Fuel Sales On Your Auto And Loan Protection Products With These Winning Points

Protection products offer a range of benefits that safeguard a borrower’s peace of mind while simultaneously buckling up their financial security.

As credit unions move from experimentation to adoption, leaders offer firsthand knowledge on what separates weak policies from strong ones that actually work.

How Members Cooperative focuses on structure, oversight, and clear expectations to ensure AI supports, not undermines, long term strategy.

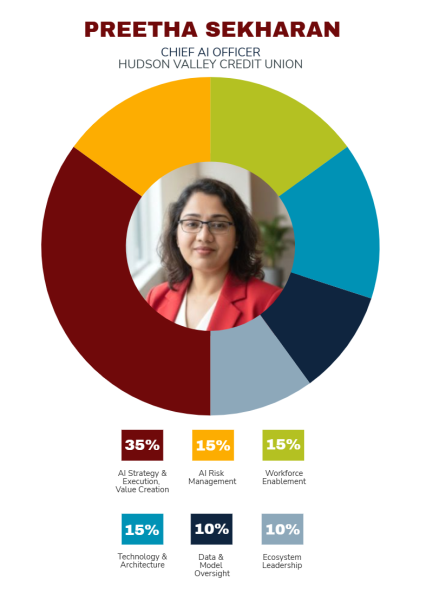

As Hudson Valley Credit Union’s artificial intelligence chief, Preetha Sekharan holds a rare role in the industry, but it’s one that is likely to become far more common in the future.

Artificial intelligence for credit unions has moved from a future concept to today’s full-fledged leadership and governance challenge.

What happens when credit union performance data meets March Madness? Callahan’s proprietary model breaks down state-level results to forecast who takes home the hardware.

Nuvision’s Added Advantage program tracks member engagement across the credit union, then rewards relationships through better pricing and other perks.

CDFI grant funding helps the Florida cooperative offer microloans for small businesses after many banks pulled out of its market.

By aligning governance, leadership, and day to day operations, Marine Credit Union transformed its foundation from a parallel operation into a visible extension of the credit union brand.

Credit union and bank earnings reflect different business objectives. Those differences matter for how financial institutions serve their markets.

AI governance matters as much as innovation when it comes to AI. Learn how BCU built an AI practice that prioritizes data integrity, risk management, and real world decision making.