Like many of its peers, Rogue Credit Union ($1.1B, Medford, OR) has enjoyed strong deposit growth in recent years. Helping that along has been loyalty programs that aim to build even deeper relationships with members.

We know credit unions are different, says president and CEO Gene Pelham. The opportunity we have is to educate members on the benefits of ownership as they make their financial decisions and to think of the credit union in a more holistic way. ContentMiddleAd

CU QUICK FACTS

Rogue Credit Union

Data as of 06.30.16

HQ: Medford, OR

ASSETS: $1.1B

MEMBERS: 104,413

BRANCHES: 16

12-MO SHARE GROWTH: 17.9%

12-MO LOAN GROWTH: 12.2%

ROA: 1.72%

Rogue’s solution is its new Rogue Rewards loyalty program, which the credit union launched in February with the Rogue Rewards Loyalty Dividend and the opening of an Ownership Savings Account for every member.

Rogue has deposited dividends totaling $2.5 million into members’ accounts, and Pelham says the feedback has been overwhelmingly positive.

A Shift Toward Service And Value

Rogue was founded in 1956 as a teachers’ credit union. Today, it is a state-chartered community credit union serving more than 100,000 members from 17 branches across six counties in southern Oregon.

Rogue designed the high-yield Ownership Savings Account as a withdrawal-only savings account earning one of the highest rates available to members currently 2.00% APY. The credit union automatically opens an account for each member as a benefit of membership. Members earn deposits into the account by participating in the credit union under the Rogue Rewards Program. Rogue charges no fees and has no minimum balance requirements on the account.

The credit union paid its first loyalty dividend to all open 98,846 ownership accounts on Feb. 17, 2016. It plans to deposit additional loyalty dividends and other rewards into eligible members’ accounts over time. Rogue’s management is careful to say future dividend payouts are dependent upon the financial performance of the credit union.

The loyalty dividend is the catalyst, but the real glue will be in deploying a relationship with our members that reminds them that being a credit union member is different.

The Ownership Savings Account is non-transactional by design. Members may remove funds from their account at any time by making a transfer to another savings or checking account, but they cannot redeposit these funds once withdrawn, nor can they make additional deposits to the account.

In April 2016, members with a Rogue Visa Platinum card received their 1% cash back rewards as deposits into their ownership accounts. The credit union plans to introduce additional Rogue Rewards promotions later this year.

Don’t reinvent the wheel. Get rolling on important initiatives using documents, policies, and templates borrowed from fellow credit unions. Pull them off-the-shelf and tailor them to the credit union’s needs. Visit Callahan’s Executive Resource Center today.

According to Pelham, Rogue made a strategic shift in focus several years ago toward creating loyalty with members and demonstrating commitment to the local community.

Our management team realized we needed something more than just the one and done’ loyalty dividend, where you pay folks and they forget about it until the next year, Pelham says. The loyalty dividend is the catalyst, but the real glue will be in developing a relationship with our members that reminds them that being a credit union member is different.

A cross-functional team worked full-time on a project for expecting and rewarding participation from May 2015 up until the Feb. 17, 2016, implementation date. Internal Rogue staff handled all aspects of the project, with the exception of the automated account opening, which a third-party vendor helped facilitate. It took just seven minutes to open and fund the accounts via a batch process.

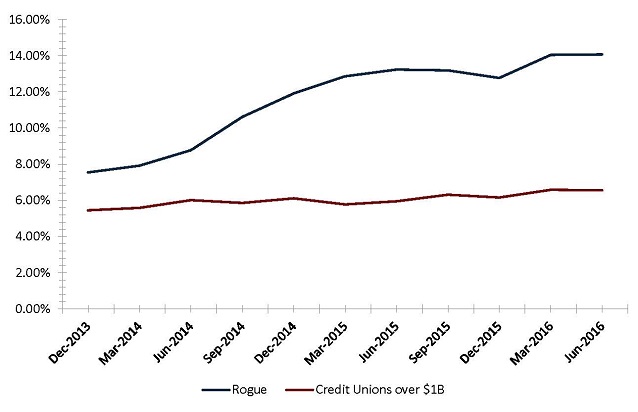

SHARE GROWTH

For CREDIT UNIONS 1B | DATA AS OF 06.30.16

Source: Callahan Associates.

To promote the new Rogue Rewards program, the credit union advertised on television and radio. It also took advantage of free and low-cost promotion through media interviews, online ads, and social media. Positive buzz in the community, amplified by Rogue’s strong reputation and healthy market share, proved critical to spreading the word quickly.

Key in the communicaiton process is Rogue’s decision to place the Ownership Savings Account transaction summary at the top of every member’s statement, which prioritizes its visibility over every other account or loan.

The first account you see on your statement, your internet banking profile, and on the mobile app is your high-yield Ownership Savings Account, Pelham says. Members are reminded every time they access the credit union that they have an ownership interest.

The credit union plans to implement two to four new Rogue Rewards in 2016 and is devoting resources to improving member onboarding and staff training.

Loyalty Rewards Are Having An Impact

In the first few months since implementation, Rogue has realized tangible results from its Rogue Rewards campaign.

According to Rogue executives, of the $2.5 million in loyalty dividends deposited to members’ owner accounts in February, fully 89% of funds remain in the accounts. Rogue’s aggregate balances per member are $18,334, below its $20,677 peer average, but balances have been increasing since the implementation of the ownership account.

Typically, new members don’t open their membership with loans and deposits that total $18,000 or more, so we would expect to see this number decrease with the membership growth we’ve experienced in 2016, says COO Jeanne Pickens. What we are seeing is that not only are new members bringing over full relationships, but existing members are doing more business with us as well.

Rogue tracks active or participating checking accounts, defined as those share drafts with an average daily balance of $500 or more and 10 or more automated transactions per month. As of May 31, 2016, participating checking accounts made up fully 25% of Rogue’s total checking accounts. Due to this increased engagement, share draft penetration has risen from 54.83% in March 2016 to 56.12% in May 2016, the highest level in Rogue’s history.

The impact of the growth in penetration is magnified by the fact that we are growing new members at an annualized rate of over 14%, Pickens says.

Indeed, as of March 2016, the credit union’s annualized membership growth is trending at a robust 14.05%, compared with a 6.59% average among its $1 billion-plus asset peers. This growth rate places Rogue in the 95th percentile among its peer group.

MEMBER GROWTH

For CREDIT UNIONS $1B | DATA AS OF 06.30.16

Source: Callahan Associates.

Continual Trust Building

Rogue’s senior executives have some advice for credit unions looking to implement a member loyalty program. First and foremost is to maintain an unwavering focus on the member across the organization.

It can’t be a marketing department priority or an operations department priority, Pickens says. It must be integrated into multiple areas of the credit union. There has to be ownership from the top and commitment in the areas that are facilitating the initiative.

For Pelham, this means going beyond lip service to incorporate the member’s perspective into every decision, from board room strategy down to day-to-day operations.

Income and growth are not our primary goals, Pelham says. But we are challenging some of the best in the country right now with our performance because we focus solely on creating an experience that our members are willing to pay for.

There are a few tactical aspects of the project that Rogue executives would do a little differently if they had it to do over again.

One is to have had more reward programs in place before the official launch of the Rogue Rewards Program and the Ownership Savings Account. Rogue has since implemented its Visa Reward cash-back program, and has several additional loyalty reward programs in the pipeline for later this year.

Pickens also wishes that they had integrated the new member onboarding more fully into Rogue’s training program prior to rollout. As a result of its recent rapid growth the credit union has been hiring extensively, resulting in some catch-up in ensuring that all new front-line staff are fully immersed in the member loyalty initiatives.

A big part of the process with new members is to educate them on the benefits of ownership, Pickens says. At the initial account opening, the member service representative lets the member know about the Ownership Savings Account and the ways they could immediately benefit from it. It allows for conversations around deepening participation with our members through deposits, loans, and transactions.

How Do You Compare?

Check out Rogue’s performance profile. Then build your own peer group and browse performance reports for more insightful comparisons.

Rogue’s CEO encourages credit unions embarking on a member loyalty project to include all levels of the organization in the initiative.

We developed a strike team including multiple people at all levels of the organization ready to answer member questions, Pelham says. For our members, the loyalty dividend was new, it was different, and they didn’t really know what it meant. So we had 14 additional folks, including members of senior management like Jeanne, on the phones answering members’ questions.

Since the launch of Rogue Rewards, members have demonstrated their loyalty and trust in the credit union in some surprising ways. Pelham recounted the story of a member who received a Loyalty Dividend of $10.77. He left a message with the credit union expressing his appreciation, adding, I’ve owned stock in a bank for years and they never paid me anything.

We are challenging some of the best in the country right now with our performance because we focus solely on creating an experience that our members are willing to pay for.

Not only did this member take the time to leave a message, but he stood up at Rogue’s annual meeting and shared his story again, word for word.

Trust is our greatest currency, Pelham says. At Rogue we work every day to make sure we are continually building that trust with our members.