Credit unions with more than $1 billion in assets reported 2.55 accounts per member as of third quarter 2017. Conversely, credit unions with less than $20 million in assets reported an average 1.67 accounts per member. The difference shows a clear relationship between credit union size and the number of accounts held by individual members.

Callahan’s Peer-to-Peer quickly shows how your credit union stacks up against peers for key member-centric metrics. Learn more today.

Although credit union membership increased, members per employee remained consistent, year-over-year, at 386. Broken up regionally, credit unions in the Mid-Atlantic Region reported the highest number of members per employee 445. New England credit unions followed with 380 members per employee. Then came the Southeast Region with 378 and the Western region with 372. Credit unions in the Central Region reported 364 members per employee, the lowest average among regions for the ratio.

Click the graphs below to enlarge and then continue reading to see how TruStone Financial Federal Credit Union staged a competition to showcase local volunteerism.

Member relationships have deepened at credit unions nationwide as members increase their share, real estate loan, and consumer loan activity.

CASE STUDY

TRUSTONE FINANCIAL CREDIT UNION

TruStone Financial Federal Credit Union staged a Show Us Your NeighborGood competition to showcase local volunteerism in the form of nominations, selfies, and digital voting.

Katie Grindeland, TruStone’s director of marketing and communications, says the campaign drove a 245% increase in Twitter mentions and 50% increase in Facebook posts during its four-week run.

For less than $2,300, including prizes, we created an impactful campaign that exceeded our expectations and brought awareness to local non-profits and charities, Grindeland says.

During the social media campaign, nominees had to submit a selfie of them volunteering with the charity for posting on the credit union’s Facebook page.

TruStone’s Facebook followers then selected four weekly winners and the grand prize winner. The credit union also used Twitter to post messages based on trending hashtags and account handles for contest participants.

This encouraged others to share, like, and retweet posts that included personalized content for their channel, Grindeland says.

The promotion generated 42 volunteer selfies and more than 13,000 unique visitors to the contest page, 556% over TruStone’s goal. Nearly 6,000 votes were cast for the $50 weekly winners and $1,000 grand prize winner, an animal rescue group.

Our staff, members, and community were engaged in the contest, Grindeland says. In the end, it truly captured the people helping people’ philosophy that is the foundation of the credit union movement.

Read The Whole Story

Strategy Performance 3Q 2017

Credit unions have made significant gains since the Great Recession started 10 years ago. Third quarter credit union growth trends surged past that of community banks and the overall banking industry. Measures such as loans, shares, capital, and membership have all reached new levels. These gains are all notable and meaningful; however, they are backward-looking. The important question to ask is: Where will credit unions be in the next 10 years? In this issue of Strategy Performance, learn why now is the time for credit unions to challenge themselves.

Read More

RETURN TO INDUSTRY PERFORMANCE BY THE NUMBERS 3Q 2017