This is part of the Callahan Financial Performance Series. Presented by the analysts at Callahan & Associates, the series helps leaders interpret data to drive smarter decisions and uncover new approaches to measure performance. Callahan clients can access the full version of this article right now on the client portal. Read it today.

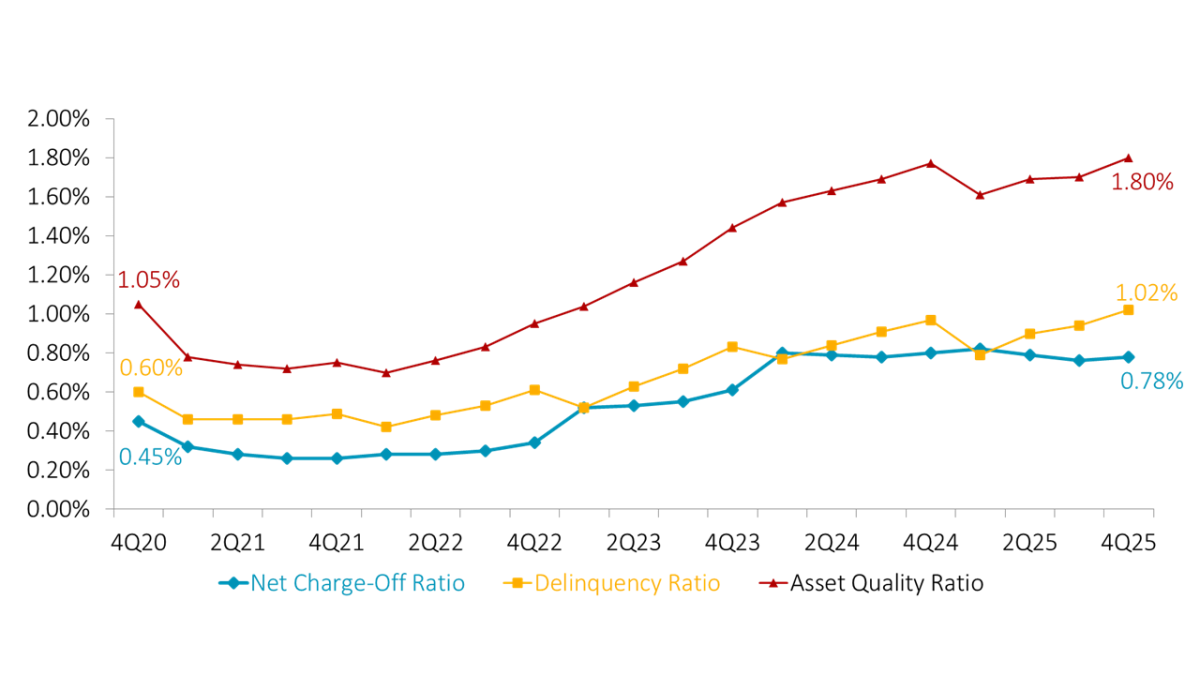

The first quarter of 2025 offered a sign that three years of gradual asset-quality deterioration could be slowing; however, subsequent quarters defied that narrative and moved asset quality squarely back into the spotlight for credit unions and regulators.

Although 2025 was not a record year for increases in delinquency, repayment rates did steadily worsen. The overall loan delinquency rate closed the year at 1.02%, the highest level since the third quarter of 2013.

It is not easy for credit unions to address worsening asset quality without making some tough decisions. Digging deeper into the delinquency and charge-off numbers reveals interesting dynamics in product performance by type. Some product repayment rates have stabilized; other products — including some not historically prone to delinquency — have risen in alarming fashion.

ASSET QUALITY RATIO

FOR U.S. CREDIT UNIONS

SOURCE: CALLAHAN & ASSOCIATES

Dig Deeper Into The Credit Union Loan Portfolio

- First Mortgages — Delinquency has dropped slightly to 0.89%, but that’s still high enough to worry credit unions. Homeownership is the foundation of financial health for many U.S. households, and first mortgages are typically the last product to report higher delinquency. When faced with tough budgetary choices, members usually opt to pay their mortgages before all other debts.

- Other Real Estate — Delinquency has increased to 0.78%. These loans are mostly HELOCs, which have dramatically increased in popularity in the past few years. Many homeowners have tapped into increased home equity to pay for purchases large and small or, more recently, to consolidate other debt. Other real estate net charge-offs remain microscopic, but they have increased 3 basis points annually to 0.05%.

- Commercial — Delinquency fell slightly on the quarter to 0.96%. This is down from last quarter but is 12 basis points higher than one year ago. Commercial lending might not be the priority of many credit union lending programs; however, it has grown as a percentage of credit union portfolios, which makes the rise in delinquency more troubling. Just as troubling is the multi-year increase in net charge-offs, jumping from a low of 0.02% in the first quarter of 2023 to 0.23% in the fourth quarter of 2025.

- Auto — On the brighter side, total auto delinquency held steady year-over-year at 0.96%, a welcome sign following the significant increases in auto delinquency that began in 2022. Although delinquency rates have not returned to pre-COVID levels, the fact total auto delinquency has increased just 6 basis points in the past two years is a welcome reprieve after it increased 48 basis points in the preceding two-year period.

- Credit Cards — Credit card delinquency stayed flat year-over-year, at 2.15%, a positive sign for credit unions and their members. Although steady credit card delinquency often suggests net charge-offs are increasing, this does not seem to be the case this time. Net charge-offs on credit cards have flatlined as well; beginning in 2024, they’ve held steady around 5.00%.

Ready To Read The Full Story? Callahan clients can access the full version of this article right now on the client portal. Read it today. Not yet a client but looking for expert insights to help you adapt to change, develop your organization’s leaders, and stay at the forefront of industry trends? Connect with our team to learn more.