Read the full analysis or skip to the section you want to read by clicking on the links below.

DEPOSITS MEMBERS MORTGAGES CREDIT CARDS LENDING INVESTMENTS AUTO LENDING EARNINGS EFFICIENCY

Strong lending across the industry underpinned an expansion of total assets in the first quarter of 2018.

Loan originations increased $5.0 billion year-over-year, yet annual growth slowed to 4.4%. Total loans on the balance sheet grew 9.7% year-over-year. Prior to this quarter, annual loan growth topped 10% for 14 consecutive quarters.

Despite the slowdown in growth, every segment of the loan portfolio still increased compared to the first quarter of 2017.ContentMiddleAd

Loan originations at credit unions increased to $474.9 billion in the first quarter, a first quarter record for the industry.

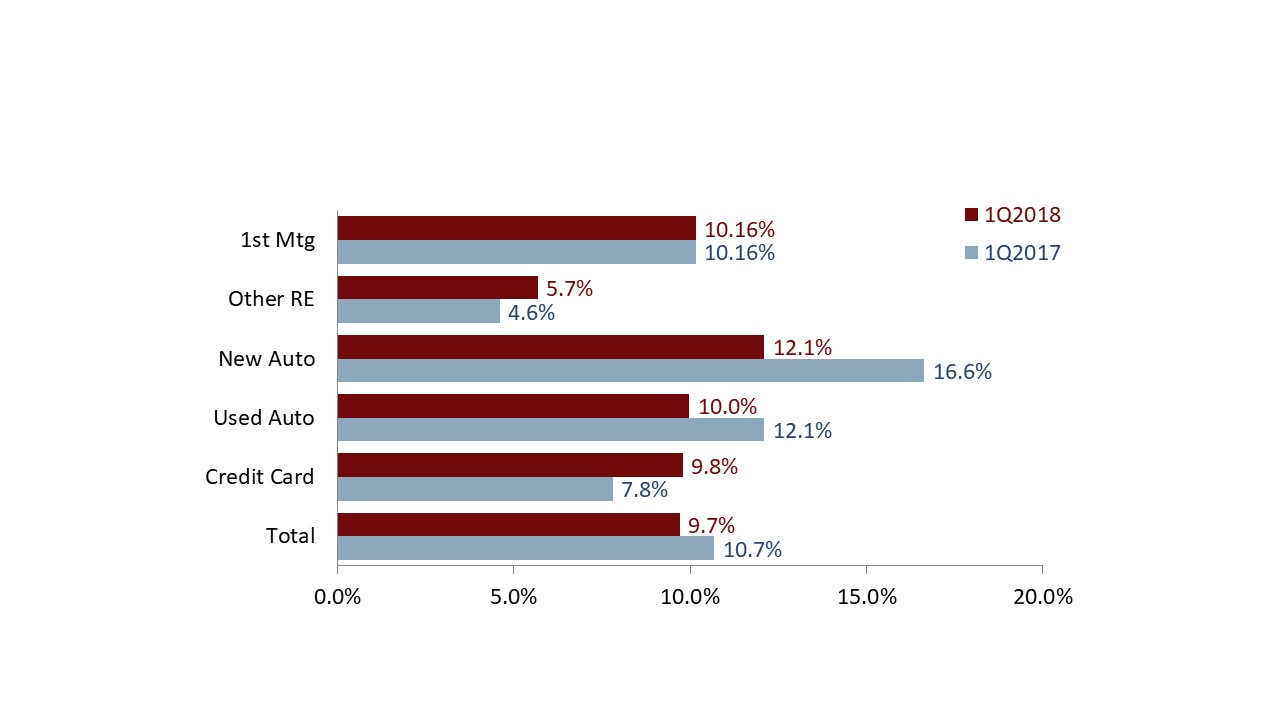

The only two major categories that grew faster this year than last were credit cards and other real estate. Credit card balances increased 9.8%, or $5.1 billion, annually and reached $57.2 billion. Other real estate loans increased 5.7%, or $4.4 billion, and reached $83.1 billion.

First mortgages grew 10.2% annually the same rate as first quarter 2017 and totalled $403.7 billion as of March 31, 2018.

Total auto loans increased 10.8%, or $33.5 billion, annually and reached $343.6 billion as of first quarter 2018. New auto loans grew 12.1%, or $14.7 billion. Used auto loans grew 10.0%, or $18.9 billion. Indirect lending continued to play a significant role in the auto loan portfolio. These loans expanded 16.6% year-over-year and closed the quarter at $202.6 billion.

ANNUAL GROWTH IN LOANS OUTSTANDING

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.16

Annual growth in revolving products accelerated, whereas growth in first mortgages held steady. Source: Callahan & Associates.

Elsewhere in the credit union loan portfolio, private student lending grew 13.9% year-over-year. Balances for these loans stood at $4.6 billion as of March 31. Commercial loans to members increased 2.8% quarterly, and member business loans increased 4.7% quarterly and 14.8% annually. Balances for these segments of the portfolio reached $57.0 billion and $71.7 billion, respectively.

Dig deeper into your credit union’s lending performance, and find out how your lending portfolio stacks up against peers with a custom performance report from Callahan & Associates. Learn more today.

The delinquency rate at credit unions was 66 basis points in the first quarter of 2018. That’s down from 69 basis points one year ago. Credit card delinquency was up 15 basis points to 124 basis points, but credit unions reported a year-over-year improvement in all other loan categories.

The net charge-off ratio for all credit unions was 60 basis points in the first quarter of 2018. That’s up from 58 basis points in the first quarter of 2017.

Despite a slight annual uptick in net charge-offs, credit union asset quality remained manageable.